You paid for coverage. Then the loss hit. Fire, theft, water damage, smoke damage. Your apartment is wrecked, your routine is gone, and the insurance company sends a number that doesn't come close to replacing what you lost.

That first offer feels personal because it lands when you're already exhausted. It also isn't random. On renters insurance claims, the fight usually turns on one issue: renters insurance replacement cost. If you don't understand how that works, the carrier controls the language, the math, and the payout.

Renters commonly become ensnared. The policy says one thing. The adjuster explains it another way. The settlement arrives in pieces. If you don't push back, the “replacement cost” promise gets reduced to a cheap depreciated check and a pile of paperwork.

Table of Contents

- Your Claim Was Low-Balled This Is The First Fight

- Replacement Cost vs Actual Cash Value The Insurer's Shell Game

- Uncovering The RCV Endorsement Your Policy's Hidden Weapon

- Building an Undeniable Inventory to Defeat Adjuster Tactics

- How to Fight the Two-Step Payout and Maximize Your Settlement

- When to Stop Fighting Alone and Hire a Public Adjuster

- Take Control of Your Claim and Get The Payout You Deserve

Your Claim Was Low-Balled This Is The First Fight

A renter loses clothes, electronics, furniture, kitchen gear, and work equipment in a covered loss. They expect help because they kept the policy active and paid on time. Then the carrier sends a settlement that won't even reset the basics.

That shock is common because many renters start underinsured. The average annual cost of renters insurance is around $171, but costs are rising for many, with 23.5 percentage points more policyholders reporting premium increases than decreases. At the same time, average personal property coverage is just $10,000, which leaves many renters exposed before the claim even starts, according to The Zebra's renters insurance cost analysis.

So when the adjuster trims values, disputes brand quality, or classifies your policy in the cheapest possible way, every dollar matters. This isn't just paperwork. It's the difference between replacing your life and going into debt to do it.

Your first payment is often the insurer's test. If you cash it, stay quiet, and move on, they've learned they can settle cheap.

The fight starts when you stop treating that offer as final. Read the estimate line by line. Compare it against what you owned. If the company's adjuster is talking in circles, learn how to handle dealing with an insurance adjuster after a low claim offer.

The first move after a bad offer

- Request the full breakdown: Ask for the carrier's complete contents valuation, depreciation method, and any notes used to downgrade items.

- Check the policy language: You need to know whether the company is paying actual cash value now because your policy requires it, or because they're hoping you won't notice the difference.

- Establish your case early: Don't summarize your loss loosely. Specifics win disputes.

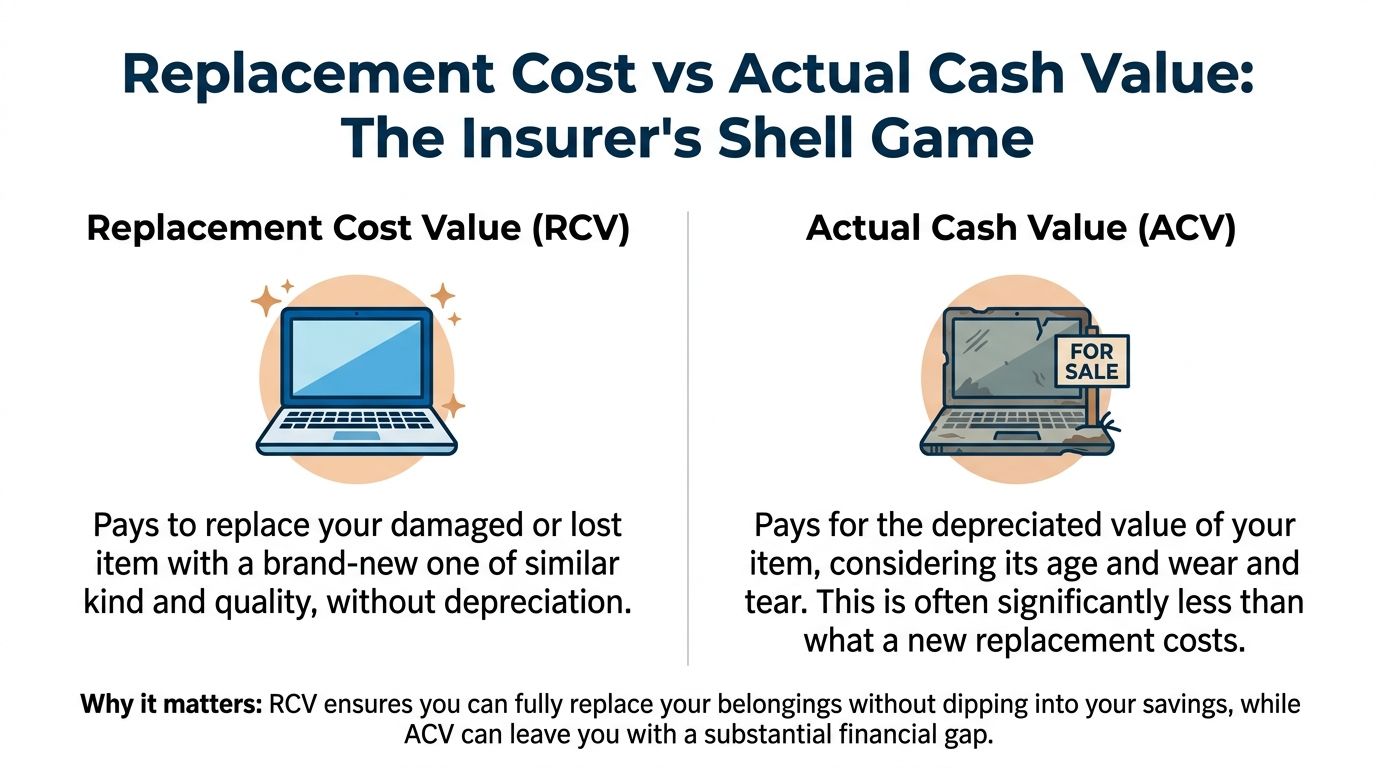

Replacement Cost vs Actual Cash Value The Insurer's Shell Game

Most renters hear two labels and assume the difference is technical. It isn't. It's money.

What the company is really doing

Replacement cost value, or RCV, pays what it costs to buy a new equivalent item. Actual cash value, or ACV, subtracts depreciation first. The carrier knows that policyholders often don't feel the difference until they try to shop for replacements and realize the check won't cover them.

A simple example shows how brutal that gap is. If a $1,000 TV is destroyed and has $500 of depreciation, an ACV policy pays $500, while an RCV policy pays the full $1,000, as explained in Policygenius's guide to replacement cost renters insurance.

The insurer's trick is making depreciation sound reasonable while you're grieving the loss. It isn't reasonable if your goal is to replace what you had.

The payout gap in plain English

Here's the cleanest way to understand the concept:

| Coverage type | What it pays | What happens to you |

|---|---|---|

| RCV | Cost of a new comparable item | You can replace what was lost without eating the depreciation |

| ACV | Used value after depreciation | You pay the gap out of pocket |

That's the whole game. If your couch, TV, laptop, mattress, and cookware are valued as used goods, your claim shrinks fast. If they're valued at replacement cost, your recovery is far closer to reality.

Practical rule: Don't argue “my stuff was expensive.” Argue “my policy owes replacement of like kind and quality.”

If you want a sharper breakdown of how insurers use these two methods, read this comparison of actual cash value vs replacement cost in property claims.

What to challenge immediately

- Depreciation assumptions: If the company applies ACV where your policy supports replacement cost, challenge it in writing.

- Equivalent quality downgrades: A premium item isn't replaced by a bargain-bin version just because the carrier found a cheaper listing.

- Loose descriptions: “Television” gets low-balled. “Samsung 55-inch 4K smart TV” is much harder to cheap out.

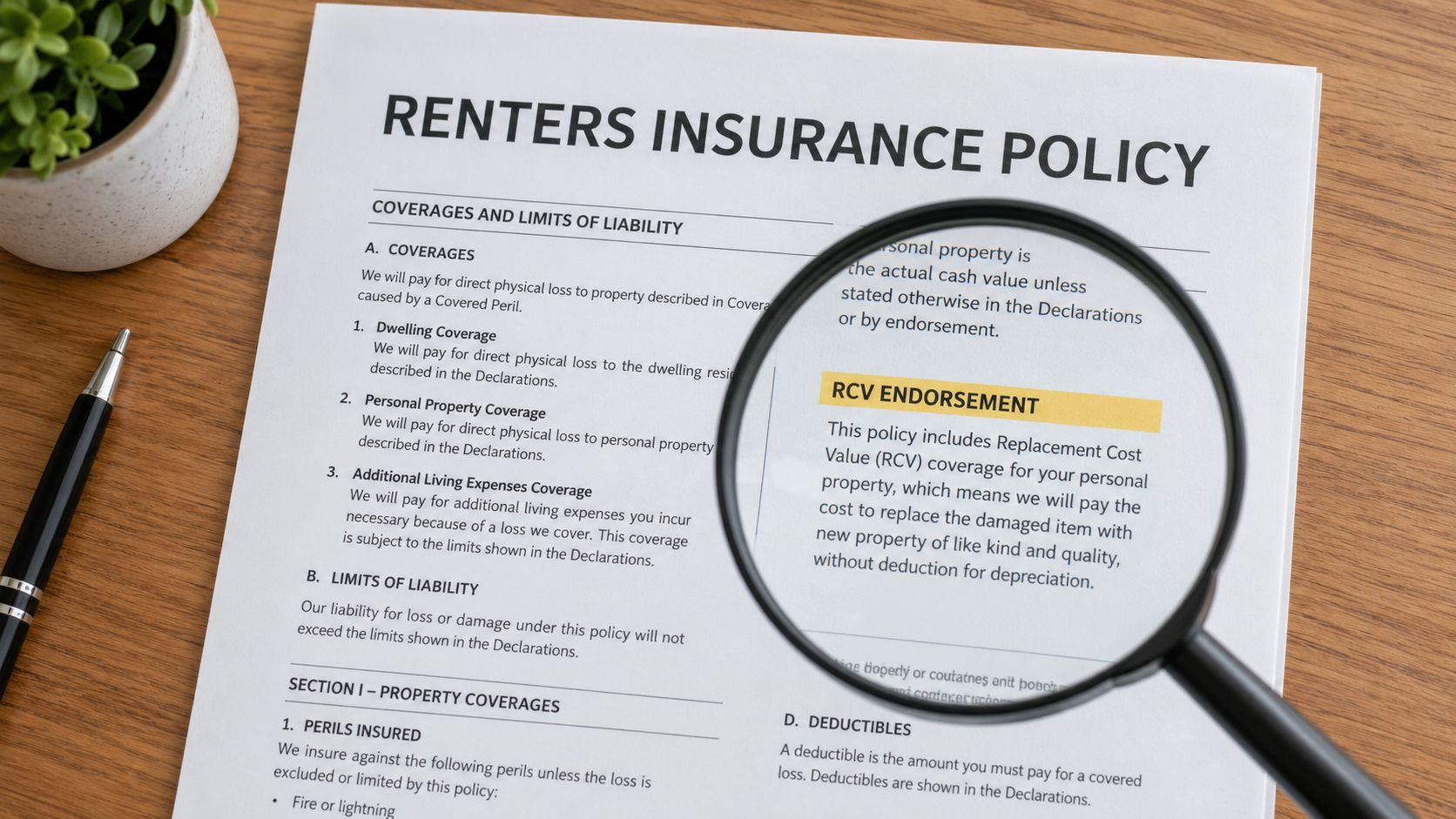

Uncovering The RCV Endorsement Your Policy's Hidden Weapon

Most renters assume replacement cost is built in. That assumption costs people money.

Start with the declarations page

Replacement cost coverage is not automatic. It usually requires a specific replacement cost endorsement listed on the declarations page. Without that endorsement, the policy defaults to actual cash value, which gives the insurer room to reduce the payout by deducting depreciation, according to Wallace Insurance Law's discussion of denied renters claims and replacement cost endorsements.

That means your first job is document review, not debate. Pull the declarations page, endorsements, and personal property section. Look for language that clearly identifies replacement cost for contents or personal property.

If you have that endorsement, the adjuster doesn't get to treat ACV like the final answer. The policy controls. Their opinion doesn't.

What to do if the adjuster plays dumb

Adjusters sometimes speak vaguely on purpose. They'll say the claim is being handled “subject to policy terms” or “based on valuation.” That language is designed to keep you from pinning them down.

Use direct questions:

- Ask where the endorsement appears: Request the exact form name, number, and page.

- Demand written confirmation: Make the carrier state whether personal property is settled on ACV only or eligible for replacement cost recovery.

- Compare the estimate to the contract: If the declarations page says replacement cost applies, ask why the settlement letter reads like an ACV-only claim.

If you're not sure what endorsement language to look for, this breakdown of a personal property replacement cost endorsement helps you identify what should appear in the policy packet.

If the coverage isn't written on the policy, don't assume you have it. If it is written on the policy, don't let the insurer pretend it isn't there.

Building an Undeniable Inventory to Defeat Adjuster Tactics

Insurers love vague inventories because vague inventories are easy to cut.

Your list has to prove quality not just ownership

A bad inventory says “toaster,” “laptop,” “shoes,” “watch.” That's exactly what the carrier wants. Once you describe property in generic terms, they can price the cheapest reasonable substitute and call it done.

Documentation standards are getting tougher. Insurers increasingly want photos, receipts, or serial numbers, and without brand or model data they'll often offer a downgraded equivalent. Just as important, gifted, thrifted, or inherited items are treated the same as new ones under RCV, which many renters miss, as discussed in this insurance forum discussion on replacement value documentation.

That last point matters. If your item came from a thrift store, a family member, or an estate, don't write it off. Replacement cost focuses on replacing the item with like kind and quality, not punishing you because you got it cheaply.

What to gather before the adjuster narrows your claim

Build a forensic inventory, not a casual one.

- Use old photos: Holiday pictures, apartment listing photos, social media posts, and move-in videos often show furniture, electronics, rugs, art, and appliances in the background.

- Pull account history: Amazon, Best Buy, Target, Walmart, Apple, and email order confirmations can rebuild a surprising amount of your contents list.

- Capture product detail: Brand, model, size, finish, material, and any distinguishing features matter.

- Document high-value electronics carefully: Serial numbers, box photos, setup screenshots, warranty emails, and repair records all help.

- Don't skip gifts or inherited items: Write what the item is, who gave it to you, when you received it, and what a comparable replacement would be.

A claim inventory wins when a stranger can read it and understand exactly what must be replaced.

Here's a stronger example:

| Weak entry | Strong entry |

|---|---|

| Laptop | Apple MacBook Air, color and screen size if known, plus purchase email or device photo |

| TV | Brand, screen size, smart TV feature, mounting style, and any visible model label photo |

| Necklace | Metal type, style, gifting history, close-up photos, and any appraisal or jeweler note |

Build your proof in layers

Don't wait for one perfect receipt. Use layered proof.

- Primary proof: receipt, invoice, appraisal, serial number.

- Secondary proof: photos, videos, owner manuals, warranty registration.

- Supporting proof: bank statements, shipping confirmations, repair records, witness statements.

A single missing receipt doesn't kill a legitimate claim. A thin file does.

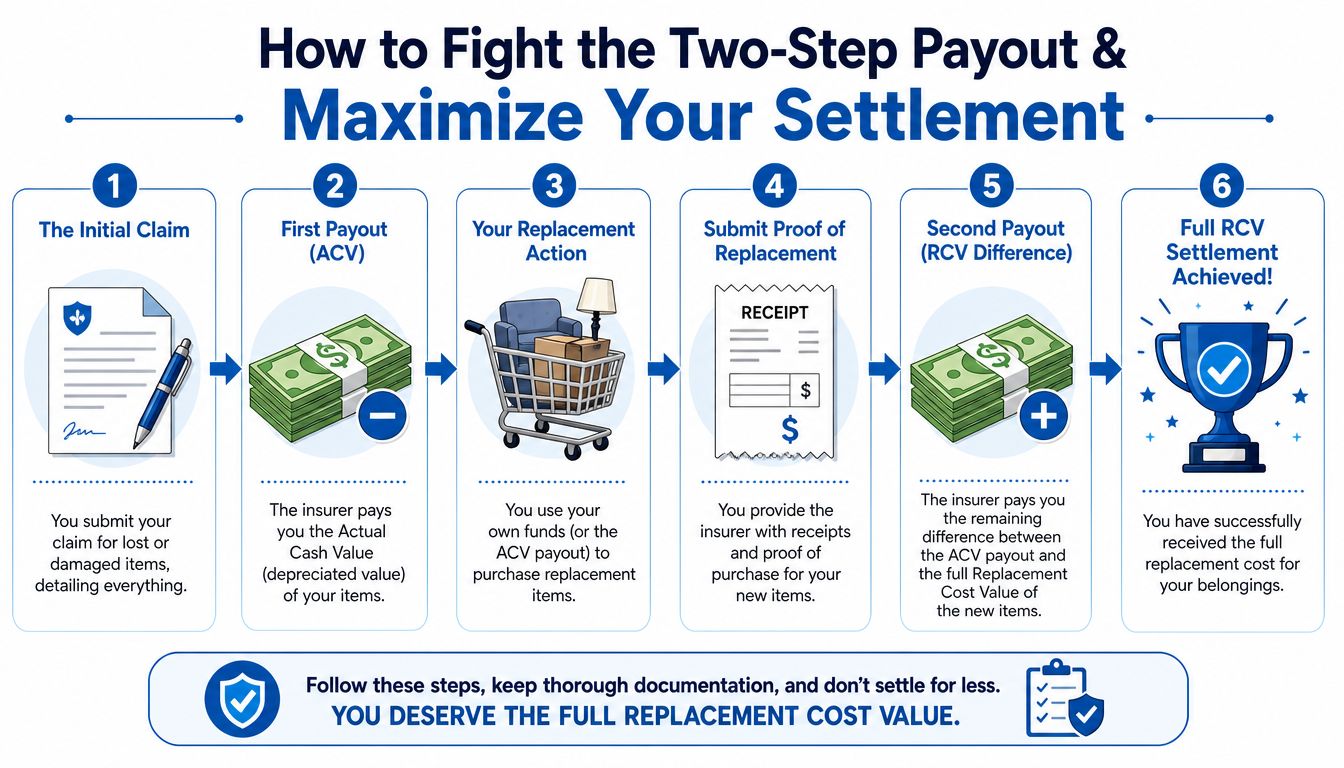

How to Fight the Two-Step Payout and Maximize Your Settlement

The most frustrating part of renters insurance replacement cost isn't the label. It's the payout structure.

Why the two-step payout hurts renters

Nearly all RCV policies require the policyholder to replace the item first and then submit receipts to recover the final payout. The carrier pays the depreciated ACV first, then reimburses the difference later. That creates a cash-flow trap, especially after major losses, and United Policyholders explains that common $30,000 limits can already be insufficient for average inventories.

This system benefits the insurer in two ways. First, it slows down how much cash leaves their hands. Second, it counts on some renters never making the second trip through the paperwork.

That's why so many people with “replacement cost” coverage still end up settling for something that feels like ACV. They run out of money, patience, or both.

Before you tackle the reimbursement process, watch this quick explainer:

How to push back without losing leverage

You don't beat this by complaining in general terms. You beat it by controlling the paper trail.

- Ask for the recoverable depreciation schedule: You need the exact amount being withheld on each item.

- Replace strategically: Start with essential items that are easiest to document and hardest to dispute.

- Submit receipts in organized batches: Tie each receipt to the line item number on the carrier's inventory sheet.

- Challenge mismatches quickly: If the carrier priced a lower-grade item on the front end, don't accept that pricing as the baseline for reimbursement.

- Request clarity on time limits: Some policies impose deadlines for replacement and recoverable depreciation claims. Get those deadlines in writing.

Don't send a pile of receipts with no map. Send a package the adjuster can't pretend to misunderstand.

In some situations, renters can try to negotiate a different path, including asking whether the insurer will waive strict replacement documentation or consider a cash-out approach. Carriers don't volunteer that option. You have to raise it.

What North Carolina and Virginia renters should do

North Carolina and Virginia renters should keep every dispute in writing and demand clear explanations for valuation, depreciation, withheld amounts, and reimbursement rules. If the carrier delays responses, changes adjusters, or keeps asking for the same documents again, treat that as a claim handling problem, not a clerical accident.

Your written dispute should include:

- The policy basis: Point to the contents coverage and any replacement cost language already confirmed.

- The item-level challenge: Identify where the valuation is too low, too generic, or based on the wrong quality level.

- The documentation attached: Receipts, screenshots, photographs, product pages, and inventory references.

- The relief requested: Revised ACV, confirmation of recoverable depreciation, or written approval of replacement documentation.

If the carrier keeps hiding behind process, escalate above the desk adjuster. Ask for a supervisor review. Ask for a written explanation. Ask who made the pricing decision. Adjusters respect files that look ready for scrutiny.

When to Stop Fighting Alone and Hire a Public Adjuster

Some claim disputes stay manageable. Others turn into a second job you never asked for.

The moment the claim stops being manageable

Hire help when the insurer keeps moving the target. That usually shows up as repeated document requests, changing explanations, unexplained depreciation, vague denials of quality, or long stretches of silence after you submit support.

You also need help when the claim gets emotionally heavy. A fire loss, major theft, or serious water damage can leave you trying to inventory your life while also finding temporary stability. Most renters can't do that well while sparring with a trained insurance professional.

The conflict is basic. The company adjuster works for the company. You need someone whose job is to value the loss from the policyholder's side.

What real help should look like

A strong public adjuster should do more than “check in” with the carrier. They should:

- Audit the policy: confirm valuation method, endorsements, limits, and duties after loss.

- Rebuild the contents claim: organize the inventory, improve descriptions, and support like-kind-and-quality pricing.

- Challenge low valuations: dispute generic substitutions and unsupported depreciation.

- Handle communication: stop the endless back-and-forth that wears policyholders down.

- Push the claim to closure: not just reopen the argument.

Clients often say the biggest relief is finally having someone translate the carrier's language and call out what doesn't add up. The best reviews of public adjusters sound similar. The policyholder felt ignored, buried in paperwork, and pressured to accept less. Then someone stepped in, cleaned up the file, and forced the carrier to deal with facts instead of shortcuts.

If you've explained the same problem three times and the insurer still responds with canned language, you're no longer in a normal claim conversation.

Take Control of Your Claim and Get The Payout You Deserve

You don't have to accept a low offer just because it arrived on company letterhead. If your policy supports replacement cost, hold the carrier to it. If the inventory is weak, strengthen it. If the adjuster keeps downgrading your property, force the dispute onto item-by-item specifics where vague excuses fall apart.

This is the core battle plan:

- Confirm the coverage on the declarations page.

- Demand the valuation breakdown.

- Rebuild the contents inventory with real detail.

- Track every withheld dollar of depreciation.

- Submit organized proof of replacement.

- Escalate fast when the company stalls or distorts the policy.

Most renters lose ground when they assume the insurer will “do the right thing” if they stay patient. That's not a strategy. Documentation is a strategy. Written disputes are a strategy. Knowing how renters insurance replacement cost works is a strategy.

Have your water damage claim questions answered at NO COST. Call 919-400-6440 to speak with a licensed Public Insurance Adjuster or Contact Us here with questions. WE Work For YOU… NOT Your Insurance Company!

If your property claim has been delayed, underpaid, or flat-out mishandled, For The Public Adjusters, Inc. helps policyholders in North Carolina and Virginia fight back. Their team represents homeowners and business owners, not insurance companies, and can review the damage, the policy, and the carrier's numbers to see what's being missed.