When a disaster like a fire, flood, or hurricane hits your home or business, your first instinct is to call your insurance company. But here’s the hard truth: the adjuster they send to your property works for them, not you. They are trained to protect the company’s profits, which means paying you as little as legally possible.

This is a fundamental conflict of interest, and it’s why searching for a public insurance adjuster near me is often the single most important step you can take to fight back and protect your financial recovery.

Why Your Insurer Is Not on Your Side

It’s completely understandable to think your insurance provider will be your partner after a major property loss. After all, you’ve paid your premiums on time, every time. You expect them to hold up their end of the deal.

But this is rarely how it plays out when it comes to large homeowner or business claims.

Major insurance carriers, like State Farm or Allstate, are for-profit corporations. Their primary responsibility isn’t to you, the policyholder; it’s to their shareholders. Their entire business model is built on a simple equation: collect as much as possible in premiums while paying out as little as possible in claims. These companies have mastered the art of delaying, denying, and underpaying valid claims to boost their bottom line.

From the second you report your damage, this conflict of interest kicks in and works against you.

Your Claim Advocate vs The Insurer’s Adjuster

It’s crucial to understand who is really in your corner. The adjuster sent by your carrier has a very different job and motivation than a public adjuster you hire yourself.

| Role | Insurance Company Adjuster | Your Public Insurance Adjuster |

|---|---|---|

| Who They Work For | Works for and is paid by the insurance company. | Works exclusively for you, the policyholder. |

| Primary Goal | Minimize the insurance company’s financial payout. | Maximize your financial settlement to ensure full recovery. |

| Allegiance | Loyal to the insurance company’s bottom line. | Loyal to you and your best interests. |

| Incentive | To close your claim as quickly and cheaply as possible. | To document every detail of your loss to get you a fair and just payout. |

The table makes it clear: one is there to protect the company’s assets, the other is there to protect yours.

Common Tactics Used to Minimize Your Claim

To keep their payouts low, insurance companies and their adjusters have a playbook of tactics designed to underpay, delay, or flat-out deny legitimate homeowner and business property claims.

The company adjuster assigned to your case is trained to find reasons to reduce your settlement. They might use confusing policy language, rush you into a quick and low settlement, or conveniently “overlook” significant damages that aren’t immediately obvious. Their objective is simple: close your file for the lowest amount possible, saving their employer money at your expense.

This is where the power dynamic is stacked against you. You can learn more about the critical differences between these roles in our detailed guide on the insurance adjuster vs. public adjuster.

“It’s extremely widespread. Can I prove it? No. But I have had a lot of anecdotal conversations with adjusters about it.”

This quote from an industry insider says it all. There is immense internal pressure on company adjusters to keep settlements down, and it’s the policyholders who pay the price.

Your Advocate in a Biased System

This is exactly why public adjusters exist. Our profession is growing because people are tired of being bullied by their insurance carriers. The industry has ballooned, hitting $14.6 billion in revenue after a 9.6% annual growth rate over the past three years.

That growth is a direct result of homeowners and business owners realizing they need an expert in their corner to dispute an unfair offer and navigate an increasingly hostile claims process.

A public adjuster works only for you. We level the playing field. We meticulously document every detail of your loss, translate the complex language in your policy, and negotiate aggressively with the insurer to fight for the full and fair settlement you are entitled to.

How to Find the Right Adjuster for Your NC or VA Claim

When your insurance company drops a lowball offer on the table, you quickly realize not just any public adjuster will get the job done. The person you hire to fight for you will absolutely define the outcome of your claim. Finding a true professional in North Carolina or Virginia isn’t just a step—it’s the most critical step, and it all starts with some serious due diligence.

First things first: verify their license. This is not a suggestion; it’s a hard rule. For any claim in North Carolina, you have to confirm their credentials through the NC Department of Insurance. If your property is in Virginia, you must check their standing with the VA Bureau of Insurance. Working with an unlicensed “adjuster” is illegal and puts your entire claim in jeopardy. Don’t even think about it.

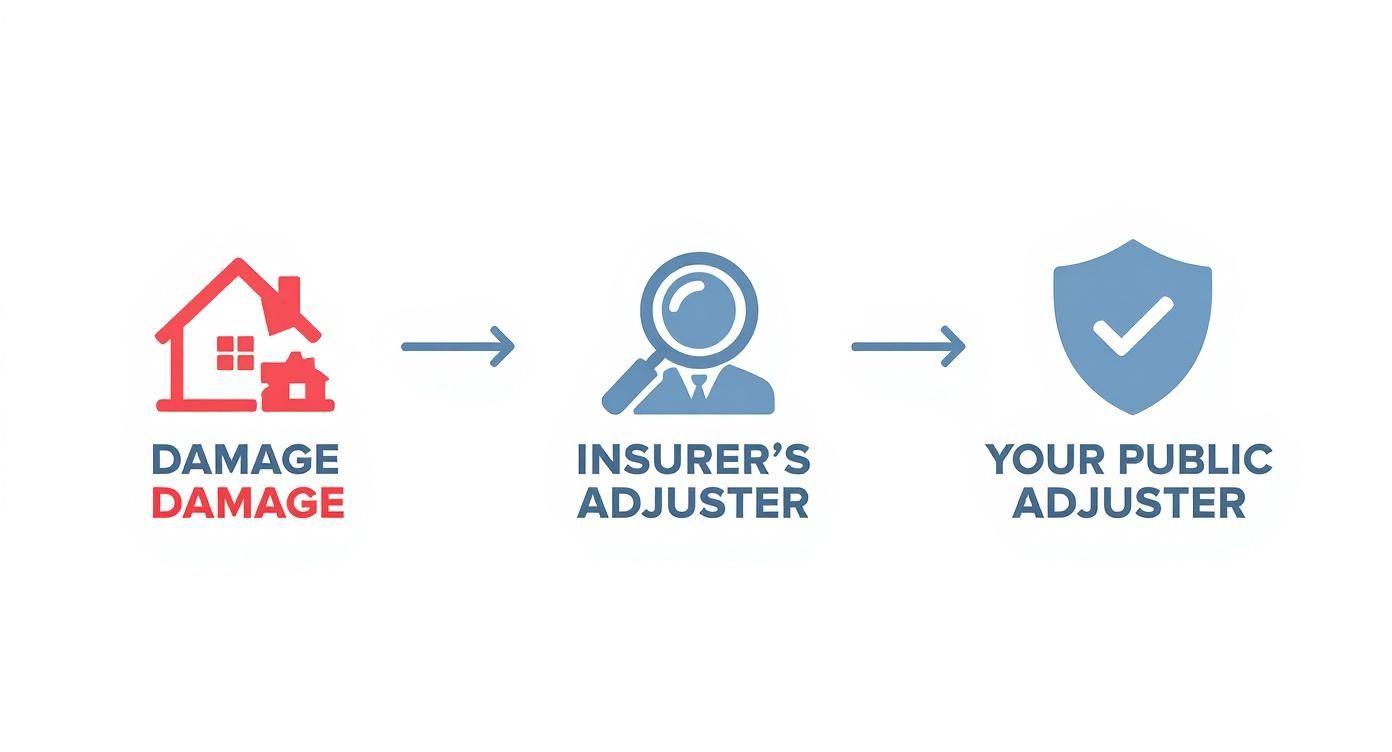

This infographic breaks down the typical claims process and shows exactly where a public adjuster steps in to turn the tables.

As you can see, bringing in a public adjuster isn’t just adding another person to the mix. It’s about shifting the power dynamic back where it belongs—with you. They become a shield against the insurer’s delay-and-deny tactics.

Look for Specialized Experience

Once you’ve confirmed they’re licensed, it’s time to get specific. The public adjuster who spends all their time on hurricane claims in Wilmington probably isn’t the right fit for a massive commercial fire loss in Richmond. Experience in your specific type of dwelling or business damage is everything.

You need to see proof that they’ve handled claims just like yours.

- Fire & Smoke Damage: Can they show you case studies involving total loss valuations? Do they understand smoke remediation and how to fight for it?

- Water & Flood Damage: Ask about their track record with mold, hidden moisture detection, and catastrophic plumbing failures.

- Storm & Wind Damage: They need to have deep, almost obsessive, knowledge of roof systems, siding, and complex structural assessments.

An adjuster who’s been in the trenches with your type of loss knows the playbook. They anticipate the shady arguments your insurer will use to slash the value of your claim and come prepared with a counter-argument that can’t be ignored.

Refining Your Local Search

Googling “public insurance adjuster near me” is fine for a start, but it’s not enough. You have to dig deeper and look for local proof that they actually win against the big insurance carriers.

Get more specific with your search terms. Try things like:

- “Raleigh NC public adjuster reviews”

- “Apex public adjuster fire claim success”

- “Virginia commercial property adjuster case studies”

Hunt for testimonials from people in your own city who were in the same nightmare situation you’re in now. Even better, find reviews that name the exact insurance company you’re fighting. An adjuster who has a history of beating Allstate or State Farm in your area is a powerful ally.

A great public adjuster does more than just estimate damages; they build an undeniable case that forces the insurance company to honor the policy. They are your strategist, your documentarian, and your negotiator.

Finding that local expert is the key. To see what a firm with deep roots in the state can do, take a look at the services offered by a dedicated public adjuster in North Carolina. That local presence means they already know the regional building codes, labor costs, and unique headaches that NC & VA policyholders are up against.

Critical Questions to Ask Before You Hire Anyone

https://www.youtube.com/embed/VjOaa2q0FHI

Once you’ve got a shortlist of licensed, experienced public adjusters, the interview is everything. This is your most powerful tool for separating the true professionals from the rest.

Don’t treat this like a casual conversation. You’re hiring a fighter to go to battle for you against a multi-billion dollar insurance corporation. You need to know, without a doubt, that they have the skill, the strategy, and the grit to win.

Vague, slippery answers are a massive red flag. You’re looking for concrete, specific responses that show they understand the fight ahead—and have won it before.

How Much Experience Do They Really Have with Your Insurance Company?

Don’t let them off the hook with a simple “yes, we’ve handled claims with them.” Pin them down. A great public adjuster won’t flinch at these questions; their track record is their single best asset.

Here’s how to get the real story:

- “My homeowner’s claim is with State Farm. Can you walk me through two recent fire damage claims you handled against them right here in North Carolina?”

- “Show me some examples of water damage claims on a business owner’s policy similar to mine. What were the insurance company’s initial lowball offers, and what were the final settlements you actually secured for the policyholder?”

- “What is your exact strategy for countering claim delays from a carrier like Allstate? What specific actions will you take in the first 30 days to force their hand?”

A confident, seasoned pro will have these case studies ready to go. If they get defensive or hit you with generic lines like “we fight hard for all our clients,” it’s a clear sign they don’t have the specific experience your claim demands.

Who Is Doing the Work and What’s Their Process?

You need to know exactly who you’ll be dealing with day-to-day. It’s a common tactic for a senior adjuster to sign you up, only to pass your file off to a junior associate you’ve never met.

A strong public adjuster relationship is built on clear communication and direct access. You should never feel like your file is just a number, lost in some big, impersonal firm.

Ask them directly: “Who will be my primary point of contact?” and “Will the person I’m speaking with right now be the one personally inspecting my property and negotiating with my insurance company?” Knowing who is actually managing the critical details of your claim is essential for your peace of mind and for getting a successful outcome.

Another non-negotiable step is to ask for a sample contract before making any decisions. Never, ever sign anything under pressure. Take it home, read it carefully, and pay close attention to the fee structure, the scope of services, and any cancellation clauses. This kind of transparency is the hallmark of a reputable firm.

Finally, a crucial question for any public insurance adjuster near me is how they build their case. Ask them, “What software or tools do you use to build your damage estimate, and how is it different from what the insurance company’s adjuster uses?”

Their answer will tell you everything about their technical proficiency. You want someone who is committed to building an undeniable, evidence-based case that gives the insurer no choice but to pay what you are rightfully owed.

Preparing to Work with Your Public Adjuster

Hiring a public adjuster is your first big move. But how you work with them is what truly wins the fight. Once you’ve got an expert in your corner, the real work begins: arming them with the undeniable proof they need to tear down the insurance company’s lowball offer or bogus denial.

Your readiness has a direct impact on how fast and how hard they can go to bat for you.

Think of it this way: your public adjuster is the general leading the charge, but your documents are the ammunition. The better organized you are, the more firepower they have from day one. Don’t make them waste precious time digging for information you’ve already got.

This is about building an ironclad foundation for your claim dispute right from the start.

Your Essential Documentation Checklist

Get these items together before your first strategy session, and your adjuster can hit the ground running. They can immediately spot the weak points in the insurer’s argument and start building a counter-attack based on cold, hard facts.

Here’s exactly what you need to pull together:

- Your Complete Insurance Policy: We need the whole thing—the declarations page and every single endorsement. This is the contract they’re legally bound to, and every word matters.

- All Correspondence: Every email, letter, and text you’ve exchanged with the insurance company, their staff adjuster, or anyone representing them. This paper trail is a goldmine for proving delays, contradictions, and bad faith tactics.

- Photo & Video Evidence: Hand over every picture and video you took right after the damage occurred. Don’t edit or hold anything back. A detail that seems minor to you could be the key piece of evidence that breaks the case open.

- Repair Estimates: If you’ve gotten any quotes from contractors, we need them. It doesn’t matter if they seem high or low; they help establish a real-world baseline for repair costs that your insurer probably ignored.

- Proof of Loss Forms: Did you already submit a Proof of Loss form? Did the insurer send you a blank one? Make sure your adjuster has a copy.

Having this stuff organized from the start does more than just save time. It fires a warning shot at the insurance company, letting them know you are serious, prepared, and ready for a fight. It stops them from using their favorite delay tactic: asking for documents you’ve already sent them.

Why Your Organization Matters

Insurance giants rely on chaos and confusion to wear you down. They bury you in paperwork and bombard you with requests, hoping you’ll get so frustrated you just give up and take their pathetic offer.

When you walk in with a well-organized file, you completely neutralize that strategy before it even begins.

This frees up your public adjuster to go on the offensive. They can focus their time and energy on what really matters: analyzing your policy line-by-line, documenting the full scope of your loss, and building an airtight case for the maximum possible settlement.

This prep work is a critical piece of the puzzle. As our guide on how to negotiate with an insurance adjuster explains, the effort you put in now pays off massively when it’s time to talk numbers. Your readiness speeds up the entire process.

What Happens After You Hire a Public Adjuster

The moment you sign that contract, the real fight begins. Hiring a public adjuster isn’t some overnight magic trick; it’s the start of a methodical process to tear down the insurance company’s weak assessment and force them to pay what your homeowner or business claim is actually worth.

When you bring in a professional, the entire dynamic shifts. Your carrier knows the game has changed.

The first thing we do is send a formal Letter of Representation to your insurance company. This is a legal notice that puts them on blast: you are no longer their point of contact. From this moment on, every single phone call, email, and negotiation attempt has to go through us. This immediately stops the carrier’s reps from calling to pressure, confuse, or trick you into a quick, lowball settlement.

This letter signals that they’re no longer dealing with an overwhelmed homeowner. They’re facing off against a licensed expert who knows their playbook inside and out.

The Independent Investigation Begins

Remember that quick, 20-minute walkthrough the company adjuster did? The one where they were practically looking for reasons to deny your claim? We do the exact opposite.

We launch our own exhaustive, independent investigation to document the full scope of your loss, hunting down every last detail the insurer conveniently “missed” or ignored.

This is a ground-up process that includes:

- A Meticulous Re-Inspection: We conduct a detailed, room-by-room, inch-by-inch analysis of your property. We bring in specialized equipment to find hidden water damage, smoke residue, and structural issues that aren’t visible to the naked eye.

- A Deep Dive Into Your Policy: We scrutinize every line of your insurance policy to find all available coverages. We’re talking about things like code upgrade costs, additional living expenses, or debris removal—coverages the insurance company’s adjuster probably never even mentioned.

- Building a Brand-New Estimate: Using the same industry-standard software the insurers use, but loaded with accurate, local material and labor costs, we build a new, comprehensive estimate that reflects what it really costs to make you whole again.

This isn’t just about getting a “second opinion.” This is about building a comprehensive, evidence-based counter-claim designed to be so thorough and well-documented that it becomes irrefutable.

The Negotiation and Settlement Fight

Once we’ve built this mountain of new evidence, we present it to the insurance company and the real negotiations begin. We go head-to-head with their adjuster, challenging their insultingly low offer point by point. We use our detailed report to prove exactly why their original settlement was incomplete and unfair.

This back-and-forth can take time. But your public adjuster handles every call, every email, and every meeting. We speak their language, and we’re prepared to shut down every delay tactic and flimsy excuse they throw at us. This is a massive industry—the market for claims adjustment services in the U.S. has hit $315.3 billion for a reason. You can dig into the numbers by reviewing the market size research on claims adjusters.

When you hire a public insurance adjuster near me, you’re paying for an expert to take on this entire grueling process. It frees you up to focus on putting your life back together while we go to war for the settlement you rightfully deserve.

Answering Your Questions About Hiring a Public Adjuster

Making the call to hire a public adjuster is a big decision, especially when you’re already staring at a mountain of stress from property damage. It’s completely normal to have questions. Getting straight answers is the only way you can move forward with confidence and start fighting back.

Here are the honest answers to the questions we hear most often from homeowners and business owners when their claim hits a brick wall.

When Is the Best Time to Hire a Public Adjuster?

Ideally, you bring in a public adjuster right after the disaster, before the insurance company’s guy even steps on your property. This lets your advocate control the narrative from day one. But the truth is, you can hire one at any stage of the fight.

It is never too late to get professional help, especially if you see these classic red flags:

- Delay Tactics: Your insurer is dragging their feet, ignoring your calls, or blowing past deadlines they’re legally required to meet.

- A Lowball Offer: The settlement they slide across the table is a joke. It doesn’t even come close to covering the repair estimates you’ve already gathered.

- An Outright Denial: You get a denial letter that makes no sense, full of confusing jargon that seems to contradict the very policy you paid for.

The second you feel like you’re getting the runaround, that’s your signal. It’s time to bring in a professional to take over the fight for you.

My Claim Was Denied. How Can I Afford a Public Adjuster?

You absolutely can. This is one of the biggest misconceptions out there, but our entire fee structure is built to help people in your exact situation.

Nearly every reputable public adjuster works on a contingency fee basis. What does that mean? We only get paid if we win you a settlement. Our fee is a small, agreed-upon percentage of the money we recover for you.

If we don’t get you paid, you don’t owe us a dime. This system ensures our goals are 100% aligned with yours—we are laser-focused on getting you the absolute maximum payout possible.

Will My Insurance Company Punish Me for Hiring Help?

No. Let’s be crystal clear: It is illegal for an insurance company to cancel your policy, jack up your premiums, or retaliate in any way just because you hired professional representation. Your policy is a contract, and that contract gives you the right to have an expert on your side of the table.

Hiring a public adjuster isn’t an act of aggression—it’s an act of self-preservation. You’re simply telling the insurance company that you know your rights and won’t be bullied into an unfair settlement.

They may not like it when you level the playing field, but they are legally forbidden from punishing you for it. Their only choice is to deal with your licensed representative—someone who knows the rules of the game even better than they do.

What’s the Difference Between a Public Insurance Adjuster and a Lawyer?

This is a crucial distinction. A public adjuster is a licensed insurance expert. We specialize in one thing: documenting and valuing property damage, digging into the fine print of your policy, and negotiating a settlement directly with the insurance company. Our entire world revolves around the claim itself.

You need an attorney when the fight escalates to a lawsuit. While some disputes do end up in court, the vast majority can be settled—and won—through the expert negotiation and relentless documentation a public adjuster provides. In most cases, a public adjuster is the first and only expert you’ll need to win what you’re owed.

Q2: How do I verify the license of a Public Insurance Adjuster I find near me?

A: You must verify their license using your state's official Department of Insurance (DOI) website. A licensed Public Adjuster is legally required to carry a valid license for the state where the property loss occurred. Checking the DOI also confirms there are no recent ethical complaints or disciplinary actions.

Q3: Do local Public Insurance Adjusters have better knowledge of my specific state and city building codes?

A: Yes. Local PAs possess critical knowledge of state-specific insurance regulations and local city building codes (e.g., requirements for mandatory upgrades like roof trusses or electrical standards). This ensures that the claim estimate includes all costs necessary for compliant and safe repairs, which often increases the final settlement.

Q4: What is the best way to vet or check the reputation of a local Public Insurance Adjuster?

A: Beyond checking the state license, you should read Google and Yelp reviews that mention specific claims (like fire or water damage), ask the adjuster for client references from your area, and verify they are a member of professional organizations like the National Association of Public Insurance Adjusters (NAPIA).

Q5: If I find a Public Insurance Adjuster near me, how quickly should they respond to my emergency claim?

A: A professional, local Public Adjuster should be able to offer an immediate response (within hours) for emergency situations like fire or severe storm damage that requires immediate mitigation (board-up, water extraction). Prompt response is a key benefit of choosing a PA located "near me."

Q6: Do Public Insurance Adjusters near me charge a fee for the initial inspection and consultation?

A: The vast majority of reputable Public Adjuster companies offer a free, no-obligation claim review. They only charge their contingency fee (a percentage of the settlement) after they successfully increase your payout. You should never pay upfront for an initial consultation. Further, in many states it's against the law to charge an upfront fee for public adjusting services.

Q7: What kinds of property insurance claims do local Public Insurance Adjusters near me handle?

A: Local Public Adjusters handle all types of covered property claims for residential and commercial policyholders, including major losses from fire, water, flood claims, wind/hail storms, hurricane/tornado damage, mold, collapse, and business interruption claims.

Q8: Will hiring a local Public Insurance Adjuster limit my choice of local repair contractors?

A: No. A Public Adjuster works only on the claim valuation and negotiation. They ensure the insurer pays for the work, but you retain the right to choose any licensed contractor you trust to perform the physical repairs on your property.

Q9: Can a local Public Insurance Adjuster help resolve disputes with my specific regional insurance branch?

A: Yes. A local PA often has experience dealing with the specific adjusters and managers in your regional insurance office. This familiarity can be leveraged to streamline communication, address common regional issues, and secure a faster and more favorable negotiated settlement.

Q10: If I hire a Public Insurance Adjuster near me, does that mean they can settle the claim without my permission?

A: Absolutely not. The Public Adjuster is an authorized representative, but you, the policyholder, retain final authority. They can negotiate on your behalf, but they cannot sign release forms or finalize the settlement without your explicit review and authorization.

When you’re going toe-to-toe with a billion-dollar insurance corporation, you need a team of fighters in your corner. If you’re done with the delays and ready to fight for the settlement you deserve, For The Public Adjusters, Inc. is ready to step in.

Contact us today for a free, no-pressure review of your homeowner or business property claim. CALL (567) 888-HELP