The fire trucks have left. The tarp is flapping on the roof. Your tenant has moved out because the place isn’t livable, and the rent that covered your mortgage, taxes, and operating costs has stopped cold. You report the property damage claim, point to your loss of rents coverage, and expect the carrier to pay what the policy promises.

Instead, you get a slow drip of emails, repeated document requests, or a payment position that feels detached from reality. The insurer acts like your lost income is negotiable. It isn’t. If covered damage made the property unrentable, the fight is no longer about whether the loss hurts you. It’s about whether you can prove the amount and force the carrier to follow its own policy language.

A lot of landlords find themselves boxed in. They know the building is damaged. They know the rent stopped. But they don’t know which policy terms matter, how insurers trim these claims, or how to push back without sounding emotional. That’s the gap this guide is built to close.

Table of Contents

- Fighting for Your Rightful Loss of Rents Payout

- What Your Policy Says vs What Your Insurer Claims

- Common Tactics Insurers Use to Underpay Your Claim

- Proving Your Actual Loss with Evidence

- A Landlord’s Guide to Disputing a Bad Offer

- Specific Claim Challenges for NC and VA Property Owners

- Why You Need a Public Adjuster on Your Side

Fighting for Your Rightful Loss of Rents Payout

A typical dispute starts the same way. A storm tears off part of the roof, water gets in, drywall swells, electrical components need inspection, and the tenant leaves because the unit can’t be occupied safely. The landlord thinks the hard part was surviving the damage event. Then the claim process starts, and the insurer shifts the argument to paperwork, timing, and narrow readings of the policy.

That’s why loss of rents coverage matters so much. Historical data from 2019 to 2023 shows this coverage typically replaces monthly rent for 6 to 12 months, and the length of the repair period is the biggest driver of the total payout according to this loss of rental income coverage analysis. In practice, that means the primary dispute often isn’t over whether rent was lost. It’s over how long the carrier says repairs should take.

Where landlords get trapped

Most owners focus first on the building damage number. That’s understandable. The visible damage gets attention. The income interruption claim often gets treated like an add-on, even though for many landlords it’s the part that keeps the property from turning into a financial drain.

A few issues show up again and again:

- The carrier separates the building claim from the income loss: One adjuster talks about roof decking, drywall, and flooring. Nobody gives a straight answer on lost rent.

- Repair assumptions get compressed: The insurer uses a clean, ideal schedule that ignores permitting delays, material lead times, and the fact that trades don’t always line up perfectly.

- The owner gets pushed into waiting: While the insurer “reviews” the rental loss piece, the mortgage payment still comes due.

Practical rule: If the building isn’t tenantable, treat the loss of rents portion like a core claim from day one, not a side issue to revisit later.

For owners dealing with storm-related roof failures, it helps to understand the property-damage side too, because the roof timeline often drives the rent-loss timeline. A practical outside resource on handling storm damage roof claims can help you see how the repair dispute and the income dispute often move together.

What works and what doesn’t

What works is direct proof, a documented restoration timeline, and a clear calculation tied to the policy. What doesn’t work is telling the carrier you’re frustrated and hoping they’ll fill in the blanks fairly.

Insurers count on confusion. The stronger move is to force precision. If they say the unit should’ve been back on the market sooner, make them explain how. If they say the rent amount is too high, make them confront the lease history and market support. A loss of rents claim isn’t won with broad complaints. It’s won by pinning the insurer down on facts they can’t easily dodge.

What Your Policy Says vs What Your Insurer Claims

Most loss of rents disputes turn on a few policy phrases. If you understand those phrases, the insurer has a harder time steering the conversation into vague territory.

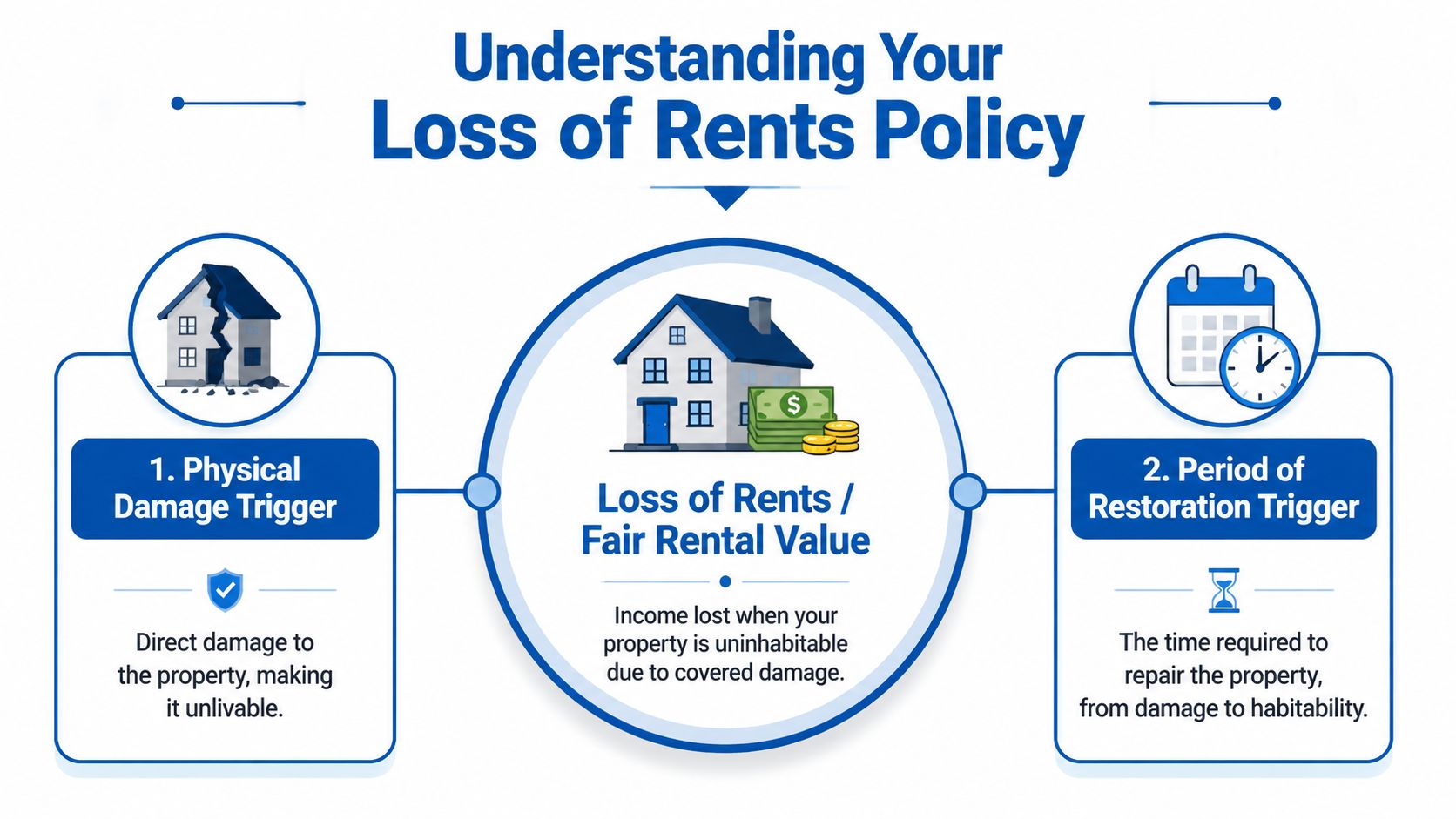

The two triggers that usually matter

At its core, loss of rents coverage is generally tied to two things:

- Covered property damage that makes the building or unit uninhabitable or unrentable.

- A restoration period tied to the time needed to repair and restore tenantability.

That sounds simple. The problems start when carriers reinterpret ordinary words to narrow the claim. They may admit there was damage, but argue the property was still livable enough. Or they may accept that it was temporarily unrentable, but insist the restoration period should be much shorter than reality.

Another point owners miss is that this coverage concerns rental value, not your emotional stress, not your inconvenience, and not every expense connected to ownership. It’s a policy-based income claim. If you’re comparing policy options before or after a dispute, this guide to insurance for rental property investors is useful for understanding how landlord-oriented coverage is typically structured.

The vacancy argument insurers still try

One of the most common bad arguments is that no tenant means no loss. Carriers sometimes act as if a vacant unit can’t generate a valid loss of rents claim because no rent was actively being collected on the date of loss.

That position took a major hit in a significant California appellate decision. In 2013, the California Court of Appeal ruled that loss of rents coverage can apply even when the building was vacant at the time of the loss, and that the “loss of the opportunity to lease” counts as an “actual loss” of rental value, as discussed in this analysis of the 2013 California Court of Appeal ruling.

A vacant unit can still produce a covered financial loss when physical damage destroys the owner’s ability to lease it.

That matters because vacancy is often seasonal, transitional, or part of ordinary turnover. A landlord shouldn’t lose coverage just because a tenant happened not to be in place on the day a fire or storm hit.

What the insurer says versus what the policy usually means

Here’s the practical contrast:

-

Insurer claim: “There was no actual loss because the unit was vacant.”

Policyholder position: If covered damage destroyed the ability to rent the property, the lost leasing opportunity may still qualify. -

Insurer claim: “The unit was damaged, but not unrentable.”

Policyholder position: Tenantability is a factual question supported by inspections, contractor findings, photos, and repair scope. -

Insurer claim: “The restoration should’ve been much faster.”

Policyholder position: The carrier doesn’t get to invent an ideal construction timeline that ignores real repair conditions.

Read the words they rely on

Pull the declarations page, the business income or rental value wording, the definitions section, and any endorsements that modify income-loss coverage. Don’t skim. Read the exact language around covered cause of loss, rental value, period of restoration, waiting period, and any special limitations.

That’s how you stop arguing in generalities. Once the dispute moves from “I think this is unfair” to “your position conflicts with the policy wording,” the advantage changes.

Common Tactics Insurers Use to Underpay Your Claim

Most low-ball loss of rents outcomes don’t happen because the carrier openly denies everything. They happen because the insurer chips away at the claim in several smaller places and hopes you won’t notice the cumulative impact.

They shorten the restoration timeline

This is the cleanest way to reduce a payout without saying “no.” If your rental value is paid during the period of restoration, then a shorter repair duration means a smaller check. The carrier may use a timeline that looks tidy on paper but doesn’t reflect permitting, inspections, sequencing of trades, hidden damage, or code-related work.

When I review these disputes, this is often where the insurer’s number falls apart. The desk estimate assumes a frictionless project. Real repairs rarely work that way.

They squeeze the value of the rent itself

Another tactic is to push down the monthly rental figure. The insurer may ignore signed lease history, discount recurring charges that formed part of the rental value, or rely on a weaker market comparison than the property supports.

A proper rental value analysis should be grounded in objective proof. If the carrier reaches a lower number, they should be able to show exactly what evidence supports it. Many can’t.

They misuse waiting periods and coinsurance

Technical claim language often proves costly. Waiting periods and coinsurance clauses sound minor until the insurer applies them in a way that strips out days of payment or reduces reimbursement more than the policy supports.

Recent claim audits in North Carolina found that nearly 40% of underpaid loss of rents claims stemmed from incorrect application of payout modifiers such as the waiting period and coinsurance clauses, according to For The Public Adjusters’ discussion of underpaid loss of rents claims. That tracks with what policyholders experience on the ground. The underpayment often hides inside “calculation adjustments” rather than a clean denial letter.

Watch closely: If the insurer says the claim wasn’t denied but only “adjusted,” that doesn’t mean the math is right.

They bury you in document requests

Some document requests are legitimate. Others are a tactic. The insurer asks for the same materials twice, requests records that don’t affect the issue in dispute, or keeps the file open while giving no clear calculation.

Common pressure points include:

- Repeated lease demands: Even after you’ve already provided the executed lease or rental history.

- Shifting repair questions: The carrier asks for more contractor detail every time one issue is answered.

- Undefined valuation requests: They ask for “proof of rental value” without saying what standard they’re using.

How to respond without losing ground

Don’t answer confusion with more confusion. Pin every disagreement to one of three buckets:

| Dispute Area | What the Insurer May Do | What You Need to Demand |

|---|---|---|

| Repair duration | Use an unrealistically short timeline | A written basis for the timeline |

| Rental value | Apply a low monthly figure | A line-by-line explanation of the valuation |

| Payout modifiers | Misapply waiting period or coinsurance | The exact policy language and calculation used |

Once you force the carrier to identify its assumptions, weak positions start showing. A vague underpayment is hard to attack. A specific one is much easier.

Proving Your Actual Loss with Evidence

A loss of rents dispute gets easier the moment you stop arguing in general terms and start building a file like an adjuster would. You’re not trying to show that losing rent was painful. You’re trying to prove the exact rental value lost because covered damage made the property unrentable.

Start with gross rental value

The first mistake many owners make is using personal cash-flow logic instead of policy logic. The claim usually turns on gross monthly rent, not on what was left after your own ownership costs. If you begin with mortgage payments, tax bills, or other owner expenses, you’re already speaking the wrong language for this part of the claim.

Loss of rents calculations should be based on objective support. Expert adjusters use proof such as signed lease agreements, historical bank statements, and market-rate valuations, and the process often includes a waiting period of 3 to 7 days before payments begin, as noted qualitatively in the earlier discussion of payout modifiers.

Build the claim file in layers

Use documents that answer different parts of the same question. One document rarely does it all.

- Lease support: Current leases, prior leases, renewals, and rent rolls help establish what the property was earning or would reasonably have earned.

- Payment history: Bank statements and deposit records show consistent collection patterns and expose carrier attempts to undervalue the unit.

- Market support: Comparable listings, broker opinions, or local rental valuations help when the insurer argues your expected rent was too high.

- Damage proof: Photos, inspection reports, contractor scopes, and repair estimates connect the income interruption to physical damage.

- Timeline proof: Emails with contractors, permit records, and scheduling updates show how long restoration required.

Don’t send a pile of records with no explanation. Organize them by issue: rent amount, damage, and restoration time.

Sample loss of rents calculation

Below is a simple format owners can use to present the numbers clearly. Replace the sample labels with the figures supported by your own records.

| Item | Monthly Amount | Total Loss (6 Months) |

|---|---|---|

| Base Rent | Supported by lease | Base Rent x 6 |

| Parking Fees | Supported by lease or records | Parking Fees x 6 |

| Maintenance Charges | Supported by lease or records | Maintenance Charges x 6 |

| Utilities Paid by Tenant | Supported by lease or records | Utilities x 6 |

| Total Claimed Rental Value | Sum of supported monthly amounts | Monthly total x 6 |

If you need a good outside primer on documentation standards, this piece offers expert guidance on proving insurance claims that aligns with the broader principle that unsupported numbers invite disputes.

What usually fails

Owners hurt their own position when they rely on rough estimates, informal text messages, or unsupported opinions about market rent. Another common problem is sending only the lease and nothing that proves the property couldn’t be rented because of damage.

A persuasive file does two jobs at once. It proves the rent amount, and it proves why that rent could not be earned during the restoration window. If either half is weak, the insurer will attack the gap.

A Landlord’s Guide to Disputing a Bad Offer

A low offer is not the finish line. It’s the insurer’s opening position. If the number doesn’t reflect the policy language, the repair reality, or your documented rental value, the right move is to dispute it in writing and force a substantive response.

What to put in the dispute letter

Keep the tone firm and factual. Don’t write a rant. Write a claim position.

Your letter should identify:

-

The policy provision at issue

Quote the rental value or loss of rents wording, the covered cause of loss wording, and the restoration language the carrier is relying on. -

The exact point of disagreement

State whether the dispute is over tenantability, monthly rental value, waiting period treatment, coinsurance, or restoration duration. -

Your calculation

Attach a clean summary showing how you arrived at the amount claimed and which records support each component. -

Your demand for re-evaluation

Ask for a revised coverage position and written explanation of any remaining disagreement.

Use the policy timeline against bad assumptions

Some policies cap the indemnity period at 12 months, while some let the policyholder select 6 or 12 months, which gives you a concrete framework when the insurer tries to distort the restoration argument, as outlined in this overview of loss of rents duration options.

That matters in disputes because carriers often talk loosely about “reasonable repair time” without anchoring their position to the actual policy limit you purchased. If you selected a specific duration, that election belongs in the conversation from the beginning.

Escalation tools that actually matter

A dispute gets stronger when you stop asking the insurer to “take another look” and start demanding precision.

Consider these pressure points:

- Request the carrier’s math: Ask for the exact calculation, not a summary conclusion.

- Force a timeline breakdown: If they shortened the restoration period, ask which trade activities they included and excluded.

- Invoke the appraisal clause when appropriate: If the policy provides appraisal and the dispute is over amount of loss, that may be a serious advantage.

- Document every response delay: A slow file often becomes a pattern, and patterns matter.

A weak dispute says the offer feels unfair. A strong dispute says the offer conflicts with the policy and the evidence.

For owners dealing with rental property disputes specifically, this article on how a public adjuster can help with rental property claims gives a useful view of where professional claim support becomes worth it.

When to stop fighting alone

If the insurer keeps changing the rationale, ignores your documents, or hides behind vague calculations, that’s a signal. So is a claim where building damage, code issues, and rental loss are all tangled together.

At that stage, the issue usually isn’t that you haven’t explained enough. The issue is that the carrier now knows you’re negotiating without equal technical support. That’s when many owners lose ground they could’ve kept.

Specific Claim Challenges for NC and VA Property Owners

North Carolina and Virginia owners deal with a claim environment that generic online advice often misses. Hurricane-driven losses, wind-driven rain, coastal exposure, and high post-storm claim volume create a messy reality. Carriers may inspect quickly, write lean scopes, and move files fast before the full repair picture is clear.

That creates a direct problem for loss of rents coverage. If the building estimate is incomplete, the restoration timeline is usually incomplete too. And when the insurer starts from a short timeline, the rental-loss payment often shrinks with it.

Covered peril issues matter more in coastal claims

Loss of rents coverage is triggered only by a covered property loss. It doesn’t apply if the damage came from an excluded peril like flood, unless flood coverage was added, and it excludes expenses that don’t continue during the interruption, such as mortgage interest or taxes, under the Underwriters Rating Board form addressing loss of rents.

That distinction becomes critical in NC and VA coastal claims. Owners may have wind damage, water intrusion, storm surge, and flood-related issues mixed together in the same event. If you don’t separate which damage came from which cause, the insurer will often use that confusion against you.

Why local claim knowledge matters

A generic adjuster may not appreciate local permitting pace, contractor availability after a regional storm, or what comparable rental value looks like in your area. That can distort both the repair schedule and the rent calculation.

For policyholders dealing with an underpaid or denied property claim in this region, this guide on how to dispute an insurance claim is a helpful next step.

Local context matters because the dispute isn’t happening in a vacuum. It’s happening in your market, with your repair conditions, under your policy, after your loss event. That’s where many carrier shortcuts break down.

Why You Need a Public Adjuster on Your Side

The insurance company’s adjuster works for the insurance company. That isn’t an insult. It’s the structure. If your loss of rents claim is being delayed, narrowed, or underpaid, you need someone whose job is to build your side of the file, challenge weak assumptions, and negotiate from the policy forward.

A strong public adjuster does more than complain about the insurer’s number. They document tenantability issues, organize lease and bank support, test the carrier’s restoration timeline, and push back when waiting periods or valuation methods are being applied incorrectly. They also know when a claim has crossed the line from ordinary adjustment into a real dispute.

What that help looks like in practice

When a property owner is trying to manage repairs, tenants, contractors, and a mortgage at the same time, claim strategy usually slips. That’s where professional representation changes the dynamic. Instead of reacting to the carrier’s latest request, the claim gets built proactively.

For a deeper look at that role, this explanation of what a public adjuster does for policyholders lays out why independent representation matters when the claim becomes adversarial.

One more resource may help if you want to hear directly from the firm.

If your insurer is low-balling your loss of rents coverage, the worst move is to assume the first serious offer is the best available outcome. It usually isn’t. Bad assumptions can be challenged. Weak calculations can be exposed. Vague denials can be forced into writing.

For The Public Adjusters, Inc. represents homeowners, dwelling policyholders, and business owners facing denied, delayed, and underpaid property damage claims in North Carolina and Virginia. If your rental income claim is stuck in a dispute, you don’t have to take the carrier’s version of the policy at face value. Have your water damage claim questions answered at NO COST. Call 919-400-6440 to speak with a licensed Public Insurance Adjuster or Contact Us here with questions. WE Work For YOU… NOT Your Insurance Company!