An insurance dispute lawyer is who you call when your insurance company stops being your safety net and starts acting like your adversary. These are attorneys who only represent property owners—homeowners and business owners like you—when a dwelling or commercial property claim is unfairly denied, deliberately delayed, or shamelessly underpaid.

They’re the legal muscle you bring in when polite negotiations have failed and your carrier—be it State Farm, Allstate, or any other—refuses to honor the contract you paid them to uphold.

When Your Insurance Company Becomes Your Opponent

It’s a gut-wrenching feeling. You’ve paid your premiums on time, every time, trusting that your insurance company would have your back after a fire, hurricane, or busted pipe destroyed your home or business. Instead of a check to rebuild, you get the runaround. A lowball offer that won't even cover the drywall. Or worse, an outright denial letter full of confusing legal jargon designed to make you give up.

Make no mistake: this isn't just bad customer service. It’s a calculated business strategy. Insurance carriers like Allstate and State Farm are billion-dollar corporations with entire departments dedicated to one thing: minimizing what they pay out on claims. Their profits depend on it. This immediately puts you at a massive disadvantage, fighting a financial giant all by yourself.

The Insurer's Playbook of Delay and Denial

Insurance companies are experts at playing the waiting game. They know that the more they stall and drag out your claim, the more desperate you’ll become. A financially and emotionally drained homeowner is far more likely to give up and accept a terrible settlement. Many use systems for automated claims processing that can flag claims for extra scrutiny, often unfairly, leading to more delays.

Their tactics are frustratingly common because they work. You might be experiencing:

- The Document Black Hole: They demand endless paperwork, asking for the same forms over and over or requesting records that have nothing to do with your property damage. This is a classic delay tactic.

- Going Ghost: Your adjuster, who was so friendly at first, suddenly stops returning your calls and emails. Your claim is left in limbo for weeks, then months, while your life is on hold.

- "Policy-ese" as a Weapon: They twist the language in your policy, pointing to obscure exclusions they claim justify denying your payment. They’re betting you won’t have the expertise to fight back.

- Lowball Intimidation: The company adjuster pressures you to take a fast, cheap payout, sometimes even hinting that your legitimate claim might be fraudulent if you push for more.

These aren’t the actions of a partner. They are the moves of an opponent who has a clear game plan to pay you as little as possible. When you see these red flags, it’s a sign that you're no longer just managing a claim; you're in a dispute.

Below is a quick-reference table to help you identify when it’s time to stop negotiating and start escalating your fight.

Red Flags That Signal You Need a Legal Expert

| Insurer Tactic (Red Flag) | What It Means for Your Claim | Your Next Strategic Move |

|---|---|---|

| Silent Treatment | Your claim is being "slow-walked" to frustrate you into accepting a low offer. | Document every attempt to contact them. Consult an attorney or public adjuster immediately. |

| Endless Document Requests | They're building a paper trail to justify a potential denial or delay. | Keep organized copies of everything you send and note the dates. |

| Pointing to Vague Exclusions | The insurer is misinterpreting the policy in their favor, hoping you won't challenge it. | Ask for the specific policy language in writing and get a professional opinion. |

| Lowball Offer with Pressure | This is a classic tactic to close the claim quickly and cheaply, preying on your stress. | Never accept a first offer. Tell them you need time to review it with a professional. |

| Blaming You for the Damage | They suggest you failed to mitigate or maintain the property to avoid paying. | This is a serious accusation and a clear sign you need professional representation. |

Recognizing these tactics for what they are—strategic maneuvers to protect their profits—is the first step toward taking back control of your claim.

Why You Need a Legal Advocate

When your insurer trades its promise of protection for a playbook of opposition, you have to change the game. An insurance dispute lawyer does more than just level the playing field; they force the carrier to play by a completely different set of rules—the law.

These attorneys know every trick in the insurer's book and, more importantly, they know the state and federal laws that prohibit "bad faith" insurance practices.

An insurance dispute isn't just about the money. It's a fight to hold a massive corporation accountable for the promise it sold you. Filing a lawsuit is often the only way to make them take you seriously.

Think of this guide as your new battle plan. We'll walk you through the essential role an insurance dispute lawyer plays and show you precisely when taking legal action becomes your best and only option for getting the money you are owed.

What an Insurance Dispute Lawyer Actually Does

Let's be blunt. An insurance dispute lawyer isn't just another attorney. They are the legal specialist you bring in when your insurance company has drawn a line in the sand, deciding their bottom line matters more than rebuilding your home or business. Think of them as the general you call when polite negotiations have failed and it's time to go to war with a carrier like Allstate or State Farm.

Their one and only job is to wield the full power of the legal system to force a fair outcome for your property claim. While a public adjuster fights on the battlefield of negotiation, an insurance dispute lawyer prepares for—and wages—war in the courtroom.

Building a Case Brick by Legal Brick

The first thing a good lawyer does is rip your insurance policy apart, legally speaking. They scrutinize every word, comparing the specific language against what actually happened to your property and how the insurer responded. They're hunting for one thing: proof the insurance company broke the rules, either by breaching their own contract or by violating state law. This is a level of forensic analysis that goes miles beyond a typical claim review.

From there, they start taking formal legal actions that the insurance company cannot ignore:

- Official Demand Letters: These aren't just strongly worded emails. They are legally loaded documents that detail the insurer's failures and put them on notice: pay what's owed, or we'll see you in court.

- Filing a Lawsuit: When the carrier still refuses to do the right thing, the lawyer files a formal complaint for breach of contract or, in the most outrageous cases, for insurance "bad faith."

- Forcing Legal Discovery: This is where the game completely changes. Your lawyer can legally force the insurance company to turn over internal emails, private adjuster notes, training manuals, and internal memos—the kind of evidence you could never get on your own.

The discovery process is the key that unlocks the truth. It's how a lawyer proves an insurer didn't just make an honest mistake; they made a calculated business decision to delay, deny, or underpay your claim.

For example, your lawyer might unearth an internal email from a supervisor telling adjusters to "keep all hurricane estimates low to protect Q4 profits." That isn't just a smoking gun; it's the kind of concrete evidence that wins bad faith lawsuits. In the landmark case State Farm Mut. Auto. Ins. Co. v. Campbell, the U.S. Supreme Court upheld a verdict against State Farm for a nationwide scheme of capping payouts and using fraudulent practices, showing just how far some insurers will go to protect profits.

From the Negotiating Table to the Courtroom

Once they've built an ironclad case, your insurance dispute lawyer becomes your champion in high-stakes negotiations, mediation, or even a full-blown jury trial. They take over all communications, shielding you from the stress and intimidation tactics that insurance company lawyers love to use.

Modern lawyers are also armed with powerful tools. Many are now using AI for legal research to dissect thousands of past cases and policy documents with lightning speed, giving them an edge against the massive corporate legal teams they're up against.

Ultimately, an insurance dispute lawyer’s job is to escalate the fight. They take your claim from being a simple disagreement and turn it into a serious legal threat that a billion-dollar corporation can no longer brush aside. They transform your claim from a number on a spreadsheet into a major financial and reputational risk for the insurer, forcing their hand to finally pay you what you were owed all along.

Public Adjuster vs. Insurance Lawyer: Which Ally Do You Need?

When your home or business gets hammered by a disaster, figuring out who to call can feel overwhelming. You’re already reeling from the damage, and now you’re facing off against your insurer’s adjuster—a professional trained to protect the company’s bottom line, not yours.

To even the odds, you need an expert in your corner. But who? A public adjuster or an insurance dispute lawyer?

Making the right choice at the right time is everything. It can be the difference between getting a check that actually covers your repairs and getting stuck with a lowball offer that leaves you paying out of pocket. Both are fierce advocates for policyholders, but they fight in different arenas and are called in at different stages of the battle.

The Diplomat vs. The Special Forces

Think of a public adjuster as your frontline negotiator and damage expert—your skilled diplomat. They are the first call you should make when you have a significant homeowner or commercial property claim. Their entire job is to manage the claim from day one to prevent a dispute before it ever starts.

A public adjuster’s mission is to:

- Meticulously document every last inch of damage.

- Dig through the fine print of your policy to find every bit of coverage you're entitled to.

- Build a professional, detailed estimate that reflects the true cost of getting you back to normal.

- Negotiate directly with the insurance company's adjuster to get a fair settlement without ever needing to go to court.

Their goal is to build such an airtight, well-documented case that the insurer has no logical choice but to pay what you are rightfully owed. Many policyholders don’t know the difference, but understanding the roles of an insurance adjuster vs. a public adjuster is the first step toward taking back control of your claim.

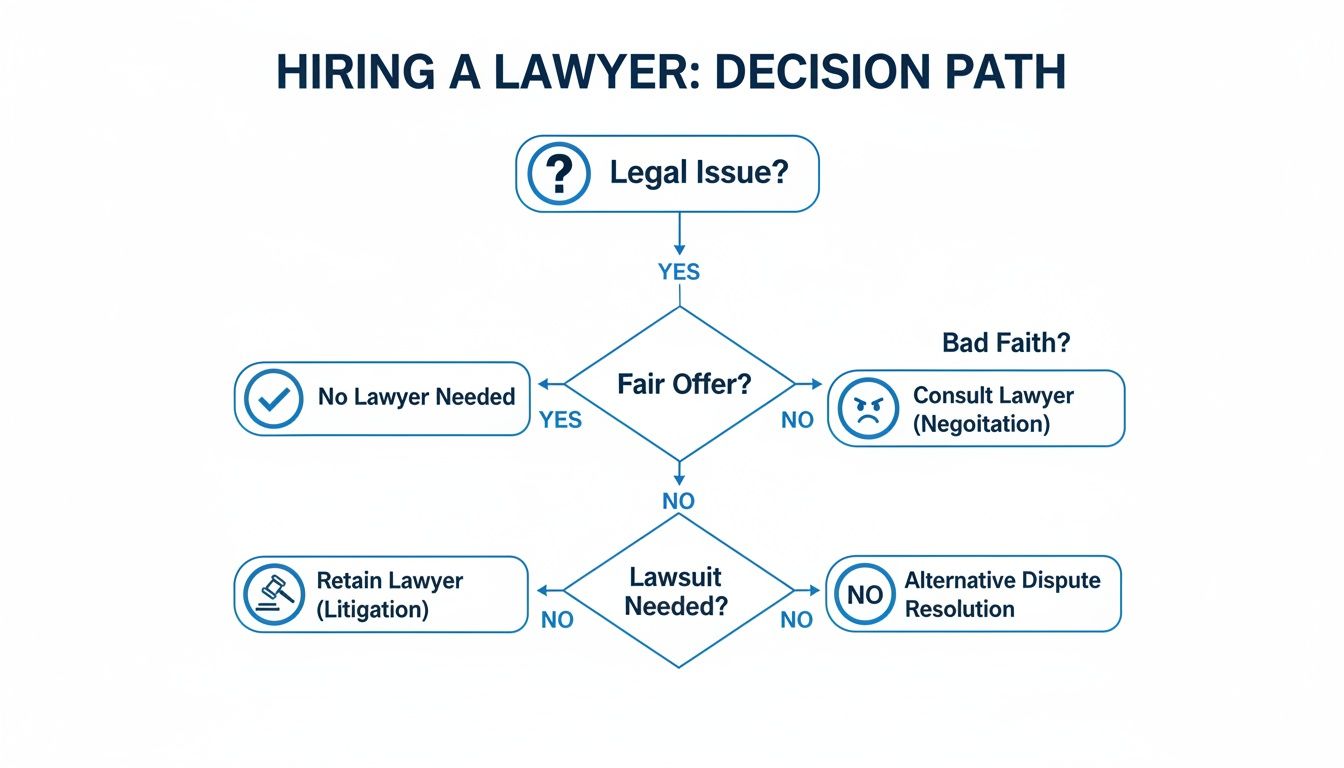

When to Escalate to an Insurance Dispute Lawyer

An insurance dispute lawyer is your ultimate escalation. You bring in the legal firepower when diplomacy has failed and your insurer is playing hardball. If the public adjuster is your diplomat, the lawyer is the special forces team you send in when the insurance company has declared war on your claim.

It’s time to lawyer up when your insurer:

- Outright denies your valid claim based on a flimsy, self-serving interpretation of a policy exclusion.

- Acts in "bad faith" by using deceptive tactics, lying about what’s covered, or dragging their feet on the investigation.

- Refuses to budge from a ridiculously low settlement offer, even after your public adjuster has handed them undeniable proof of the real damages.

This flowchart breaks down the decision of when to bring in legal help.

As you can see, legal action is the final, most powerful move you can make when an insurer simply refuses to do the right thing.

To make it even clearer, here’s a quick breakdown of how these two vital roles compare.

Public Adjuster vs. Insurance Dispute Lawyer at a Glance

| Aspect | Public Adjuster (Your First Call) | Insurance Dispute Lawyer (Your Legal Escalation) |

|---|---|---|

| Primary Role | Damage assessment, policy interpretation, and claim negotiation. | Legal representation, filing lawsuits, and fighting in court. |

| When to Hire | Immediately after a significant property loss. | When your claim is denied, underpaid, or stalled (bad faith). |

| Expertise | Construction, property damage valuation, claims process management. | Insurance law, civil litigation, bad faith statutes, and courtroom strategy. |

| Main Goal | Maximize your settlement through pre-litigation negotiation. | Force payment through legal action, sue for damages and penalties. |

| Fee Structure | Small percentage of the final settlement (5% to 15%). | Contingency fee, often 33% to 40% of the awarded amount. |

| Licensing | Licensed and regulated by the state Department of Insurance. | Licensed by the state Bar Association to practice law. |

This table shows how each professional serves a distinct, critical purpose in your recovery. One handles the technical claim, the other wields the power of the law.

A Powerful Partnership for Your Claim

The smartest strategy is almost always to start with a public adjuster. Why? Because their work creates the rock-solid foundation of evidence—the detailed reports, photos, and professional estimates—that an insurance dispute lawyer needs to build a winning lawsuit. The public adjuster's meticulously prepared file becomes the core of the legal case.

It proves the insurer had all the information needed to pay the claim fairly but chose not to.

Here’s a real-world success story. A public adjuster representing a commercial property owner after a fire in North Carolina presented a detailed $750,000 claim to State Farm. The insurer came back with a pathetic lowball offer of just $200,000, inventing reasons why certain damages weren't covered.

The public adjuster had built such an ironclad evidence file that when the business owner hired an attorney, the lawyer used that exact file to sue for bad faith. Faced with a lawsuit built on undeniable proof, State Farm quickly caved and settled for $725,000 rather than get destroyed in front of a jury.

Starting with a public adjuster maximizes your chance of a fair settlement through negotiation. If the insurer still wants to fight, the adjuster's work gives your lawyer the ammunition needed to win in court.

This one-two punch ensures you’re using the right expert for each phase of the fight. The public adjuster handles the technical side, while the lawyer steps in to leverage the law when the insurance company refuses to listen to reason. This partnership is your best defense against the delay, deny, and defend tactics that define the modern insurance industry.

How Lawyers Win Bad Faith and Denial Lawsuits

When an insurance company like Allstate or State Farm decides to play hardball, a good insurance lawyer doesn't just argue with them. They strategically dismantle the insurer's entire case, piece by painful piece, using the full force of the law.

Winning these fights isn't about crossing your fingers and hoping for the best. It’s about executing a methodical legal strategy built to expose the insurer's bad behavior and force their hand.

Lawyers essentially go to war on three main fronts. The path they take depends entirely on how your insurance company has decided to wrong you.

Challenging a Wrongful Claim Denial

The most common battle is over a flat-out wrongful denial. Legally, this is a breach of contract lawsuit. In plain English, your lawyer is arguing that the insurance company took your premium money but refused to hold up its end of the bargain.

To win, your attorney has to prove that your loss was absolutely covered under the policy you paid for and that the insurer had no legitimate reason to say no. They do this by:

- Dissecting the Policy: They become experts in your specific policy, finding the exact language that proves your damage is covered. They know how to neutralize the obscure, confusing exclusions the company adjuster is hiding behind.

- Bringing in the Experts: They'll hire engineers, contractors, or industrial hygienists to provide scientific proof of what caused the loss. This makes it nearly impossible for the insurer to get away with blaming "wear and tear" on a roof that was clearly wrecked by a hailstorm.

- Filing a Lawsuit: This is the move that forces the insurance company to stop ignoring you. Once a lawsuit is filed, they have to defend their denial to a judge, where their usual delay tactics and stonewalling don't fly.

This kind of legal pressure is often all it takes to make a stubborn insurer suddenly see reason and come to the negotiating table with a fair offer.

Fighting an Extreme Underpayment

Sometimes, the insurance company doesn't deny the claim—they just insult you with a ridiculously lowball offer. When that happens, your lawyer’s job is to prove the true and full cost of what it will take to make you whole again.

The strategy here is to overwhelm the insurer's flimsy estimate with a mountain of indisputable proof. An insurance dispute lawyer will take the detailed reports, damage estimates, and thorough documentation from a public adjuster and use it as the bedrock of their legal case.

By showing a judge the massive gap between the insurer's lowball number and the actual repair costs, they build a powerful case that the underpayment wasn't an honest mistake—it was a deliberate business tactic.

Suing for Insurance Bad Faith

A bad faith lawsuit is the nuclear option. This isn't just a simple contract dispute over money anymore. This is an accusation that the insurance company acted dishonestly, unreasonably, and without any justifiable reason for its actions.

A bad faith claim argues that the insurer knew—or should have known—it had a duty to pay you, but it deliberately chose to protect its own profits instead of honoring its legal and ethical obligations to you, its policyholder.

Winning a bad faith lawsuit means proving the insurer’s malicious intent or reckless disregard. Consider the case of a business owner whose fire claim is denied because the insurer dug up some obscure policy exclusion. A lawyer can prove bad faith by uncovering internal company emails showing that adjusters are trained to use this exact tactic to deny otherwise valid claims.

This often involves forcing the insurer to comply with an Examination Under Oath, a formal proceeding where their representatives must answer tough questions under penalty of perjury. You can learn more about how an Examination Under Oath works in our detailed guide.

When a bad faith case is successful, a court can order the insurer to pay not just what they originally owed on your claim, but also massive punitive damages as punishment. Landmark cases have resulted in multi-million-dollar verdicts for homeowners, proving that with the right legal strategy, you can hold them accountable for both the claim they owe and the devastating harm they caused by breaking their promise.

Understanding the Costs and the Legal Battle Ahead

When your home or business has been devastated, the last thing you want to think about is another huge bill. The idea of hiring a lawyer can feel completely out of reach, and that’s a fear the insurance companies count on.

But here’s the reality they don't want you to know: you don't need a fat bank account to get an expert lawyer in your corner.

Most seasoned insurance dispute lawyers work on a contingency fee basis. Think of it as a partnership where your lawyer is betting on your success. They don’t get paid a dime unless they win money for you.

You pay absolutely nothing upfront. Instead, the lawyer’s fee is a pre-agreed percentage of the final settlement or verdict they secure. This system puts your lawyer’s interests directly in line with yours. They have a powerful financial incentive to fight for every last dollar you’re owed, because if you don’t get paid, neither do they.

What Does the Legal Timeline Look Like?

Hiring a lawyer kicks off a formal, structured fight designed to force the insurance company’s hand. Every claim is different, but the legal battle generally follows a clear path. Knowing the roadmap can take some of the mystery and fear out of the process.

Here’s what you can typically expect:

- Initial Consultation and Case Review: This is where your lawyer goes deep. They'll pour over your policy, the denial letter, and every piece of communication you've had with the insurer. If they see a clear path to winning, they’ll take on your case.

- Filing the Complaint: This is the opening shot. Your attorney drafts a formal lawsuit, filing it with the court and officially accusing the insurance company of breaking their contract or acting in bad faith.

- The Discovery Phase: Get ready, because this is often the longest and most crucial stage of the fight. Your lawyer uses powerful legal tools—like depositions and formal requests for documents—to force the insurer to hand over their internal files, adjuster notes, and emails you’d never see otherwise. This is where the truth comes out.

- Negotiation and Mediation: Armed with the evidence uncovered in discovery, your lawyer enters into serious settlement talks. Many times, a neutral mediator is brought in to help push both sides toward a fair agreement before a trial becomes necessary.

- Trial: If the insurance company still stubbornly refuses to do the right thing, your case goes to trial. Your lawyer will present all the evidence to a judge or jury, who will then make the final, legally binding decision.

It’s not a quick process, but it’s a powerful one. It's often the only way to make a big insurance company finally pay what they should have paid in the first place.

Why You Can’t Settle for Anything Less Than Local Expertise

The insurance claim battlefield is getting more brutal every year. The global market for legal protection insurance is exploding—it's projected to jump from $16.20 billion to a staggering $23.55 billion by 2029. This isn't just a random number; it's proof of a massive increase in legal fights and skyrocketing costs. Meanwhile, the insurance carriers’ own defense costs have shot up by 30% since 2019, and they're passing that aggression on to you. You can read more about the trends in legal protection insurance to see just how intense the landscape has become.

When you're fighting a claim in North Carolina or Virginia, you need more than just a good lawyer; you need a lawyer who lives and breathes the specific property insurance laws of your state.

The laws that govern bad faith claims, the deadlines for filing a lawsuit (statutes of limitations), and how policies are interpreted can be wildly different from one state to the next. An attorney who knows the local court system, the judges, and the opposing law firms in NC or VA has a massive advantage. They understand the specific legal arguments and precedents that will make or break your case right here at home.

Your Next Steps to Take Control of Your Insurance Claim

Let’s be clear: you are not powerless in this fight. Staring down a claim denial or a lowball offer feels like running full speed into a brick wall. But you have options, and the path to taking back control starts right now.

The single most important first move you can make is to get an independent, professional assessment of your damages. This has to be done by someone completely separate from the insurance company’s adjuster, who is paid to protect their employer’s bottom line, not yours.

This unbiased evaluation becomes the bedrock of your fight. It gives you the hard evidence you need to tear down the insurer's flimsy excuses. Whether your battle ends in a tough negotiation or you need an insurance dispute lawyer to file a lawsuit, it all starts with having a real expert on your side documenting the true scope of your loss.

Building Your Foundation for a Successful Dispute

Before you do anything else, you have to protect your position. The insurance company has been building its case against paying you since the moment you called them. Now, it's your turn.

Start by getting a no-cost claim review from an expert public adjuster. This initial gut check costs you nothing and gives you a professional opinion on how strong your claim really is. From there, a public adjuster can build the detailed damage reports and estimates that become the core of your evidence—the ammunition you need to fight back and show the insurer you won’t be bullied.

Your Immediate Action Checklist

Taking back control means taking decisive action. Follow these steps immediately to protect your rights and get ready for what comes next:

- Gather Every Single Document: Get your hands on your full insurance policy and organize all emails, letters, and any other communication you’ve had with your insurer and their adjuster.

- Create a Communication Log: Start a detailed log of every phone call. Write down the date, time, who you talked to, and a quick summary of what was said. This record can be priceless.

- Do Not Sign Final Releases: Never, ever sign a "final payment" or "release of claim" form from your insurer without having a professional review it first. It’s often a trap to close out your claim for pennies on the dollar.

- Schedule Your Expert Review: This is the game-changer. An expert can walk you through all your options, including the steps for appealing an insurance claim denial and knowing when it's time to bring in the lawyers.

You’ve paid your premiums faithfully, expecting your insurance company to be there for you. Holding them to that promise isn’t asking for a favor—it’s demanding what you are contractually owed.

The message here is simple: you can win this. The delay-and-deny tactics used by carriers like State Farm and Allstate are designed to make you feel exhausted and alone. But with the right team fighting for you, you can beat their playbook, get the full settlement you deserve, and finally start putting your life back together.

Frequently Asked Questions

Going up against your insurance company is overwhelming, and it’s natural to have a lot of urgent questions. Here are some straight answers to the things homeowners and business owners ask us most when their insurer is digging in its heels.

How Long Do I Have to Sue My Insurance Company in NC or VA?

This is one of the most dangerous traps in any insurance dispute, and it’s called the statute of limitations. It’s the legal deadline for filing a lawsuit, and if you miss it, your claim is dead—no matter how right you are.

In North Carolina, the general rule is three years for a breach of contract lawsuit. Virginia is a bit more generous, typically giving you five years from the moment the insurance company broke its promise (like the day they sent your denial letter).

But here’s the kicker: insurance companies like State Farm love to bury clauses deep in their policies that slash this timeline, sometimes down to just one year. You have to act fast. The only way to be certain about your deadline is to have an insurance dispute lawyer review your policy immediately.

Can I Sue My Insurance Company for Emotional Distress?

Yes, you can, but it’s a very high bar to clear. This isn't about the normal stress and frustration that comes with fighting a denied claim. To win, you have to prove the insurer’s behavior was genuinely extreme and outrageous.

This type of claim is usually part of a larger "bad faith" lawsuit. Your lawyer would need to show that the company’s actions were intentionally malicious or reckless, causing you severe emotional harm. Think intimidation tactics, knowingly lying about your coverage, or deliberately stalling your claim to drive you into financial ruin. It’s a tough fight, but for the most egregious cases, it's absolutely necessary.

What if I Already Cashed the Insurer's Check?

Cashing the check doesn't automatically mean your fight is over, but it can make things a lot harder. The critical detail is the language on the check itself or in any separate release form you might have signed.

If the check was marked as a "full and final settlement," the insurance company will argue that you’ve accepted their offer and closed the case. Even then, you might still have options if you can prove you were misled, pressured, or didn't understand the consequences. The best move? Stop talking to the insurer, don’t sign anything else, and let an expert public adjuster or an insurance dispute lawyer review the payment and paperwork before you do anything else.

Can a Lawyer Help with a Denied FEMA or NFIP Flood Claim?

Yes, but you need to understand that this is a completely different war. Claims under the National Flood Insurance Program (NFIP) operate under unforgiving federal laws, not state insurance codes. NFIP and its representatives, including Write Your Own (WYO) company adjusters, are notoriously difficult to deal with, often delaying and denying valid claims.

The rules are rigid, and the deadlines are brutal:

- You often have just 60 days to file a sworn "Proof of Loss" document—a tiny window.

- A lawsuit can only be filed in federal court, not your local state court.

- The system is complex, and adjusters often look for any reason to deny coverage.

Because of this difficulty, getting help from a public adjuster early is crucial to build a strong case. If a dispute arises, you absolutely need an insurance dispute lawyer who has specific, hands-on experience fighting FEMA and the NFIP. This is not a job for a general practice attorney; it demands a specialist who knows this unique and challenging system inside and out.

When your property claim is met with delays, denials, or lowball offers, you need an expert on your side from the start. The team at For The Public Adjusters, Inc. provides no-cost claim reviews to help North Carolina and Virginia policyholders understand their rights and build the strongest possible case. Don’t let the insurance company dictate your recovery—get the professional help you deserve by visiting https://forthepublicadjusters.com today.