You opened the estimate, scanned the line items, and felt your stomach drop. The carrier says your roof, water, fire, wind, or business property loss is worth far less than what it will take to repair, replace, and reopen. The adjuster sounds calm. The paperwork looks official. The number still feels wrong.

That reaction usually is right.

Property claim negotiation isn't a polite back-and-forth between equal sides. It's a controlled contest over scope, pricing, coverage, and pressure. If you're a homeowner or business owner in North Carolina or Virginia, especially without representation, the insurer often starts with structural advantages you don't have. The good news is that those advantages can be challenged when you know how to negotiate settlement from a position of proof, not emotion.

Table of Contents

- Your Claim Dispute Is a Battle You Can Win

- Build Your Pre-Negotiation Arsenal

- Calculate Your True Number and Make Your Demand

- Counter Common Insurer Tactics and Low-Ball Offers

- How to Escalate When Your Claim Is Denied or Stalled

- Claim Help Is Here with For The Public Adjusters

Your Claim Dispute Is a Battle You Can Win

The first offer often tells you how the rest of the claim will go. If it's low, stripped down, vague, or missing obvious damage, the insurer isn't inviting a fair discussion. It's testing whether you'll accept less, get tired, or negotiate against yourself.

Why the first offer feels insulting

In property claims, the numbers don't just reflect damage. They reflect who documented the damage better, who controlled the inspection, and who framed the dispute first. That is why many policyholders feel blindsided. They thought they were submitting a covered loss. The carrier treated it like a cost-control file.

Unrepresented claimants face a real disadvantage. Research reveals that unrepresented claimants in property damage cases receive 18–22% lower settlements than those with public adjusters or attorneys, and the same source says insurers now use AI-driven screening to flag unrepresented claimants for underpayment in some cases, which can be countered with certified documentation that makes the claim appear litigation-ready from the start, according to this discussion of negotiating leverage for claimants.

Practical rule: Stop treating a low offer like a misunderstanding that will fix itself. Treat it like a position that has to be challenged with records, estimates, and written rebuttal.

A lot of homeowners and business owners waste the first critical weeks arguing by phone. That usually helps the carrier more than it helps you. Verbal complaints disappear. Written objections backed by evidence don't.

Leverage beats frustration

The right mindset is simple. You're not asking for a favor. You're forcing the insurer to account for the full scope of covered damage.

That means you need bargaining power. Bargaining power comes from three things:

- A complete file: photos, videos, contractor estimates, contents lists, moisture records, invoices, and communication logs.

- A defendable number: not a guess, not a round figure, but a total you can support line by line.

- A structured response: every omission, pricing issue, coverage dispute, and low-ball assumption answered in writing.

If you want a useful outside perspective on negotiation posture, Bell Law has a solid overview of effective settlement negotiation strategies that aligns with the same basic reality. The side with the better preparation usually controls the conversation.

You can win this fight. But you won't win it by sounding upset. You'll win it by becoming hard to ignore.

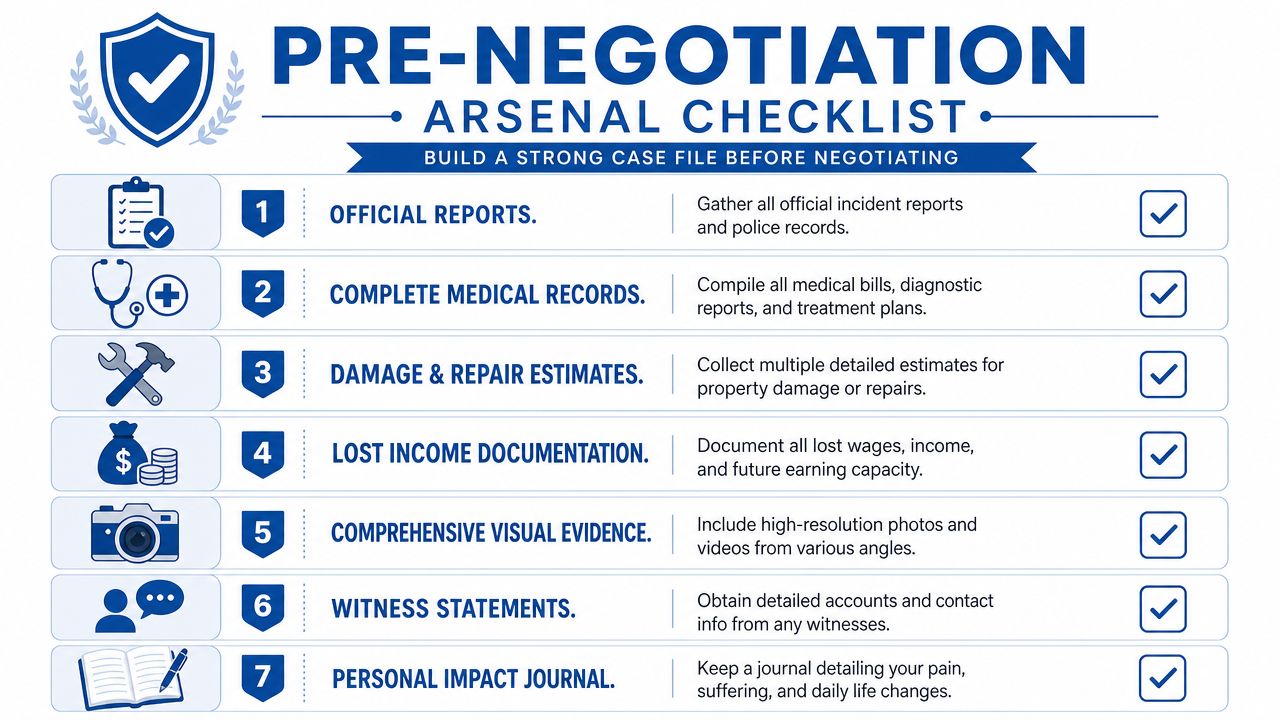

Build Your Pre-Negotiation Arsenal

Before you push back on the number, build the file that makes your pushback expensive to dismiss.

Your file has to beat their file

Insurers often work from limited inspections, narrow scopes, and pricing assumptions that favor them. If your documentation is thinner than theirs, you're arguing uphill. Build a claim package that answers the obvious carrier defenses before they raise them.

Start with the damage itself. Document every affected area, not just the dramatic one. In a water claim, that means the visible staining, but also flooring transitions, baseboards, cabinets, insulation, drywall cuts, and any room where moisture migrated. In a fire or smoke claim, include odor impact, HVAC contamination concerns, content damage, and cleaning versus replacement disputes.

Use independent professionals you trust. Don't rely only on the insurer's preferred vendor list. You want contractor evaluations that describe the work required, the reason it is required, and the pricing basis behind it.

Proof of Loss is not a throwaway form

Many policyholders sign whatever the carrier sends them. That's a mistake when the insurer's version understates the amount owed.

Most homeowner policies allow up to 60 days to submit a signed Proof of Loss, and if the insurer's version is inaccurate, the policyholder has the right to submit their own sworn statement of the claimed amount, supported by contractor evaluations and complete documentation, as explained in this overview of appealing an insurance claim and handling Proof of Loss issues.

If you need a deeper look at what should go into that form, review this guide on Proof of Loss requirements and common mistakes.

The Proof of Loss is where many claim disputes quietly turn. If the amount is wrong there, the rest of the negotiation often starts from the wrong number.

What belongs in a litigation-ready package

A strong property claim file isn't one document. It's a stack that works together.

A room-by-room scope

List each damaged building component and each disputed line item. Don't write "kitchen damage." Write the actual components affected and the work required.

Independent repair estimates

One detailed estimate is good. Multiple detailed estimates can be stronger when they confirm the same repair path.

Photos and video

Take overview shots and close-ups. Date them. Organize them by room or claim category.

A communication log

Keep every email, letter, text, inspection date, voicemail summary, and promised callback. Delays become easier to challenge when they're documented.

Policy excerpts

Pull the sections on dwelling, other structures, contents, business personal property, loss settlement, duties after loss, additional living expense, ordinance or law, and any appraisal language that applies.

Business records for commercial claims

If you're a business owner, preserve invoices, purchase records, lease obligations, interruption records, and vendor correspondence that shows operational impact.

A damages summary

Create a clean master sheet that ties your evidence to each amount claimed.

The purpose isn't to impress the adjuster. It's to remove their excuses.

Calculate Your True Number and Make Your Demand

The insurer's estimate is not your claim value. It's their opening position.

Start with the real cost of repair and recovery

A proper property demand starts with full scope, then moves to full cost. That means more than obvious repairs. Homeowners often miss code-related work, matching issues, debris handling, professional fees tied to documenting the loss, temporary living expenses where covered, and the practical cost of restoring the property to pre-loss condition under the policy. Business owners often miss operational loss categories because the carrier keeps the discussion fixed on visible building damage.

Replacement cost language matters here. If you're working through a dispute over valuation, this explanation of replacement cost coverage and how insurers apply it is worth reviewing before you put a number in writing.

Your calculation should be methodical:

- Building damage: line-item estimate with scope and pricing.

- Contents or business personal property: itemized where possible, supported by photos, receipts, inventories, or vendor pricing.

- Secondary and hidden costs: code upgrades, specialty trades, mitigation, and related covered expense categories.

- Time-sensitive losses: temporary housing or business interruption issues where the policy supports them.

How to set your opening demand

Once you know your minimum acceptable number, don't open there. To create room for negotiation, policyholders should demand an amount 25–100% higher than their minimum acceptable figure. For example, if a claimant's minimum acceptable settlement is $10,000, their initial demand should be between $12,500 and $20,000, based on this negotiation guidance on setting an opening demand.

That principle matters because carriers almost never treat your first number as your final number. If you open at your floor, you've done their bargaining for them.

Ask for a supported number, not an emotional number. High without proof gets ignored. High with documentation gets negotiated.

What a strong demand letter includes

A good demand letter doesn't ramble. It frames the dispute in a way the adjuster, supervisor, or outside counsel can evaluate quickly.

Include these elements:

- The opening summary: the amount demanded, the date of loss, the claim number, the property address, and a short statement of the core dispute.

- Coverage position: identify the policy sections supporting payment, without over-arguing.

- Scope dispute: list what the carrier omitted, underpriced, or misclassified.

- Supporting evidence: contractor estimates, photos, expert reports, invoices, moisture findings, contents support, and any business records.

- Deadline for response: make them respond on a schedule, not whenever they feel like it.

- Written confirmation request: ask them to identify every reason for disagreement in writing.

If you're learning how to negotiate settlement in a property claim, the dispute enters a serious phase. Your demand should tell the carrier one thing clearly. This file is organized, supported, and headed somewhere if they keep low-balling it.

Counter Common Insurer Tactics and Low-Ball Offers

Once the low offer arrives, many policyholders make the same mistake. They react to the number instead of attacking the reasoning behind the number.

Low-ball offers are often a test

An unreasonable first offer is often designed to move you, not to reflect the actual value of the loss. If you immediately drop your demand, you've told the adjuster that your own number wasn't firm.

When an insurance adjuster presents an unreasonably low first offer, policyholders must not immediately lower their demand. Instead, they should demand specific justifications for the low number and formally reply to each factor cited, according to Nolo's guidance on negotiating with an insurance company.

That means your next move is not, "Can you do a little better?" Your next move is, "Identify each omitted item, pricing basis, exclusion, depreciation basis, causation position, and inspection finding supporting your offer."

Insurer Tactics vs. Your Counter-Moves

| Insurer Tactic | What It Looks Like | Your Counter-Move |

|---|---|---|

| Scope reduction | The estimate ignores rooms, contents, code work, overhead, or specialty trades | Send a room-by-room rebuttal with contractor support and photos tied to each omission |

| Pricing suppression | The carrier uses lower market pricing or bare-minimum repairs | Request the pricing basis in writing and submit competing estimates that explain why the work costs more |

| Delay by repetition | New adjuster, repeat inspection, same unanswered questions | Confirm every delay in writing and ask for a claim decision on disputed items by date certain |

| Preferred vendor steering | You're pushed toward insurer-friendly contractors | Use your own qualified contractors and require the carrier to explain in writing why their scope is different |

| Policy jargon overload | The adjuster cites vague exclusions or partial coverage language | Ask them to quote the exact policy language and identify how they say it applies to each line item |

| Low first offer anchoring | They start far below the documented loss to reset expectations | Reject the anchor, hold your demand, and rebut their reasoning point by point |

| Divide-and-conquer negotiation | They settle tiny items while bigger disputes stay unresolved | Press the major items first so the claim doesn't get trapped in side issues |

How to answer without giving ground

Use a written rebuttal that is calm, short, and specific. A useful structure looks like this:

- State the disagreement clearly: "I dispute your estimate because it omits covered damage and understates the cost to restore the property."

- Demand the reasoning: ask for the factual and policy basis for each reduction.

- Answer line by line: one omitted item, one correction, one attachment.

- Preserve pressure: request a revised estimate or written denial of each disputed item.

Another move works well in larger files. Tackle the major items first. Veritext notes that one productive settlement method is to tackle the big stuff first by resolving substantial items before the smaller ones, which helps create momentum and avoids stalls, as described in this discussion of stalled insurance settlement negotiations. In property claims, that can mean roof scope, major interior rebuild, or primary business equipment before fighting over minor trim or finish details.

If the carrier sent a weak estimate, your job isn't to act offended. Your job is to make that estimate hard to defend.

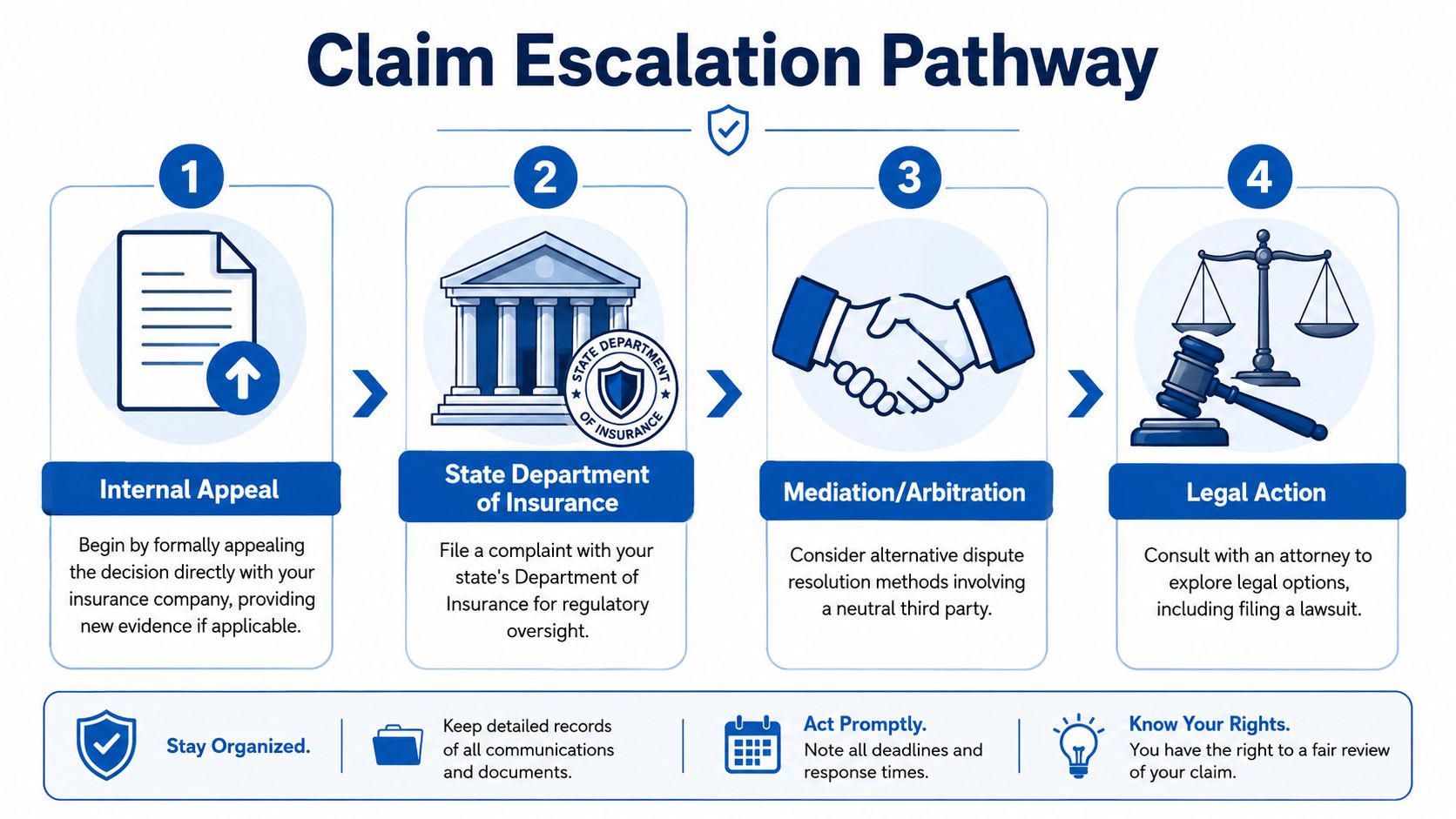

How to Escalate When Your Claim Is Denied or Stalled

You send photos, contractor estimates, moisture readings, and a clear rebuttal. Then the carrier goes quiet for two weeks, asks for documents you already sent, or repeats the same denial language without answering your evidence. That is the point where a routine negotiation turns into an escalation file.

A good escalation is controlled and documented. Angry calls rarely help. A clean paper trail does. In North Carolina and Virginia, unrepresented policyholders start at a disadvantage because the carrier controls the process, the timing, and often the first draft of the facts. The fix is to make your claim look trial-ready before anyone files suit.

Start with a formal appeal that fixes the file

Your first move is a written appeal that does more than say, "I disagree." It should identify each disputed item, attach the supporting documents, cite the policy language where you can, and ask for a written response to each point. If you need a framework, this appeal guide for insurance claim disputes is a practical place to start.

Ask for specific action. Request a reinspection. Request supervisor review. Request a revised estimate or a written denial for each item still in dispute.

That matters because a scattered file is easy to ignore. A disciplined file is harder to dismiss.

Escalate in steps, not all at once

Most stalled property claims move through a predictable ladder:

- Formal written appeal: correct the record and answer the carrier's stated reasons.

- Supervisor review: ask for a claims manager to review scope, pricing, causation, or depreciation issues.

- Appraisal or mediation, if the policy allows it: useful for valuation disputes, less useful when coverage itself is denied.

- Public adjuster involvement: bring in outside claim support when the file needs stronger scope, pricing, and claim management.

- Legal review: appropriate when the facts suggest unfair claim handling, bad faith, or a denial that does not match the policy or evidence.

Each step should build on the last one. Do not restart the dispute from scratch every time a new person touches the file. Carry forward the same chronology, exhibits, and disputed items so the carrier sees a record that is organized for scrutiny.

Use North Carolina law carefully

North Carolina gives policyholders meaningful remedies when an insurer handles a claim unfairly. As explained in this analysis of North Carolina insurance bad-faith and unfair practice claims, N.C. Gen. Stat. § 75-1.1 can support treble damages and attorney's fees in the right case.

That does not mean every underpayment turns into a lawsuit. It means the carrier should understand that delay, evasive explanations, selective readings of the policy, and unsupported denials can have consequences beyond the amount of the estimate. I have seen the tone of a claim change once the insurer realizes the file is organized, dated, and ready for outside review.

Be careful here. Throwing around legal threats too early can make you look unserious if the file is still thin. Build the record first. Then raise the issue in a measured way.

Delay is part of the fight

Some carriers wear claimants down by stretching the timeline. They ask for one more photo, one more invoice, one more inspection, then go silent again. The answer is not more phone calls. The answer is deadlines in writing.

Set a response date in each letter. Confirm every call by email. Number your attachments. If they request material you already sent, resend it the same day and note the earlier submission date. This sounds basic, but it changes the file. You are no longer arguing from memory. You are proving a pattern.

That is how unrepresented claimants start leveling the field.

Flood claims are a separate track

Do not treat a flood loss like a standard homeowners claim. Flood disputes often run through FEMA rules, the National Flood Insurance Program, or a Write Your Own carrier, and those files are much less forgiving on proof and timing.

In flood claims, small paperwork mistakes can cost real money. Scope disputes, causation disputes, and proof of loss issues need close attention early. If your loss involves both flood and non-flood damage, keep those categories clean from day one. Mixed-cause losses can become a mess fast when the file is sloppy.

Escalation works when the insurer sees a claimant who is prepared, specific, and persistent. That is the goal. Not noise. Not bluffing. A record that is hard to defend against.

Claim Help Is Here with For The Public Adjusters

Property claim negotiation is exhausting because the insurer controls information, timing, and often the first draft of the story. You don't have to accept their version of events. You can challenge scope errors, reject low-ball pricing, dispute a denied payment position, and escalate when the claim stalls.

That said, many policyholders reach the point where handling the fight alone no longer makes sense. A licensed public adjuster changes the equation by documenting the loss in a way the carrier has to answer, preparing a stronger estimate, organizing the file, and negotiating from the policyholder's side only.

For The Public Adjusters, Inc. represents homeowners and business owners, not insurance companies. The firm works on dwelling and commercial property claims involving water, fire, smoke, wind, hail, hurricane, tornado, theft, and vandalism losses in North Carolina and Virginia. That focus matters because property claims are won on scope, valuation, coverage interpretation, and persistence.

Clients say that communication, responsiveness, and detailed claim support are what made the difference when their carriers delayed or underpaid. If you're dealing with a denied claim, a low-ball offer, or an adjuster who keeps moving the goalposts, getting experienced claim help can stop the slide and put pressure back where it belongs.

Have your water damage claim questions answered at NO COST. Call 919-400-6440 to speak with a licensed Public Insurance Adjuster or Contact Us here with questions. WE Work For YOU… NOT Your Insurance Company!

If your homeowners or commercial property claim has been delayed, denied, or low-balled, For The Public Adjusters, Inc. can review the damage, the estimate, and the carrier's position, then help you build a stronger dispute strategy for recovery.