When your insurance company hits you with a denial or a laughably low offer, it’s not just frustrating—it’s their opening move. To dispute an insurance claim, you can’t just make a phone call. You have to formally challenge their decision in writing, build a case they can’t ignore, and negotiate from a position of strength, escalating the fight when they won’t budge.

This isn’t a simple conversation. It’s a strategic battle to make your insurance company honor the policy you paid for.

Why You Have to Fight Back When Your Insurance Company Says No

Feeling completely powerless after your homeowner or business insurance company lowballs or outright denies your claim is a normal reaction. Let’s be clear: massive insurers like State Farm and Allstate didn’t build their empires by happily paying claims in full. They often use confusing policy language, frustrating delays, and weak excuses to wear you down until you either give up or accept a fraction of what you’re truly owed.

This guide is your battle plan. It’s built to give you the real-world strategies you need to challenge their decision, build an undeniable case, and take back control of your claim.

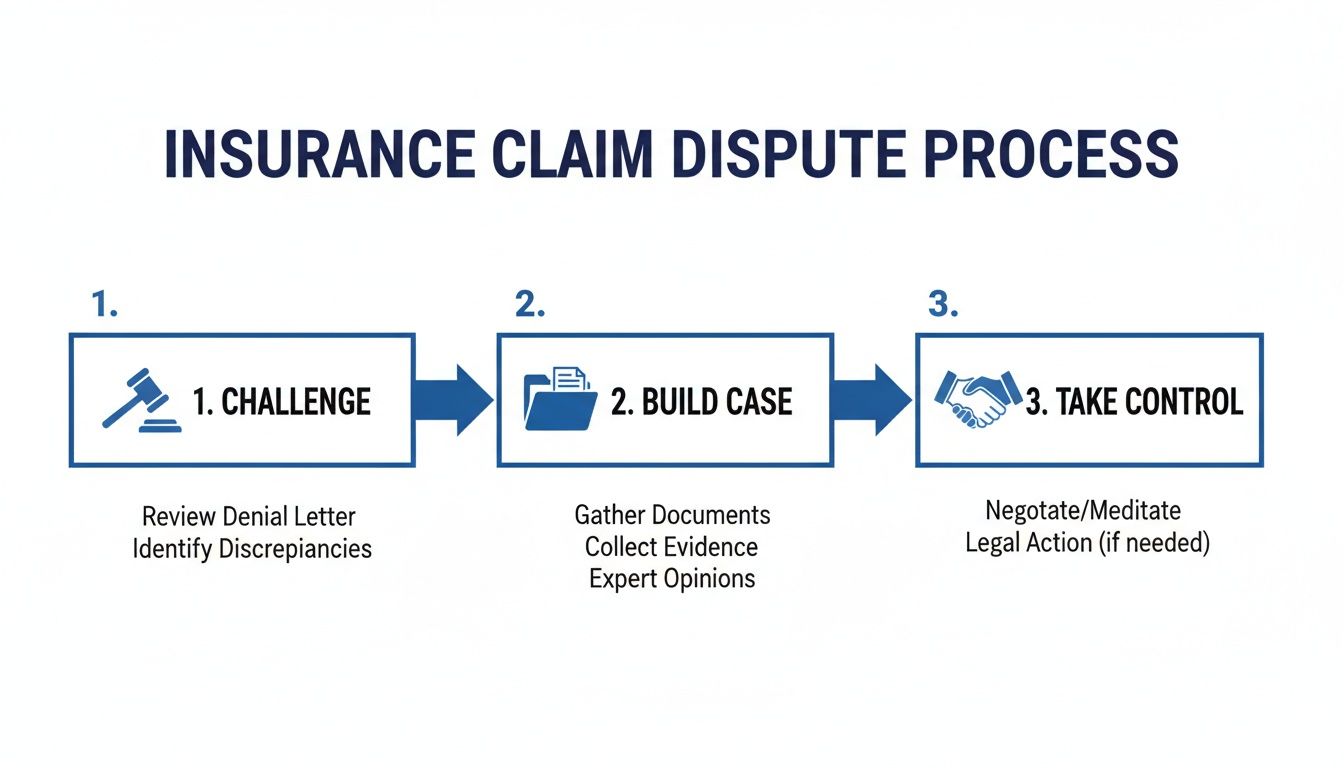

Here's a bird's-eye view of what it takes to successfully dispute an unfair claim decision.

This process really boils down to three key phases: challenging their initial decision, backing it up with solid evidence, and then taking control through smart negotiation or, if needed, escalation.

Getting Inside the Insurer's Head

You have to understand one crucial thing: your insurance company is a for-profit business. Their adjusters are trained to protect the company's money, not yours. They are banking on you being too intimidated, too tired, or too overwhelmed to fight back.

From where they sit, every single dollar they don't pay you is a dollar that goes straight to their bottom line. This fundamental conflict of interest is exactly why you need to know how to dispute a claim effectively. If you want a deeper dive into the initial steps, especially for specific damage types, this guide on navigating the roof insurance claim process is a great resource.

When You Need an Advocate in Your Corner

The moment your insurer denies or underpays your claim, the playing field is no longer level. They’ve got teams of adjusters, lawyers, and experts on their side. You’ve got a policy you can barely understand and a mountain of stress. This is precisely when a professional advocate becomes non-negotiable.

A public adjuster works only for you, the policyholder. Their entire job is to level that playing field. They take over the whole frustrating dispute process—from dissecting your policy and meticulously documenting the damage to going head-to-head with the insurer in negotiations.

If you’re wondering what that looks like, our guide explains exactly what a public adjuster can do to secure the settlement you are actually entitled to. You don't have to go into this fight alone.

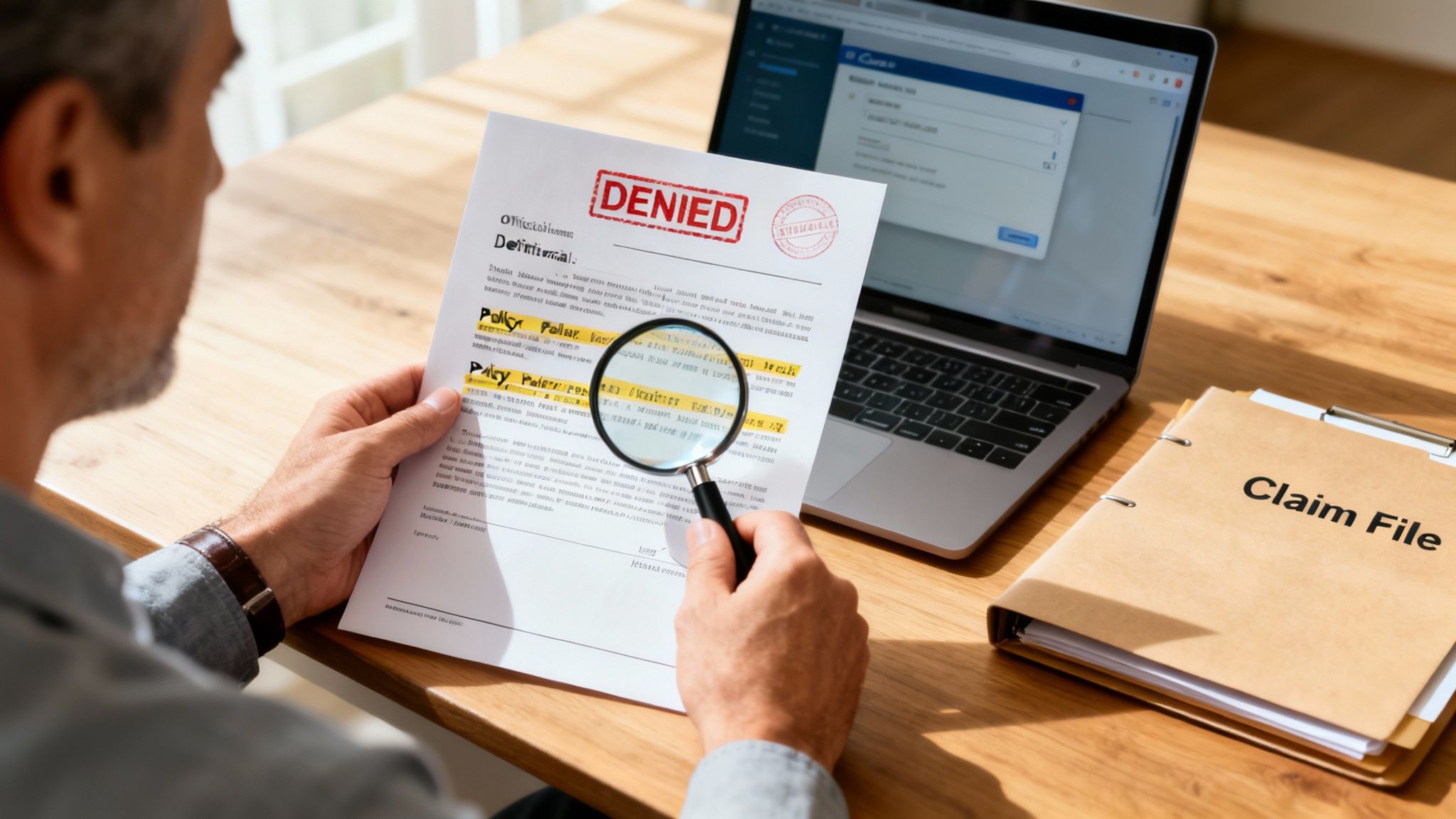

Decoding the Denial Letter and Your Claim File

Your fight to dispute an insurance claim officially kicks off with a single document: the denial letter. Let’s be clear, this letter isn't just a simple "no." It’s the insurance company’s opening salvo, a carefully crafted argument often packed with vague language, confusing legal jargon, and specific policy citations. It's designed to make you feel overwhelmed and give up right then and there.

But this letter is also their first mistake. It hands you the exact roadmap you need to dismantle their entire case. Your job is to treat it like a puzzle, pinpointing the exact policy terms, conditions, or exclusions they are banking on to justify their lowball offer or outright denial.

You Have a Right to Your Entire Claim File

The denial letter is only what they want you to see. The real story—the adjuster's private notes, internal emails, expert reports, and all the photographs—is buried in your complete claim file. You have an absolute right to this file, and you need to formally request it in writing. Don't ever accept a verbal "no" to this request.

Sending a formal, written demand for your full claim file does two critical things:

- It gives you priceless intelligence. You get a backstage pass to the adjuster's thought process, the photos they took (or conveniently didn't take), and any reports they paid for.

- It signals you're not a pushover. This is a formal step that tells the insurance company you are preparing a serious, methodical challenge. It shows them you won't be easily intimidated.

This pile of documents is the foundation of your entire dispute. More often than not, it reveals the exact inconsistencies, overlooked evidence, or biased assessments you can use to build a powerful counter-argument.

Tearing Apart Their Flawed Arguments

Once you have the denial letter and the claim file in hand, the real work begins. You have to become a detective, cross-referencing every single point they make with the actual language in your homeowner's or business owner's policy. Giant insurers like Allstate and State Farm are masters at twisting their own policies to their advantage.

A favorite tactic is citing a policy exclusion completely out of context. For instance, they might deny a water damage claim by pointing to a "long-term seepage" exclusion, conveniently ignoring that the damage was clearly caused by a sudden pipe burst—which is a covered peril. They are betting you won't know the difference.

This isn't just a rare occurrence; it’s a massive problem. A 2022 study revealed that 31% of property claimants were unhappy with how their claim was handled. This widespread dissatisfaction puts up to $34 billion in premiums at risk annually. If you want to dig deeper, you can discover more insights about the frequency and impact of denied claims and see just how many people are in the exact same boat as you.

Case Study: The Smoking Gun in the Adjuster's Notes

A small business owner in North Carolina saw their fire damage claim brutally underpaid. The insurance company's adjuster insisted that most of the inventory damage was due to pre-existing neglect, not the fire and smoke.

The owner was crushed. But after we were hired, our first move was to demand the full claim file. Buried deep in the adjuster's own notes was a short entry from his initial inspection: "inventory appears well-maintained, significant smoke damage throughout." That one sentence completely contradicted the official reason for their insulting offer.

Armed with this internal contradiction, we proved the insurance company was acting in bad faith. The claim wasn't just reopened—it was ultimately settled for more than four times the original offer. This is a perfect example of how the claim file can hide the "smoking gun" you need to win.

Building an Overwhelming Evidence Package

When it's time to dispute a claim, understand this: your opinion means absolutely nothing to the insurance company. Their adjuster’s opinion is the only one they care about, and it's almost always engineered to save them money.

To force their hand, you have to stop arguing and start proving. It’s about building an evidence package so overwhelming, so undeniable, and so meticulously organized that it leaves them no room to hide behind their flimsy excuses. You're not just presenting facts; you're building a fortress of proof they simply cannot breach.

The goal is to make it more difficult, expensive, and legally risky for them to keep fighting you than it is to just pay what they rightfully owe.

Go Beyond Their Preferred Vendors

The first move is to get your own independent repair estimate. Your insurer will almost certainly push you toward their "preferred vendors." Don't fall for it. This isn't a friendly recommendation; it's a trap.

These contractors have cozy, ongoing relationships with the insurance company. Their real job is to keep the insurer happy by churning out low-ball estimates, not to make your property whole again.

You must hire your own trusted, licensed, and independent contractor to write a detailed, line-item estimate. This document becomes your financial anchor, outlining the true scope of work and the actual cost of materials and labor in your area. It's the single most important piece of evidence showing just how badly the insurer is shortchanging you.

Document Everything Visually

In a property damage claim, photos and videos are your best weapons. The carrier’s adjuster—whether from State Farm, Allstate, or anyone else—might snap a few quick pictures and call it a day, conveniently missing the less obvious damage.

Your job is to create a visual record that is impossible to dispute.

- Take more photos than you think you need. Get wide shots of entire rooms, then zoom in on every single crack, stain, and piece of damaged property.

- Video is even better. Do a slow walkthrough of the damaged areas, narrating what you see. Describe the smell of smoke or the dampness in the air. This adds a layer of brutal reality that a static photo just can't convey.

- Dig up "before" photos. If you have pictures of your home or business from before the disaster, they are solid gold. They instantly shut down any argument about pre-existing damage.

Case Study: The Six-Figure Settlement Hidden in the Walls

We worked with a Virginia homeowner whose water damage claim was flatly denied by their carrier. The company adjuster insisted the damage was minor and superficial. But we brought in an expert who used an infrared camera to reveal extensive, hidden water damage and mold festering inside the walls. This visual evidence, which the company adjuster "missed," completely turned the tables. The claim went from a zero-dollar denial to a six-figure settlement that paid for a full remediation and rebuild.

The Paper Trail Is Your Lifeline

Every dollar you spend, every mile you drive, and every minute you waste dealing with this claim needs to be documented. You're creating a paper trail that substantiates every single part of your dispute.

Start a dedicated folder—physical or digital—and become obsessed with record-keeping.

To build a strong case, you need to collect and organize specific types of evidence. Here's a checklist to guide you.

Your Essential Evidence Checklist

| Evidence Category | What to Collect | Why It's Critical |

|---|---|---|

| Contractual Documents | Your full insurance policy, declarations page, all endorsements, and the claim denial/underpayment letter. | This is the legal contract. You need to know exactly what is covered and how the insurer is violating its own terms. |

| Independent Estimates | Detailed, line-item estimates from at least two reputable, independent (non-insurer-preferred) contractors. | This is your primary weapon against a lowball offer. It establishes the true, market-rate cost of repairs. |

| Visual Proof | Hundreds of photos (wide shots and close-ups), narrated video walkthroughs, and any "before" photos of the property. | Visuals are undeniable. They prove the extent and severity of the damage in a way words cannot. |

| Financial Records | Receipts for all related expenses: temporary repairs, tarps, cleaning supplies, hotel stays, meals (ALE), etc. | This documents your out-of-pocket losses and substantiates your claim for Additional Living Expenses. |

| Communications Log | A detailed log of every phone call, email, and letter with the insurer. Note dates, times, names, and a summary. | This creates a timeline and proves who said what and when, preventing the insurer from "forgetting" conversations. |

| Formal Submissions | Copies of all documents you send to the insurer, especially the crucial Proof of Loss form. | This creates an official record of your compliance and the information you provided, leaving no room for dispute. |

This organized collection of evidence does more than just support your claim. It sends a clear message: you are serious, you are organized, and you are not going away. That’s the kind of policyholder an insurance company thinks twice about fighting.

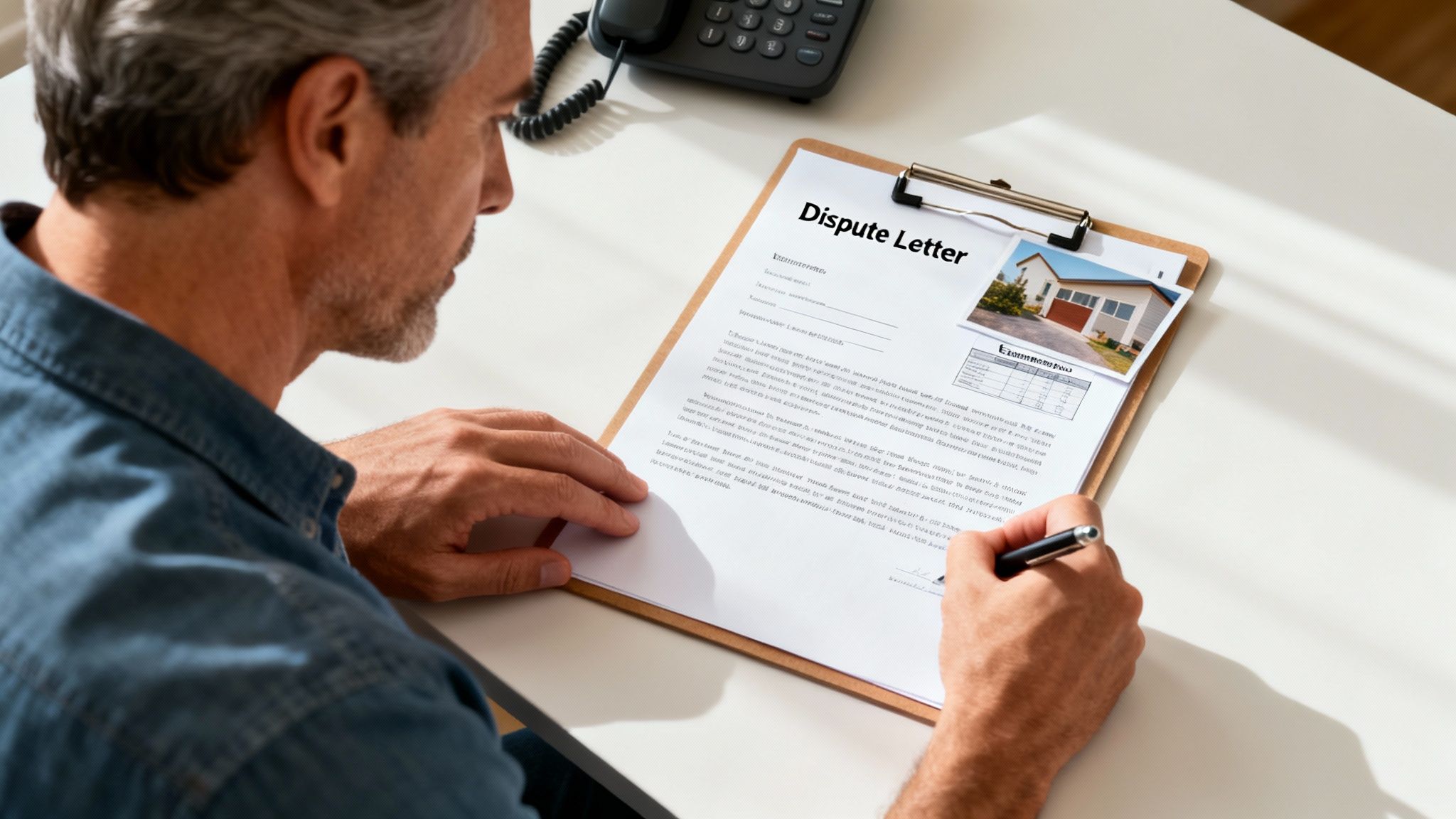

Crafting a Powerful Dispute Letter and Navigating Negotiations

Alright, you've put in the hard work and your evidence package is solid. Now it’s time to switch from defense to offense. You’re no longer just gathering proof; you’re building a rock-solid argument.

The next step is to channel all that meticulously organized evidence into a formal dispute letter. This isn't just a complaint—it's your official challenge. This document puts the insurer on notice that you reject their decision and are fully prepared to fight for what you're rightfully owed.

Think of this letter as a strategic weapon. It needs to be firm, professional, and structured in a way that’s impossible for them to simply dismiss. The goal is to systematically dismantle their denial or lowball offer and build an undeniable case for your claim. Always, and I mean always, send this via certified mail with a return receipt requested. That creates a legal paper trail proving they received it.

Structuring Your Dispute for Maximum Impact

An effective dispute letter follows a clear, logical path. This isn't about emotion; it's about presenting cold, hard facts in a way that corners the insurer. Make sure your claim number, policy number, and the date of loss are right at the top for easy reference.

Here’s how you frame your argument:

- State Your Purpose Clearly: Open by stating you are formally disputing their decision (whether it’s a denial or an underpayment) from their letter dated [Date of their letter]. Be direct.

- Counter Their Points One by One: Go through their denial letter and attack each of their reasons head-on. For instance, "You stated [their exact reason for denial], however, this is incorrect because [your counter-argument]."

- Cite Your Evidence: For every single point you make, you must reference the specific evidence you've gathered. Use phrases like, "As documented in the attached independent estimate from [Contractor's Name]…" or "Please refer to the enclosed photographs timestamped [Date]."

- Quote Your Policy: This is a total power move. Find the exact language in your insurance policy that supports your position and quote it directly. This shows them you've not only read the contract but you know how to use it against them.

When you methodically tear down their arguments and back up your own with concrete proof and contractual language, the entire dynamic shifts. You’re no longer just another frustrated policyholder; you're an organized, credible opponent they have to take seriously.

Shifting into the Negotiation Phase

Once you send that letter, the ball is back in their court. Their response will tell you everything. Often, a well-documented and forceful dispute will get your file kicked up the ladder to a new, more senior adjuster. This is where the real negotiation begins.

Remember, insurance adjusters are trained negotiators. They have a playbook of tactics designed to control the conversation and pressure you into accepting less than you deserve. They might use long, awkward silences to make you uncomfortable or try to downplay your evidence as irrelevant. You have to be ready. Our guide on how to negotiate with an insurance adjuster goes deep into the strategies you need to handle these high-pressure conversations.

Key Takeaway: Never, ever accept their first offer after you’ve sent a dispute letter. It is almost never their best offer. Your response should always be, "Thank you for the offer. I will review it against my documentation and get back to you in writing." This simple phrase buys you time and prevents you from making a snap decision based on emotion.

Shutting Down Common Delay and Denial Tactics

Insurers love to talk about the massive scale of insurance fraud—and they're not wrong, with industry estimates putting annual losses at over $300 billion. They use this as justification for tightening investigations and increasing denials, which unfortunately ends up punishing honest policyholders like you.

While fraud is a real problem, massive carriers like State Farm and Allstate often use it as a blanket excuse for their aggressive delay-and-deny tactics. You can read more about how fraud detection drives claim disputes, but don't ever let them use it to justify acting in bad faith on your valid claim.

During negotiations, get ready to hear lines like:

- "Your contractor's estimate is way too high."

- "We don't pay for that grade of material."

- "That damage was already there before the storm."

Your response must always circle back to your evidence. "My contractor's estimate reflects local market rates for labor and materials, as you can see in the detailed line items. Your estimate fails to account for [specific missing item]." You aren't arguing opinions; you're comparing documented facts.

By staying calm, professional, and relentlessly focused on your evidence, you negotiate from a position of strength, not desperation. This is how you dispute an insurance claim and win.

When You Need to Escalate the Fight

You sent the dispute letter. You handed over a mountain of evidence. And what did you get back? Crickets. Or worse, another insulting, lowball offer that doesn't even begin to cover your damages.

This is a classic insurance company tactic. They’re betting you’ll run out of steam, get exhausted by the fight, and just take whatever crumbs they’ve offered. This is the moment you absolutely cannot give up. It’s time to escalate.

You’ve played their game, and they've refused to hold up their end of the bargain. Continuing to argue with an adjuster who is paid to protect the company's profits is a dead end. You need to bring in a new player who changes the entire dynamic.

Hiring a Public Adjuster to Level the Playing Field

When your claim hits a wall, a public adjuster is your single most effective weapon.

Let’s be clear: the insurance company’s adjuster works for them. Their loyalty is to the insurer’s bottom line. A public adjuster, on the other hand, is a state-licensed professional who works exclusively for you, the policyholder.

Their entire job is to take over the fight. They dive deep, document the true scope of your loss with expert precision, and negotiate aggressively to get you the maximum settlement you're owed under your policy. They speak the insurance company’s language and know every trick in the book used to underpay claims.

The moment a public adjuster gets involved, the insurance company knows the game has changed. They aren't just dealing with a frustrated homeowner anymore; they're up against a seasoned pro who won't back down.

Success Story: From "Final Offer" to Triple the Payout

A restaurant owner in North Carolina had their business devastated by smoke and water damage from a kitchen fire. Their insurance company, a huge national carrier, dragged them along for months before slapping down a "final" offer of $85,000. They claimed most of the damage was pre-existing. Facing ruin, he brought us in. We immediately launched our own investigation, uncovering hidden smoke damage inside the HVAC system and structural problems the company adjuster conveniently "missed." We reopened the claim, hit them with our undeniable proof, and after some intense back-and-forth, secured a settlement of over $260,000—more than 3x their so-called final offer.

Invoking Your Policy's Appraisal Clause

Buried in most homeowner and business owner policies is a powerful tool you probably don't even know you have: the appraisal clause. This isn't some friendly mediation. It’s a formal process designed specifically to resolve disagreements over the amount of loss.

It's a structured showdown to settle the dollar amount, plain and simple.

Here’s the breakdown:

- You hire your own expert appraiser. The insurance company hires theirs.

- Those two appraisers agree on a neutral third party, an umpire.

- Your appraiser and their appraiser lay out their assessments and try to reach an agreement on the repair costs.

- If they can't agree, the dispute goes to the umpire. An agreement between any two of the three is binding.

When you and the insurer are worlds apart on the numbers, invoking appraisal is a fantastic way to break the deadlock and get a binding resolution.

Filing a Complaint with Your State's Department of Insurance

If you believe the insurance company is crossing a line and acting in bad faith—lying, using deceptive tactics, ghosting you, or just refusing to give a straight answer for a denial—it's time to report them.

You can file a formal complaint with your state's Department of Insurance (DOI). For policyholders in our area, this means the North Carolina DOI or the Virginia Bureau of Insurance. These agencies regulate insurers and are there to protect consumers.

Will the DOI force the insurer to cut you a check? Probably not. But your complaint goes on their permanent record. If the DOI sees a pattern of abuse from one company, it can trigger a formal investigation and hefty fines. That’s leverage.

When to Consider Legal Action for Bad Faith

Bringing in a lawyer is the final step, but it's a critical one when the insurer simply refuses to act fairly. If they have breached their contract with you or acted in bad faith, filing a lawsuit may be your only option.

Bad faith isn't just a disagreement over money. It's about unethical and illegal conduct.

Things like:

- Endless, unreasonable delays in handling your claim.

- Refusing to conduct a full and fair investigation.

- Deliberately misinterpreting your policy to deny coverage.

- Denying a valid claim without any reasonable justification.

The unfortunate truth is that terrible claims experiences are far too common. Global research reveals that a staggering 31% of property claimants are unhappy with how their claim was handled. That trend puts billions of dollars in premiums at risk for insurers who fail their customers. You can read the full research about these insurance industry findings to see just how big this problem is.

If your insurer has truly dug in their heels, exploring specialized legal services for insurance disputes might be the only way forward. Proving bad faith can result in damages far exceeding your original claim amount, making it the ultimate threat against an insurance company that refuses to pay what they owe.

Common Questions We Hear From People Fighting Their Insurance Claim

Going up against your own insurance company is confusing and, frankly, it can feel isolating. But trust me, you are not the first homeowner or business owner to be in this exact fight. We get calls every single day from people just like you.

Here are some of the most common questions that come up, answered straight.

How Long Do I Have to Dispute a Claim?

This is the single most critical question, and the answer can make or break your entire case. Your policy contains something called a statute of limitations—a hard deadline for filing a lawsuit against your insurer if you can't get them to pay what they owe.

In some states, this can be as short as one or two years from the date the damage occurred. Miss that deadline, and it's game over. You could have a slam-dunk case, but if you wait too long, you're barred from ever collecting a dime. It's one of the most ruthless rules in the insurance playbook, so find that date in your policy now.

Can My Insurer Drop Me for Filing a Dispute?

It’s a valid fear, and it happens. While it’s illegal for an insurance company to drop you in retaliation for filing a legitimate claim, they are absolute masters at finding other excuses to non-renew your policy later.

Suddenly, they might cite "increased risk" in your neighborhood or some other vague reason that just so happens to pop up after you challenged their lowball offer. It’s a dirty intimidation tactic. You can and should file a complaint with your state's Department of Insurance if this happens, but you need to know it's a real risk they might try to leverage against you.

What’s the Difference Between Appraisal and Mediation?

People mix these up all the time, but they serve two totally different purposes. Think of it like this:

-

Appraisal: This is a binding process strictly for arguing about the price of the damage. It’s not for debating whether something should be covered. You hire an appraiser, the insurance company hires theirs, and if they can’t agree on a number, a neutral umpire steps in to make the final call. It's a formal showdown over the money.

-

Mediation: This is basically a structured negotiation. A neutral mediator helps you and the insurer talk through the issues to see if you can find some common ground. It's non-binding, meaning the mediator has no power to force a decision. You can walk away at any time if you don’t like the offer on the table.

Is It Worth Hiring a Public Adjuster for a Smaller Claim?

One hundred percent, yes. It’s a huge misconception that public adjusters are only for catastrophic, six-figure losses. The exact same tactics an insurer like Allstate or State Farm uses to chisel you on a $200,000 claim are the ones they use on a $20,000 claim.

A good public adjuster can often find thousands of dollars in damages the company "missed" or policy coverages you didn't even know you had. In many cases, this extra money more than covers their fee. Just as important, they take the stress and the fight completely off your plate. That peace of mind alone is often priceless.

When your insurance company refuses to pay what you're rightfully owed, their "no" is not the final answer. The team at For The Public Adjusters, Inc. fights exclusively for policyholders in North Carolina and Virginia to force insurers to pay what you deserve.

Get a no-cost review of your claim today by visiting us at https://forthepublicadjusters.com.