Homeowners Claim Raleigh? You opened the letter expecting help. Instead, you got a denial, a tiny estimate, or a payment that wouldn’t fix half of what’s wrong. Meanwhile, your roof still leaks, your walls are wet, your contractor is shaking his head, and the insurance company keeps acting like you’re the problem.

You’re not the problem. Your homeowners claim is.

Insurance carriers understand that homeowners often lack the preparation to challenge a low scope, a bad causation decision, or a policy interpretation designed to shrink the payout. They count on confusion. They count on fatigue. They count on you needing your life back fast enough that you’ll sign and move on.

That only works if you let it.

Table of Contents

- Your Insurer Sent a Low-Ball Offer or Denial Now What

- Exposing the Insurer’s Playbook The Conflict of Interest

- How to Build an Ironclad Case for Your Claim Dispute

- Start with the policy before you touch the estimate

- Build the file like you’re preparing for an argument, not a conversation

- Hidden damage is where carriers save money

- What to document that carriers routinely miss

- Keep a communication log that reads like evidence

- Get independent experts when the scope smells wrong

- Organize the dispute package before you send anything

- The Flood Claim Fight FEMA NFIP and Hurricane Damage

- Claim Help When You Need a Public Adjuster to Fight For You

- Your Next Steps to Win Your Claim Dispute

Your Insurer Sent a Low-Ball Offer or Denial Now What

You paid premiums for years. Then a storm tears up the roof, a pipe bursts, or fire and smoke tear through the house. You report the loss, cooperate, wait, and then the carrier sends back a number that doesn’t match reality. Or worse, they deny it and bury the reason inside policy language they know policyholders rarely challenge.

That’s the moment a lot of homeowners freeze. Don’t.

The first offer is often the start of the fight

A low-ball offer isn’t proof your loss is small. It’s proof the insurer’s number is their number. That’s all.

I’ve seen homeowners get pushed into accepting a scope built around what the carrier wants to pay instead of what the property needs. Missing line items, stripped-out code upgrades, ignored moisture damage, partial roof repairs that won’t hold, and interior damage treated like cosmetic inconvenience instead of a covered loss. That’s not a fair adjustment. That’s cost control dressed up as claims handling.

Practical rule: Don’t treat a denial letter or first estimate like a final answer. Treat it like the insurer’s opening position.

There’s another problem most policyholders never see coming. A study of nearly 5,000 policyholders after the 2021 Marshall Fire found 74% were underinsured, and insurers’ own coverage estimates often fell short of actual rebuilding costs, according to reporting on the Marshall Fire underinsurance study. That’s not just a homeowner mistake. Insurers help create this gap, then homeowners pay the price when a claim gets cut down.

What you should do immediately

Don’t argue emotionally with the field adjuster. Document everything and force the dispute onto paper.

- Request the full basis of the decision: Ask for the estimate, photos, adjuster notes if they’ll provide them, engineering report if one exists, and the exact policy language they relied on.

- Do not sign a release: If they want closure fast, that’s usually because your bargaining power diminishes the second you sign.

- Check whether the carrier skipped damage categories: Roof, insulation, drywall, flooring, trim, contents, moisture intrusion, code issues, and loss of use all need review.

- Get help before you say the wrong thing: If you’re already in appeal territory, use a focused resource on how to appeal an insurance claim and make your next move based on evidence, not frustration.

Stop thinking like a claimant and start thinking like opposition

Your insurer has professionals on its side. Adjusters, consultants, engineers, desk reviewers. You need to stop showing up to that fight with only a phone call and a few photos from day one.

Anger is justified. Panic isn’t useful. The path forward is simple. Slow down, preserve your rights, and start building a file strong enough to make the carrier defend every omission.

Exposing the Insurer’s Playbook The Conflict of Interest

Insurance companies sell peace of mind. Claims departments protect the balance sheet. Those two things are not the same.

The conflict is baked in. Property damage accounts for over 97% of homeowners insurance claims, 1 in 18 insured homes files a claim each year, and the average payout stands at $13,962, according to LendingTree’s homeowners insurance claim data. When that many claims hit the books, insurers have every reason to control severity, shave scope, and close files cheaply.

Their adjuster is not your adjuster

The carrier’s adjuster may act friendly. That doesn’t change who signs the paycheck.

State Farm, Allstate, and other large carriers don’t send people out to maximize your recovery. They send people out to evaluate the loss through the company’s lens. That lens is built around internal estimating practices, causation arguments, depreciation, exclusions, and closure targets. Sometimes the low-ball isn’t a mistake. It’s the business model working exactly as intended.

Here’s how that shows up in real life:

- Delayed inspections: More waiting, more stress, more pressure on you to accept less just to move forward.

- Narrow scoping: They price the obvious damage and ignore the hidden damage.

- Causation manipulation: They blame age, wear, neglect, prior damage, or excluded water whenever it saves money.

- Preferred vendor pressure: They steer you toward contractors who are comfortable working inside the carrier’s budget, not your home’s actual needs.

The insurance company wants a closed file. You want a fully repaired home. Those goals collide the minute the loss gets expensive.

The denial rarely says what it really means

The letter says “excluded wear and tear,” “not sudden and accidental,” “pre-existing condition,” or “damage consistent with long-term seepage.” What it often means is this: they found a defense they think you can’t challenge.

That’s why homeowners get trapped. They think the denial is technical and final. It isn’t always either one. A causation decision can be wrong. A scope can be incomplete. A policy provision can be misapplied. And once the insurer sees you don’t understand the difference, they lean harder.

The old pressure tactics still work because homeowners still trust them

Insurers know most policyholders are juggling contractors, family, work, and temporary living arrangements. That gives the carrier an advantage.

A common pattern looks like this:

| Insurer move | What it does to you |

|---|---|

| Repeated document requests | Drains time and creates mistakes |

| Adjuster turnover | Forces you to restart the story |

| Small early payment | Makes the file look partially resolved |

| Partial acceptance | Gives them room to deny the expensive part |

If the company keeps changing representatives, asking for one more item, or issuing a payment that feels designed to calm you down instead of solve the loss, trust what you’re seeing.

You don’t beat this by being polite and passive

Be professional. Be organized. But stop assuming cooperation alone gets fair treatment.

What works is written communication, an independent scope, policy-based objections, and evidence that corners the carrier. If they omitted damage, you document it. If they misclassified the cause, you challenge it. If they underpriced the repair, you show why their estimate fails.

That’s how you flip the pressure back where it belongs.

How to Build an Ironclad Case for Your Claim Dispute

Most homeowners lose claim disputes for one reason. They rely on the insurer’s file instead of building their own.

That has to change fast. If your homeowners claim is delayed, denied, or underpaid, you need a record that is cleaner, deeper, and more persuasive than the carrier’s estimate. Not a stack of random photos. A deliberate case file.

Start with the policy before you touch the estimate

It’s common to look at the insurer’s number first. Wrong move. Read the policy first.

You need to know what coverage parts apply, what exclusions they’re likely to weaponize, whether replacement cost applies, whether ordinance or law coverage exists, and what duties after loss you still need to satisfy. If the carrier is demanding forms or proof, you need to know whether the request is legitimate and whether you already complied.

A focused guide on proof of loss requirements and documentation can help if the carrier is using paperwork as a choke point.

Build the file like you’re preparing for an argument, not a conversation

Your evidence needs to prove three things:

- What was damaged

- What caused it

- What it costs to restore properly

Miss any one of those, and the insurer has room to cut the claim.

- What was damaged: Photograph every room, every elevation, every ceiling stain, every buckled floor section, every detached shingle, every cracked flashing, every warped cabinet toe-kick, every affected personal property item.

- What caused it: Separate wind-created openings, plumbing failures, fire damage, smoke migration, and resulting water intrusion from long-term conditions the carrier will try to blame.

- What it costs: Use licensed contractors, detailed scopes, and line-item estimates. Generic one-page bids don’t hit hard enough.

Build your claim file so a stranger can understand the loss without you in the room.

Hidden damage is where carriers save money

This is one of the biggest reasons a homeowners claim gets underpaid. The insurer prices what can be seen during a quick walkthrough and ignores what requires effort.

Insurers often deny gradual leak claims as “wear and tear” even when a covered event started the problem. Hidden issues like punctured roof underlayment, damaged flashing, or failed window seals often go unlinked to the original storm event, which is exactly the gap described in this discussion of hidden hurricane damage and denial tactics.

What to document that carriers routinely miss

Use a sharper checklist than the insurer does.

- Roof system details: Don’t stop at missing shingles. Look for bruising, underlayment punctures, flashing displacement, ridge damage, vent issues, and soft decking.

- Moisture migration: Use moisture meters and, where appropriate, infrared scans to identify wet insulation, wall cavities, subflooring, and trim.

- Interior consequence damage: Ceiling staining is not the whole claim. Check paint, texture, framing exposure, insulation, cabinetry, flooring transitions, and microbial risk.

- Windows and doors: Storms can break seals, shift frames, and create openings that leak later.

- Smoke or soot spread after fire: Cabinets, HVAC runs, insulation, and porous materials can hold contamination long after the visible burn area is cleaned.

Keep a communication log that reads like evidence

A call log sounds boring until the insurer starts changing its story.

Track every phone call, email, inspection, promise, request, and missed deadline. Write down the date, time, who you spoke with, what was said, and what documents changed hands. If a desk adjuster says one thing and the denial letter says another, your log becomes your strongest proof.

A simple format works:

| Date | Person | What happened | Next action |

|---|---|---|---|

| [your date] | [name and title] | [inspection, request, statement, delay] | [what you sent or what they promised] |

Get independent experts when the scope smells wrong

Not every claim needs an engineer. Some do. Not every loss needs a specialty consultant. Some absolutely do.

Bring in the right expert when the dispute turns on a technical issue such as roof uplift, moisture mapping, smoke contamination, code compliance, or whether damage was sudden versus long term. The point isn’t to overwhelm the insurer with paper. The point is to close the loopholes they rely on.

Organize the dispute package before you send anything

Don’t dump documents into email chains and hope the adjuster sorts it out. Present a structured file.

A strong package usually includes:

- A dispute letter: Short, direct, and tied to specific omissions or errors.

- A damage index: Room-by-room or system-by-system list of disputed items.

- Photos and captions: Every image should prove something.

- Estimates and expert reports: Detailed and attributable.

- Policy references: Quote the coverage or condition that matters.

- Expense support: Temporary repairs, mitigation bills, and living expense records where applicable.

When you send it, ask for a written response to each disputed issue. Don’t let them hide behind a revised lump-sum estimate with no explanation.

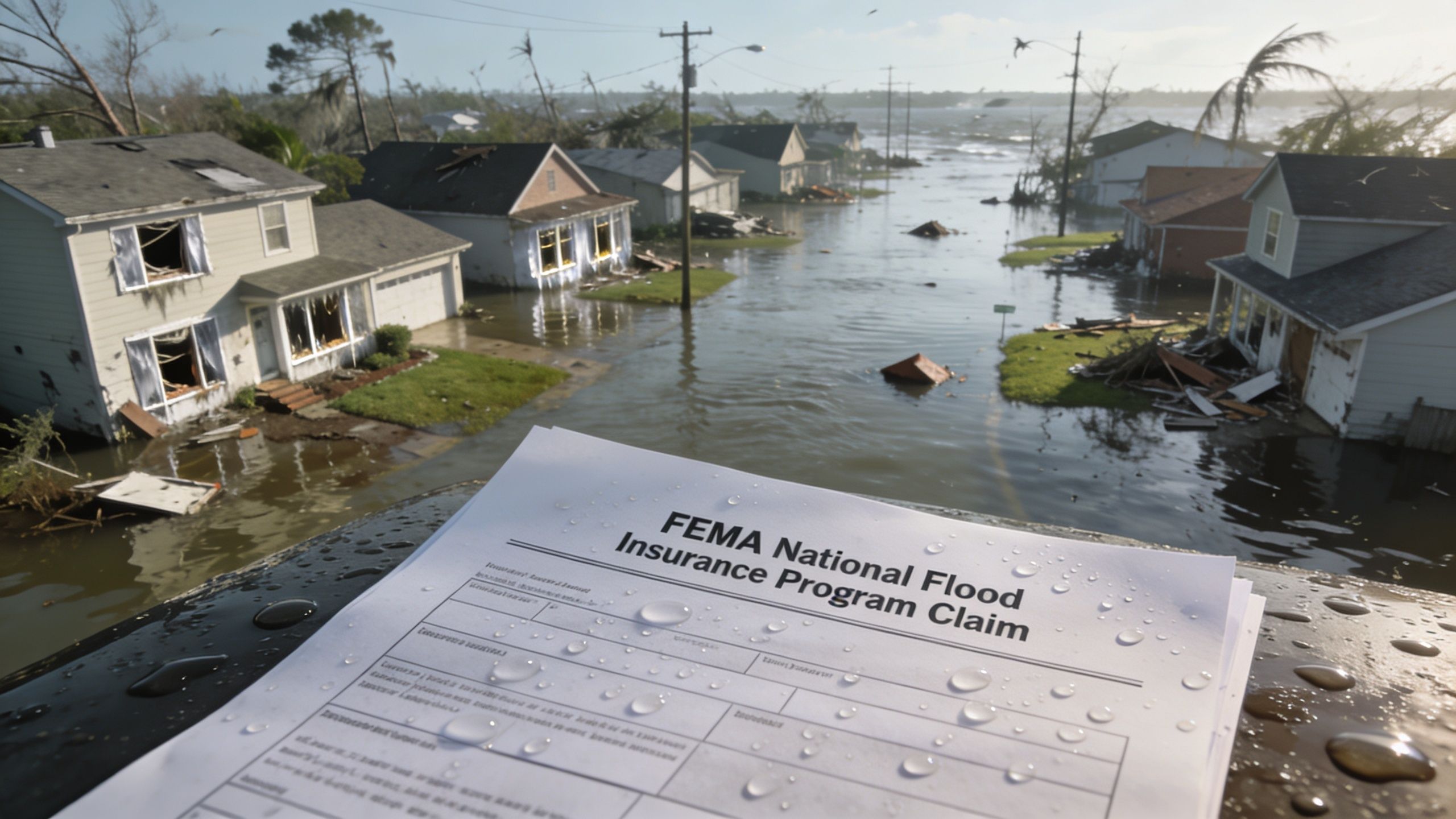

The Flood Claim Fight FEMA NFIP and Hurricane Damage

Flood claims are a different fight. Harder, slower, and more bureaucratic.

A standard homeowners policy doesn’t cover flood. If flood water caused damage, you’re likely dealing with a separate FEMA-backed National Flood Insurance Program claim, often handled through a Write Your Own company. That means two parallel battles may be happening at once. One over wind damage under the homeowners policy, and another over flood damage under NFIP rules.

Wind versus water decides who pays

After hurricanes, carriers love the wind-versus-water fight because every category they push into flood can reduce or eliminate what the homeowners carrier owes. If they can say storm surge caused it, or floodwater caused it first, they shift responsibility away from the policy you thought would respond.

That isn’t theory. Following Hurricane Helene in North Carolina, 25% of claims were closed without payment, and a major reason was insurers attributing wind-driven damage to flooding. Public adjusters counter that by proving wind damage happened first, as reported in coverage of North Carolina Helene claim outcomes and causation disputes.

You need to separate the perils immediately

Homeowners frequently lose ground here without realizing it. If a tree hits the roof, shingles blow off, or windows fail before water enters, those facts matter. A lot.

What helps:

- Time-stamped photos early: Show roof breaches, broken openings, and interior entry points before standing water changes the scene.

- Drone imagery when available: Roof damage is easier to dispute when you can see the pattern clearly.

- Moisture mapping: It helps show how water traveled and whether entry started from above versus below.

- Engineer analysis when needed: Especially when the carrier tries to flatten everything into “flood.”

If wind opened the building envelope first, that sequence can unlock coverage the insurer wants to avoid.

NFIP paperwork is strict and unforgiving

FEMA and NFIP claims don’t operate like a casual back-and-forth with a local adjuster. Deadlines, proof requirements, and category rules matter. A technical mistake can wreck an otherwise valid claim.

That’s why homeowners need discipline here. Separate flood-damaged items from wind-damaged items. Keep receipts. Preserve damaged materials when possible. Don’t assume your homeowners estimate carries over into the flood file.

If you’re trying to understand mitigation and immediate property protection after water gets into a lower level, this practical guide to basement flooding in Los Angeles is useful for the immediate cleanup mindset, even though your coverage fight under NFIP and your homeowners policy is a separate issue.

The hard part is proving sequence, not just damage

A soaked house is obvious. The order of events isn’t.

That’s why the best disputes don’t just show damage. They build a causation timeline:

| Evidence type | Why it matters |

|---|---|

| Early exterior photos | Shows wind-created openings |

| Interior water pattern photos | Helps distinguish top-down intrusion from rising water |

| Weather and event timing | Supports when the damage likely began |

| Repair and mitigation invoices | Shows what was addressed and when |

| Expert reports | Connects physical evidence to the covered peril |

If your insurer or WYO carrier is collapsing everything into flood without analyzing the building sequence, challenge it. That shortcut costs homeowners serious money.

Don’t let one claim destroy the other

Claimants often find themselves cornered. They pursue one side badly, say the wrong thing, or submit poorly organized damage categories, and the admissions in one file get used against them in the other.

Keep these boundaries clear:

- Homeowners claim: Wind, hail, falling tree impact, openings that led to interior water intrusion, and other covered non-flood perils.

- NFIP flood claim: Direct physical loss caused by flood as defined under that policy.

- Mixed losses: Need careful allocation, not guesswork.

When a hurricane loss involves both, you don’t need more optimism. You need a disciplined record and someone who knows how these files collide.

Claim Help When You Need a Public Adjuster to Fight For You

Some homeowners can handle a small, clean claim on their own. That’s not who this is for.

If your homeowners claim is denied, dragging, misclassified, or underpaid, you’re already in a technical dispute with people who do this every day. At that point, trying to “work it out” by yourself often means giving the insurer more time to control the file.

When bringing in backup makes sense

Call a public adjuster when the dispute stops being simple.

That usually means one or more of these are happening:

- The estimate is obviously short: The carrier priced a patch job, but contractors say the loss is broader.

- The denial blames exclusions: Wear and tear, long-term leakage, maintenance, or flood get used to avoid paying.

- The claim has stalled: Weeks pass, then more requests, then silence.

- The loss is large enough to hurt badly: You can’t afford to guess wrong on scope, code, or valuation.

A public adjuster works for the policyholder, not the insurer. If you need a plain-English breakdown of that role, review what a public adjuster does for property claims.

Why representation changes the leverage

The insurer already has a system. Public adjusters level it.

Wind and hail are the most common homeowners claims at 34% of total claims, with an average settlement of $11,695, and public adjuster advocacy can increase recoveries by 200-500% by challenging underpayments and invoking policy provisions such as code upgrades, according to Policygenius homeowners insurance statistics.

That matters because carriers often write estimates around bare-minimum visible repairs. A good public adjuster pushes the file back to full scope, proper causation analysis, code-related items, and complete documentation.

What a public adjuster actually takes off your plate

This isn’t just about arguing a number. It’s about taking control of the claim.

A public adjuster can:

- Inspect and scope the full loss: Not just the obvious damage the carrier chose to price.

- Prepare a detailed estimate: Usually using the same industry-standard style of line-item pricing insurers respect.

- Handle communications: So you’re not boxed into bad statements or endless phone calls.

- Challenge bad causation calls: Especially in wind, hail, water, smoke, and hurricane disputes.

- Present supplements and rebuttals: In a format the insurer has to answer.

Later in the process, seeing how an experienced advocate explains coverage disputes can help. This video gives a useful look at that mindset.

A real customer experience

| Customer Review |

|---|

|

Get suspicious when the insurer acts like your claim got complicated only after you challenged their number. That’s usually when the real review should’ve happened in the first place.

Don’t wait until you’ve boxed yourself in

The worst time to get help is after you’ve signed a release, accepted a bad scope as final, or let the carrier frame the entire loss as excluded damage.

If your file already feels slanted against you, that’s your answer. You’re not dealing with a misunderstanding. You’re dealing with a claim dispute.

Your Next Steps to Win Your Claim Dispute

You don’t need another vague checklist. You need a short list of moves that protect your money and your rights.

Start here.

Do these next

- Refuse to sign final paperwork too early: If the insurer wants a release, slow down and read every line.

- Request the full claim file support in writing: Ask for the estimate, reports, photos, and the exact policy language behind the decision.

- Get an independent scope of damage: Don’t rely on the carrier’s contractor or the carrier’s version of the loss.

- Preserve the evidence: Keep damaged materials when possible, take updated photos, and save receipts for emergency work and temporary expenses.

- Force the dispute into writing: Verbal promises disappear. Emails and letters don’t.

- Review the cause of loss carefully: A bad causation call is often the engine behind a denial or low-ball.

Don’t do these

A few mistakes can wreck bargaining power fast.

- Don’t assume the insurer explained the policy correctly

- Don’t give loose, speculative statements about what caused the damage

- Don’t accept “cosmetic” as an answer when the issue affects function, waterproofing, or safety

- Don’t let delay become the strategy that beats you

The right mindset wins more claims

A denied or underpaid homeowners claim doesn’t mean the carrier is right. It means they took a position. Your job is to challenge that position with better facts, better documentation, and better representation if the file calls for it.

The people who recover well aren’t always the people with the worst damage. They’re the people who document hard, push back early, and stop trusting the insurer to fix its own mistakes.

If you’re staring at a denial letter, a low estimate, or months of delay, act now. The claim won’t get easier because you wait. It gets harder because the insurer gets more comfortable with your silence.

If your homeowners claim has been denied, delayed, or low-balled, get a no-cost review from For The Public Adjusters, Inc.. They represent policyholders across North Carolina, inspect the loss, document the full scope, interpret the policy, and fight the carrier directly so you can stop arguing with the insurance company and start rebuilding.