You opened a claim because something in your home went wrong. A pipe burst. Wind tore shingles off. Smoke moved through rooms that never burned. You expected your insurer to step in and help you recover.

Instead, you got a denial letter, a tiny estimate, or an adjuster who keeps changing the story.

That's where most homeowners freeze. They aren't confused about the damage. They're confused about the fight. Should you push back yourself? Bring in a public adjuster? Call one of the home insurance claim lawyers in your area? If you make the wrong move at the wrong time, the insurer gains an advantage fast.

My view is simple. If the dispute is still about scope, pricing, documentation, and policy interpretation, a public adjuster is often the best first move. If the dispute has turned into a legal war, or your carrier is denying the claim outright on serious grounds, you need a lawyer. The mistake I see all the time is waiting too long to get expert help, then paying more later to clean up a preventable mess.

Table of Contents

- Your Claim Was Denied or Low-Balled Now What

- Public Adjuster vs Lawyer Your Two Main Allies

- When You Absolutely Need to Hire a Claim Lawyer

- Navigating the Legal Fight The Claim Lawsuit Process

- The Cost of Fighting Back Lawyer Fees and Payouts

- Claim Disputes in North Carolina and Virginia

- The Proactive Path For The Public Adjusters Inc

- Frequently Asked Questions About Claim Disputes

- Should I call a public adjuster before a lawyer?

- Can a public adjuster represent me in court?

- What if my insurer says the damage was pre-existing?

- Are home insurance claim lawyers worth it?

- What if I have a flood claim in North Carolina or Virginia?

- What should I do right now if my claim is stalled?

Your Claim Was Denied or Low-Balled Now What

The first bad offer usually arrives dressed up as something reasonable. The carrier's estimate looks official. The denial letter sounds confident. The adjuster says the damage is old, partial, cosmetic, or outside coverage.

That doesn't make it true.

A lot of homeowners get trapped because they assume the insurance company's first position must be close to correct. It often isn't. Insurers commonly push back by calling damage pre-existing or blaming it on neglect, and policyholders usually need records, photos, and prompt reporting to rebut that narrative, as explained in this discussion of common denial tactics and how to fight back.

The dispute usually starts with one of these moves

- A denial based on causation: The insurer says the damage came from wear and tear instead of a sudden event.

- A low-ball estimate: The check won't cover the full repair scope.

- A delay strategy: Inspections drag on, documents get requested in waves, and nobody gives you a straight answer.

- A partial payment: The carrier pays for the obvious damage and ignores the hidden damage that drives the cost.

In plain terms, the fight usually isn't about whether damage exists. It's about what caused it, how much of it is covered, and what it costs to repair correctly.

You're not the only one dealing with this

In 2020, 6% of insured homes filed at least one homeowners insurance claim, and while wind and hail were the most common, fire and lightning claims were the most severe, with an average settlement of $77,340, according to homeowners insurance claim statistics compiled by Policygenius. When that much money is on the table, disputes get aggressive fast.

Practical rule: If the insurer's explanation doesn't match what you can see in your home, don't accept the paper over the damage.

Your next move matters more than commonly understood. Don't just argue by phone. Pull together your photos, contractor observations, moisture readings if available, receipts, prior maintenance records, and every claim communication. Then read what to do after an insurance claim denial before you say anything else that locks you into the insurer's framing of the loss.

A denied or low-balled claim doesn't mean the claim is dead. It means the actual claim work is finally starting.

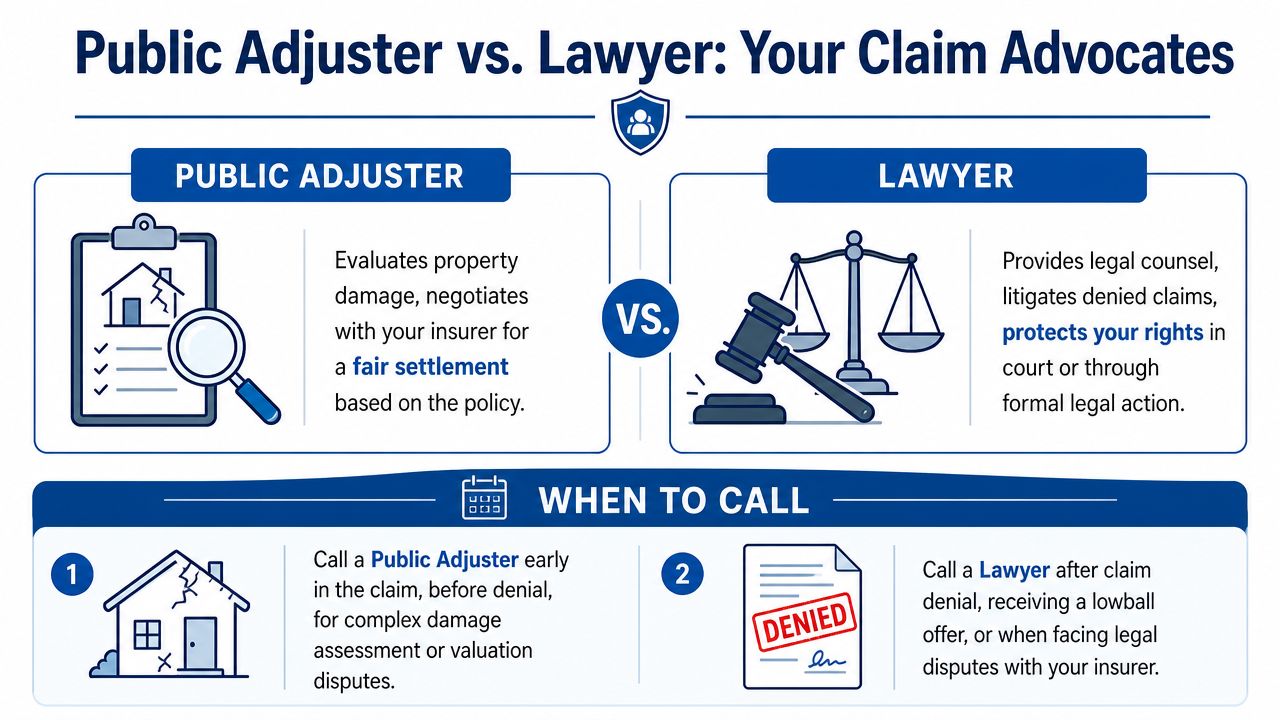

Public Adjuster vs Lawyer Your Two Main Allies

You open the insurer's letter expecting a fair number. Instead, the estimate barely covers cleanup, ignores half the damage, and leaves you wondering whether you need a lawyer right now. Usually, you don't. Usually, you need someone to rebuild the claim correctly before the dispute hardens into a legal fight.

A public adjuster and a lawyer both protect the policyholder, but they do different jobs. Confusing the two costs money and gives the carrier an advantage.

What each one actually does

A public adjuster handles the claim itself. That means inspecting the loss, reading the policy against the facts, documenting damage the carrier missed, building a credible repair scope, pricing the work, and negotiating from evidence instead of frustration. That middle step matters. Many bad claims become lawsuits only because nobody forced the insurer to deal with the full facts early.

A lawyer handles legal rights and legal pressure. If the dispute turns into a fight over policy wording, alleged misrepresentation, bad-faith conduct, examinations under oath, or a lawsuit, that is lawyer territory.

Here's the practical rule. If the claim is still fixable through better documentation, stronger estimating, and sharper negotiation, start with a public adjuster. If the insurer has moved the dispute into a legal or quasi-legal posture, bring in counsel.

Public Adjuster vs Home Insurance Claim Lawyer

| Factor | Public Adjuster | Home Insurance Claim Lawyer |

|---|---|---|

| Primary role | Documents, values, and negotiates the property claim | Gives legal advice and pursues legal remedies |

| Best time to call | Early, when the carrier is under-scoping, delaying, or underpaying | After denial, legal threats, coverage disputes, or formal escalation |

| Main focus | Damage scope, repair cost, claim presentation, policy support | Denials, exclusions, legal interpretation, bad faith, litigation |

| Typical work product | Estimates, inventories, photos, expert coordination, claim package | Demand letters, coverage analysis, pleadings, discovery, court filings |

| Court representation | No | Yes |

| Best use case | Keeping a claim dispute from getting worse | Forcing action after negotiation stops working |

That distinction matters even more in places like North Carolina and Virginia, where homeowners often have a real chance to correct the claim before paying a lawyer to prepare for litigation.

The smartest first move is usually the professional who can strengthen the claim, not the one who prepares the lawsuit.

If you are weighing legal help in North Carolina, this guide on homeowners insurance claim lawyers in NC helps you compare when counsel makes sense and when a claim advocate should come first.

When You Absolutely Need to Hire a Claim Lawyer

There are moments when negotiation is over. Once you hit one of them, stop trying to charm the carrier into doing the right thing. Get legal help.

The average home insurance claim is around $15,100, and for claims in that range, a lawyer's 30% to 40% contingency fee may not be the best economic choice, according to Insurify's explanation of when a home insurance claim lawyer makes sense. But that same analysis points to the situations where a lawyer becomes necessary. Complex, high-value claims and outright denials are where legal firepower matters most.

Red flags you should treat seriously

Call one of the home insurance claim lawyers in your market if any of these are happening:

The carrier accuses you of fraud, concealment, or arson.

That's not an ordinary claim disagreement. That's a legal threat.The denial hangs on a technical policy exclusion.

If the fight turns on wording, definitions, endorsements, or coverage carve-outs, you need legal interpretation, not just estimating help.The insurer refuses to communicate clearly.

Endless silence, inconsistent positions, and refusal to explain the basis of denial are warning signs.The loss is large enough that a bad outcome changes your financial future.

On a major fire, structural collapse, or severe water loss, a weak response can cost far more than legal fees.

When cost stops being the main issue

Some claims are too dangerous to handle as a normal negotiation. If the carrier is trying to void coverage entirely, the entire amount may be at stake. At that point, arguing about whether an attorney's fee is ideal misses the bigger issue. You may need counsel to recover anything at all.

Use a public adjuster when the dispute is still fixable through evidence, scope, and negotiation. Use a lawyer when the insurer has made the fight legal.

If your claim file now reads like an accusation instead of an adjustment, it's time to speak with counsel.

If you're weighing that step now, review this resource on when an insurance dispute lawyer is the right move. Don't wait until deadlines, recorded statements, and bad paperwork corner you.

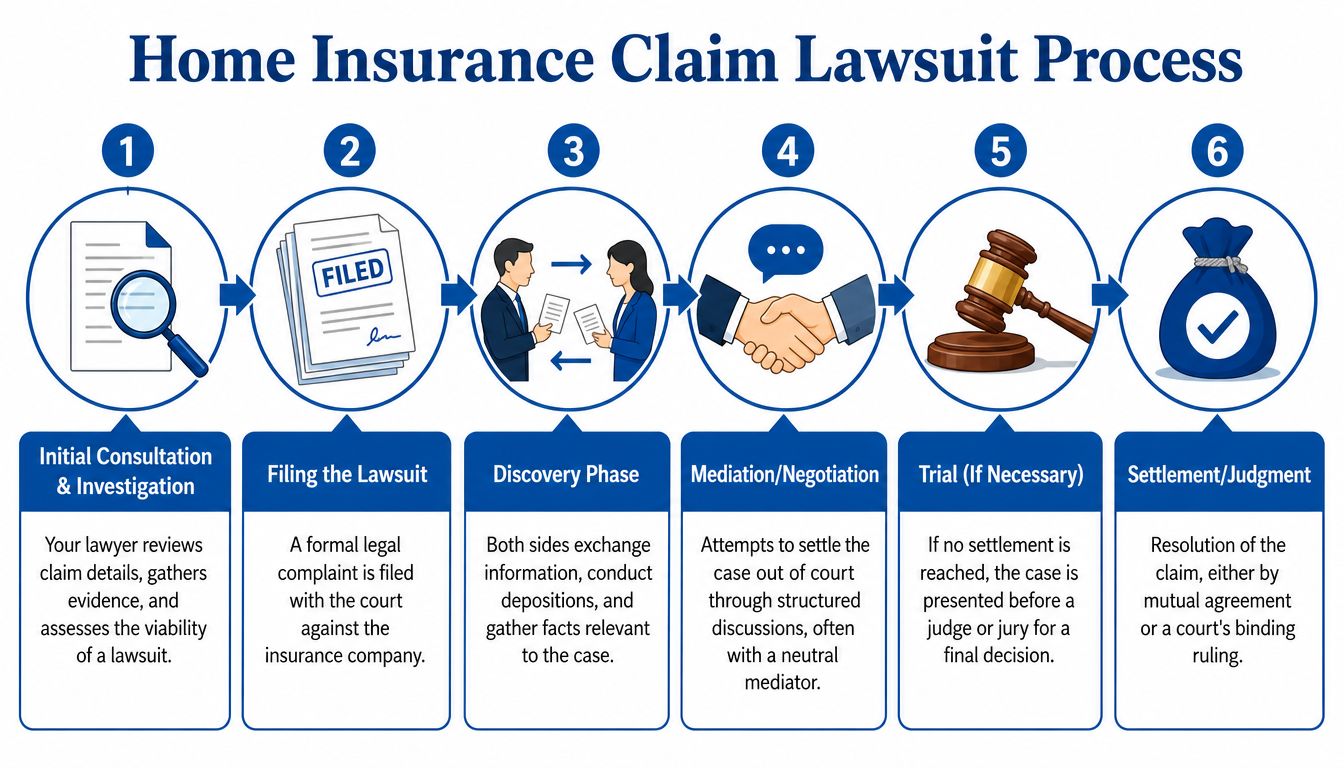

Navigating the Legal Fight The Claim Lawsuit Process

Once a lawyer takes over, the process gets more formal and more disciplined. That's good. Insurance companies are comfortable controlling messy conversations. They're less comfortable defending weak decisions under legal scrutiny.

What the process usually looks like

Most property claim lawsuits follow a recognizable path:

Investigation and file review

Your lawyer studies the policy, correspondence, estimates, reports, photos, and denial language.A demand or pre-suit push

Sometimes the insurer gets one more chance to pay correctly before suit is filed.Filing the complaint

The insurer has to answer in court, not just through adjuster emails.Discovery

During discovery, both sides exchange information. Internal claim notes, inspection reports, and expert opinions start to matter.Mediation or settlement talks

Many cases resolve here, once the carrier realizes its position won't hold up.Trial if needed

If the insurer still won't act reasonably, a judge or jury decides.

That structure matters because it changes the balance of power. The carrier now has to defend its decisions with evidence, witnesses, and testimony.

How lawyers attack weak denials

In fire and explosion cases, the best home insurance claim lawyers don't just say the insurer is wrong. They use technical standards to prove it. Lawyers rely on NFPA 921, the Guide for Fire and Explosion Investigations, to challenge biased origin-and-cause findings and establish the full extent of covered smoke, heat, and soot damage, as discussed by Liss & Earle in their property insurance claims analysis.

That matters because insurers often lean on cause-of-loss reports as if they're untouchable. They aren't. If the carrier claims to follow scientific fire investigation standards, your side can use the same benchmark against them.

Weak denials often look strong until somebody demands the insurer prove each assumption.

A good lawsuit isn't theater. It's documentation, testimony, standards, timelines, and pressure. If your claim reaches that point, the legal process stops being abstract and starts becoming a strategic advantage.

The Cost of Fighting Back Lawyer Fees and Payouts

Most homeowners ask the same question first. “How much is this going to cost me?”

That's the right question. You shouldn't hire a lawyer blindly, and you shouldn't avoid one just because legal help sounds expensive.

How contingency fees really work

Many property claim lawyers work on a contingency fee, which means they get paid from the recovery rather than billing you by the hour. That structure helps homeowners who can't or won't fund a lawsuit up front.

But contingency doesn't mean free. It means you need to understand the economics before signing anything.

Here's the practical way to understand the situation:

- Smaller disputes often don't justify legal fees. If the claim amount is modest and the dispute is mainly about scope or valuation, a public adjuster may be the more efficient first step.

- High-stakes denials often do justify legal fees. If the carrier has denied a substantial claim, recovering a smaller share of something is often better than recovering all of nothing.

- The net matters more than the gross. Don't focus only on the settlement number. Focus on what you keep after fees and costs.

A lot of policyholders also overlook the cost of delay. A dragged-out claim can stall repairs, worsen living conditions, and complicate contractor pricing. Even when legal action costs money, doing nothing can cost more.

What else you may have to pay for

Legal cases can also bring expenses beyond the fee itself. Depending on the dispute, there may be costs tied to experts, filing, records, inspections, or technical analysis. Ask about that early. Ask who advances those costs, when they're reimbursed, and whether they come out of the final recovery.

This short video helps frame the conversation about legal claim strategy and expectations:

The smart approach is blunt. If the dispute is still negotiable, use a public adjuster to maximize the claim before legal fees enter the picture. If the insurer has shut the door, calculate the likely net recovery and decide like a businessperson, not an exhausted homeowner.

Claim Disputes in North Carolina and Virginia

Your roof gets hit in a storm, the carrier sends someone out fast, and within days the file starts heading in the wrong direction. The estimate is thin. The cause of loss is framed too narrowly. Now you are reacting instead of controlling the claim.

Why local claim help matters

In North Carolina and Virginia, local experience matters because the claim is shaped early. The inspection, the first estimate, the photos in the file, and the carrier's initial theory of damage all influence what happens next. If those first steps are sloppy or one-sided, fixing the claim later gets more expensive.

That is why I push policyholders toward a public adjuster before the dispute turns into a legal fight. In both states, a good public adjuster can inspect the property, document the loss properly, challenge a weak scope, and keep the claim in the negotiation stage. That often saves you from paying a lawyer to clean up a file the insurer already hardened against you.

Virginia policyholders should pay close attention here. As noted earlier, state consumer guidance recognizes that public adjusters can represent the policyholder's interests during the claim process. That matters because it gives homeowners and business owners a real middle path between handling the claim alone and filing suit.

North Carolina policyholders face the same practical problem. Storm claims, water losses, and structural disputes can go sideways fast when the carrier controls the narrative first. Local help is not about geography for its own sake. It is about getting someone who knows the common loss patterns, the regional contractors, and the claim tactics insurers use in these states.

Flood claims are a different animal

Flood claims need a different approach. If the loss involves flood, treat it as a separate system with its own rules, forms, deadlines, and proof requirements.

That is where policyholders in NC and VA get burned. They assume a flood dispute works like a standard homeowners claim, then learn too late that the documentation standard is tighter and the process is less forgiving. Once the carrier or flood adjuster defines the damage incorrectly, reversing that position is hard.

Get qualified help early on flood losses. Start with a public adjuster who understands flood documentation and claim presentation. Bring in a lawyer if the dispute turns into a coverage fight, a deadline problem, or a serious denial that will not move.

Commercial claims raise the stakes even more. Building damage, contents, extra expense, business interruption issues, and layered policy wording can create a mess quickly. In those files, early claim control is usually the cheapest money you will spend.

The Proactive Path For The Public Adjusters Inc

The strongest claim position is built before the insurer decides what your damage is worth.

That's why I push homeowners and business owners toward early professional advocacy when the loss is serious, the damage is complex, or the carrier is already acting slippery. Waiting until you need one of the home insurance claim lawyers in your area often means you've already let the insurer define the story, the scope, and the value.

Why early advocacy changes the outcome

Professional advocacy from public adjusters or attorneys can significantly increase settlement outcomes, especially when insurers delay inspections, change adjusters, or misrepresent coverage, according to this explanation of insurer tactics and the value of expert representation. That tracks with what policyholders experience every day. Claims get smaller when nobody pushes back.

A good public adjuster doesn't just “help with paperwork.” They pressure-test the carrier's estimate, identify missing line items, document overlooked damage, and keep the claim tied to the policy instead of the insurer's convenience.

What a strong claim file looks like

A strong file usually includes:

- Clear damage documentation with photos, room-by-room detail, and supporting records

- A defensible scope of repair built from actual conditions, not shortcuts

- Policy-based arguments tied to covered loss, not emotional appeals

- Consistent communication so the insurer can't reset the claim around confusion

- Support from the right experts when causation or extent is disputed

That middle ground matters. It's where many claims are won or lost.

If the carrier still refuses to act reasonably, then legal counsel may be the next step. But the policyholder who starts with a well-built claim is in a much stronger position than the one who starts with frustration and a shoebox of receipts.

Frequently Asked Questions About Claim Disputes

Should I call a public adjuster before a lawyer?

Usually, yes. If the dispute is still about damage scope, repair cost, missing items, or policy application, a public adjuster is often the better first move. If the claim has been denied on legal grounds or the insurer is accusing you of misconduct, call a lawyer.

Can a public adjuster represent me in court?

No. A public adjuster handles the claim and negotiates with the insurer. Court representation is for attorneys.

What if my insurer says the damage was pre-existing?

You need evidence that shows the damage came from a covered event and wasn't long-term deterioration. Maintenance records, renovation photos, prior condition photos, and prompt reporting can all help counter that position.

Are home insurance claim lawyers worth it?

Sometimes. They're worth it when the dispute is high-value, legally complex, or fully denied. They're often not the first or best financial move on smaller disputes that can still be corrected through documentation and negotiation.

What if I have a flood claim in North Carolina or Virginia?

Treat flood as a separate system. FEMA and NFIP claims are not standard homeowners claims, and the dispute process can be much tougher. Get expert help early.

What should I do right now if my claim is stalled?

Stop relying on phone calls and verbal assurances. Gather every estimate, photo, letter, email, and adjuster report. Then get an expert review before you say yes to a bad payment or no to a salvageable claim.

If your homeowners, dwelling, or business owner property claim has been denied, delayed, or low-balled, get real help before the insurance company gains more ground. For The Public Adjusters, Inc. represents policyholders, not insurers, across North Carolina and Virginia. Have your water damage claim questions answered at NO COST. Call 919-400-6440 to speak with a licensed Public Insurance Adjuster or Contact Us here with questions. WE Work For YOU… NOT Your Insurance Company!