You opened the claim, waited, answered the adjuster's questions, sent photos, maybe even had a contractor walk the property. Then the carrier came back with a denial, a delay, or a settlement offer so low it won't cover the actual repair bill. That's the point where most homeowners start searching for a home insurance claim lawyer.

That search makes sense. When your roof is torn up, your kitchen is soaked, or your business property is sitting damaged while the insurer drags its feet, you want someone who knows how to fight back. But here's my blunt advice. A lawyer is not always the first or smartest move. In a lot of property claim disputes, especially low-ball disputes, the underlying problem isn't legal interpretation. It's bad estimating, incomplete scoping, sloppy documentation, or an adjuster using the carrier's numbers instead of the actual cost to repair.

You need to know the difference before you hand over a large chunk of your settlement.

Table of Contents

- Your Claim Was Denied or Low-Balled Now What

- What a Home Insurance Claim Lawyer Actually Does

- Red Flags That Your Insurer Is Fighting Your Claim

- Lawyer vs Public Adjuster The Critical Choice

- When You Absolutely Must Hire a Claim Lawyer

- The Cost of Fighting Back Fee Structures Explained

- Finding Vetted Claim Help in North Carolina and Virginia

Your Claim Was Denied or Low-Balled Now What

The storm is over, but the struggle begins when the letter arrives. Your kitchen ceiling is stained, the flooring is buckling, the contractor says the scope is bigger than you thought, and the insurance company sends back a payment that does not come close. Or it sends a denial packed with policy language clearly written to make a homeowner give up.

Do not treat that as the final word.

A denied claim and a low-ball estimate are two different problems, and that distinction matters because the right help depends on what the carrier is doing. If the dispute is about repair cost, scope, measurements, missed damage, or code upgrades, a public adjuster is often the smarter first call. If the carrier is relying on exclusions, misrepresentation allegations, late notice, or other legal defenses, you may need a lawyer fast. If you are trying to sort out which fight you are in, this guide on an attorney for a home insurance claim breaks down the difference.

The biggest mistake homeowners make is arguing with the insurer like this is still a normal customer service issue. It is not. Once the claim turns adversarial, every email, estimate, photo, invoice, and inspection note starts to matter.

What to do during the dispute phase

Start with the paper trail. Read the denial letter or estimate line by line and identify the insurer's actual position.

- Pin down the dispute type: Is the carrier denying coverage, or admitting coverage but paying far too little?

- Compare its position to your proof: Use photos, contractor estimates, mitigation invoices, receipts, inspection reports, and any expert findings to show what was missed or undervalued.

- Preserve every deadline: Appeals, proof of loss forms, and other dispute steps can have short deadlines. Some policies and claim disputes move on a tight clock, including appeal windows that can run from 30 to 90 days, as explained by CMS Law Group in its guide to disputing a homeowners insurance claim.

- Stop relying on the carrier's estimate: Their estimate is their position. It is not an objective measure of what your repair costs.

That last point matters more than homeowners realize.

In underpayment cases, the fight is often about proof, not law. The insurer's adjuster may have missed rooms, omitted line items, used low unit pricing, ignored overhead and profit, or scoped the damage as a patch job when replacement is the appropriate answer. That is usually a public adjuster problem before it becomes a lawyer problem.

Ask this before you hire anyone

Answer one question first. Is this a valuation dispute or a legal coverage dispute?

If the carrier agrees there was a covered loss but is underpaying it, get the numbers, scope, and documentation cleaned up first. That is where a strong public adjuster earns their fee. If the carrier says the loss is excluded, accuses you of violating policy conditions, or hints at fraud or bad faith issues, stop trying to negotiate your way out of it and get legal counsel involved.

Choose the professional that fits the fight. That decision can save you time, money, and a lot of avoidable damage to your claim.

What a Home Insurance Claim Lawyer Actually Does

A home insurance claim lawyer is not just someone who files lawsuits. The good ones start much earlier, and their first real job is legal analysis.

Policy language is the battlefield

The lawyer's core function is forensic policy analysis. They compare your loss documents against the policy wording to see whether the carrier's position is legally defensible. They dig into coverage grants, exclusions, duties after loss, valuation language, and the parts of the policy the insurer is leaning on to justify a denial or reduced payment.

That's different from what a field adjuster or contractor does. A contractor can tell you the roof needs replacement. A lawyer can tell you whether the insurer is misapplying the policy to avoid paying for it.

According to Merlin Law Group's discussion of insurance attorneys in California, a lawyer's core role is to cross-reference loss documentation with specific policy clauses to determine whether a denial is legally justified. That same discussion states that when lawyers intervene early, claim underpayments can decrease by 35% to 40% because insurers are pushed to recalculate damages using third-party data rather than internal estimates.

For a broader property-claim perspective, this breakdown on an attorney for a home insurance claim is worth reviewing.

A lawyer's leverage is legal pressure

Once the lawyer sees a legal problem, the strategy changes. They can build a breach of contract case, frame bad faith issues, challenge a denial based on shaky policy interpretation, and prepare the file for litigation if the carrier won't correct course.

That often includes work like:

- Reviewing carrier reasoning: Denial letters, reservation of rights letters, estimates, and internal explanations get tested against the policy itself.

- Coordinating outside experts: Lawyers may rely on independent appraisals, certified inspectors, and estimating tools such as Xactimate when the carrier's math doesn't hold up.

- Prompting serious consideration: Even before a lawsuit is filed, a credible legal threat can force a carrier to take the dispute more seriously.

A lawyer's value isn't just courtroom skill. It's the ability to turn vague insurer language into a legal issue the carrier has to answer.

If your dispute is primarily about what the policy means, legal counsel can be the right weapon. If your dispute is mostly about what the damage is worth, that's where many homeowners jump to a lawyer too fast.

Red Flags That Your Insurer Is Fighting Your Claim

When a carrier is playing fair, the process may still be slow and frustrating, but it will make sense. When a carrier is fighting your claim, the pattern feels different. Calls go unanswered. New paperwork requests appear after you already sent the same documents. The estimate ignores obvious damage. The denial letter cites exclusions that don't seem tied to what happened.

The tactics homeowners keep running into

A lot of adjuster behavior follows the same script.

- Weeks of silence: Some adjusters delay inspections or fail to return calls, a pattern described in this discussion of home insurance claim adjuster tactics.

- Low initial offers: Carriers may put out an offer that doesn't reflect real repair pricing, hoping the policyholder is too stressed to push back.

- Exclusion games: Insurers sometimes deny claims using exclusions or limitations that don't fit the loss, as outlined in this overview of insurance coverage dispute tactics.

What those red flags usually mean

Here's the part homeowners need to hear clearly. These are not random annoyances. They're pressure tactics.

If the company keeps asking for more documents without explaining why, it may be trying to wear you down. If the estimate skips line items your contractor says are necessary, the carrier may be narrowing the scope to save money. If the communication stays vague, that's often because a clear answer would expose a weak position.

If your adjuster can't explain the denial or the estimate in plain English, assume you need independent help.

Trust your instincts. If the process feels one-sided, it probably is.

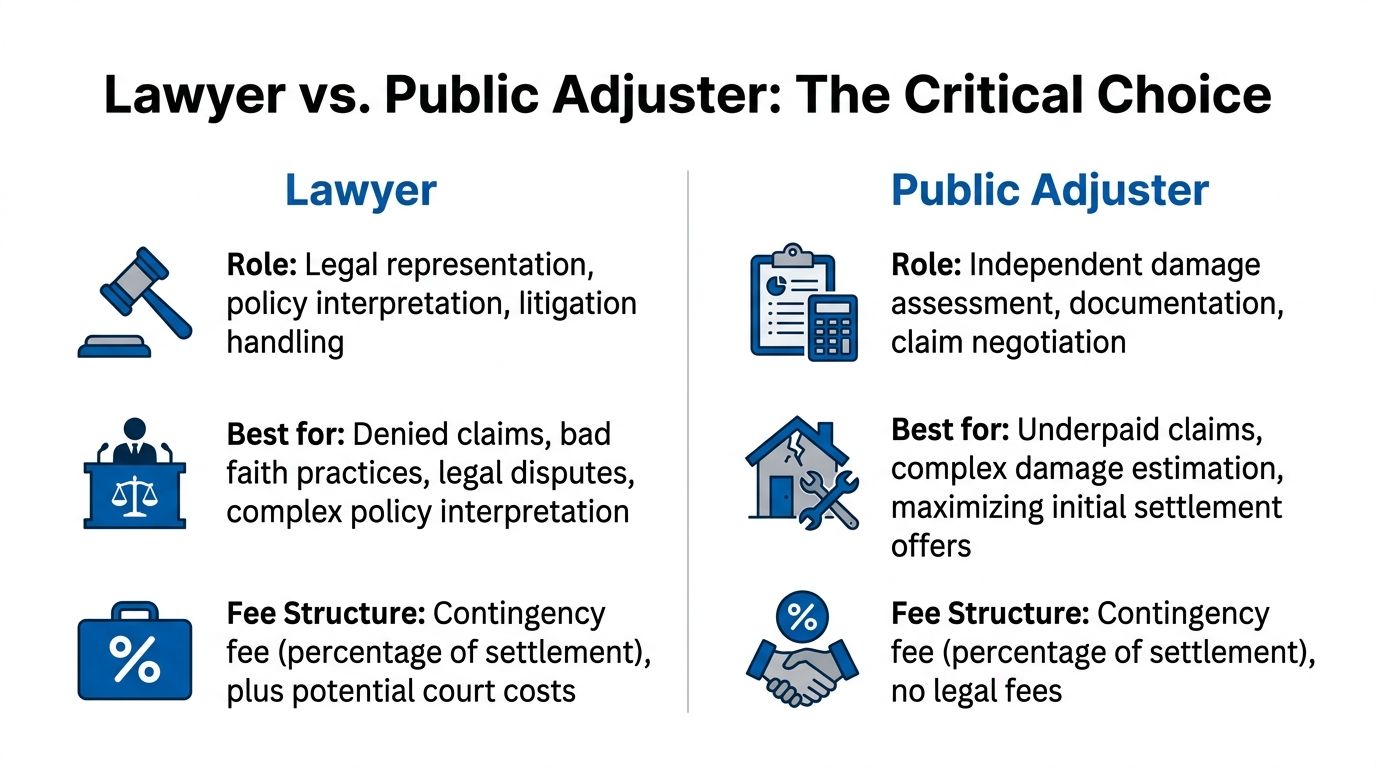

Lawyer vs Public Adjuster The Critical Choice

This is the decision most homeowners get wrong. They search for a home insurance claim lawyer because the claim feels unfair, but unfair doesn't automatically mean legal action should come first.

Most low-ball fights are proof disputes

A proof dispute is about valuation evidence. What was damaged? How far did the water travel? Does the flooring need full replacement? Was the smoke damage contained or widespread? What's the proper scope? What should the estimate include?

That kind of fight is usually better handled by a public adjuster, not a lawyer.

Guidance discussed by The Kirk Law Firm citing United Policyholders makes an important distinction between coverage disputes and proof disputes. Attorneys are recommended for legal battles over policy meaning. Valuation disputes are often resolved faster and cheaper by public adjusters, who focus on proving the full scope of loss without court intervention.

That matches what I've seen over and over. Many low-ball offers aren't the product of some brilliant legal argument. They come from bad measurements, missed rooms, ignored code items, omitted detach and reset work, incomplete moisture mapping, or depreciation applied too aggressively. A public adjuster lives in that terrain.

If you want a practical overview of that role, this explanation of what a public adjuster does lays it out well.

A public adjuster can document the loss, build the estimate, challenge the insurer's scope, and negotiate from actual damage evidence. That often fixes the problem without turning the claim into a lawsuit.

When the problem is legal coverage

A coverage dispute is different. The insurer may say the policy excludes the loss, that a condition wasn't satisfied, that a particular cause of loss isn't covered, or that the language limits payment in a way you dispute.

That's legal territory. Public adjusters can help organize the facts, but they don't replace a lawyer when the argument turns on policy interpretation or litigation strategy.

Here's the cleanest way to think about it.

| Issue | Better first call |

|---|---|

| The carrier admits damage but underprices it | Public adjuster |

| The estimate misses major line items | Public adjuster |

| The insurer says the loss isn't covered under the policy | Lawyer |

| The carrier may have acted in bad faith | Lawyer |

| You need damage scoping, documentation, and negotiation | Public adjuster |

Here's a useful discussion before you decide which lane fits your claim.

Quick comparison

- Lawyer: Best for legal interpretation, bad faith, and lawsuits.

- Public adjuster: Best for documenting, pricing, and negotiating the true value of property damage.

- Wrong hire, wrong cost: Using a lawyer on a pure valuation fight can add expense where better evidence might have solved the dispute sooner.

When You Absolutely Must Hire a Claim Lawyer

The storm hit months ago. Your house still is not repaired, the carrier keeps sending form letters, and every call ends with some new excuse. At that point, you are no longer dealing with a claim adjustment problem. You are dealing with a legal problem.

That distinction matters.

A public adjuster is usually the better first call when the fight is about scope, pricing, missed line items, or a sloppy carrier estimate. A lawyer becomes necessary when the insurer is hiding behind policy language, running out the clock, or acting in bad faith.

Bad faith changes the job

Bad faith is not just a frustrating claims experience. It is insurer conduct that may create a separate legal claim.

That is where a lawyer earns the fee. A lawyer can force production of the carrier's internal claim file through litigation, including notes, reserve history, evaluation logs, and communications that homeowners never see during ordinary negotiation. Those records often show the true story behind a denial or delay.

This overview of insurance bad faith and access to internal claim files explains why those documents matter. The denial letter is the public version. The claim file may show what the company knew internally and whether its position was ever reasonable.

Hire counsel in these situations

Get a claim lawyer involved when the dispute turns on policy interpretation. If the carrier is relying on exclusions, endorsements, conditions, causation language, late notice arguments, or technical definitions of loss, you need legal analysis, not another estimate.

Hire a lawyer when the claim is headed to suit. Public adjusters negotiate claims. They do not file lawsuits, conduct discovery, or argue motions in court.

Hire a lawyer when the carrier's behavior points to bad faith. Long unexplained delays, shifting denial reasons, selective reading of reports, or a refusal to respond after receiving solid documentation are all warning signs.

Deadlines also force action. Some states give homeowners a short window to sue, and missing it can wipe out an otherwise strong case. Florida shortened the time to bring certain property insurance contract actions in recent years. Arizona bad faith claims can also be subject to a two year limitations period, according to this discussion on Arizona law governing home insurance bad faith claims.

A missed legal deadline does more damage than a weak estimate ever will.

If you are close to a suit deadline, stop debating strategy and get legal advice immediately.

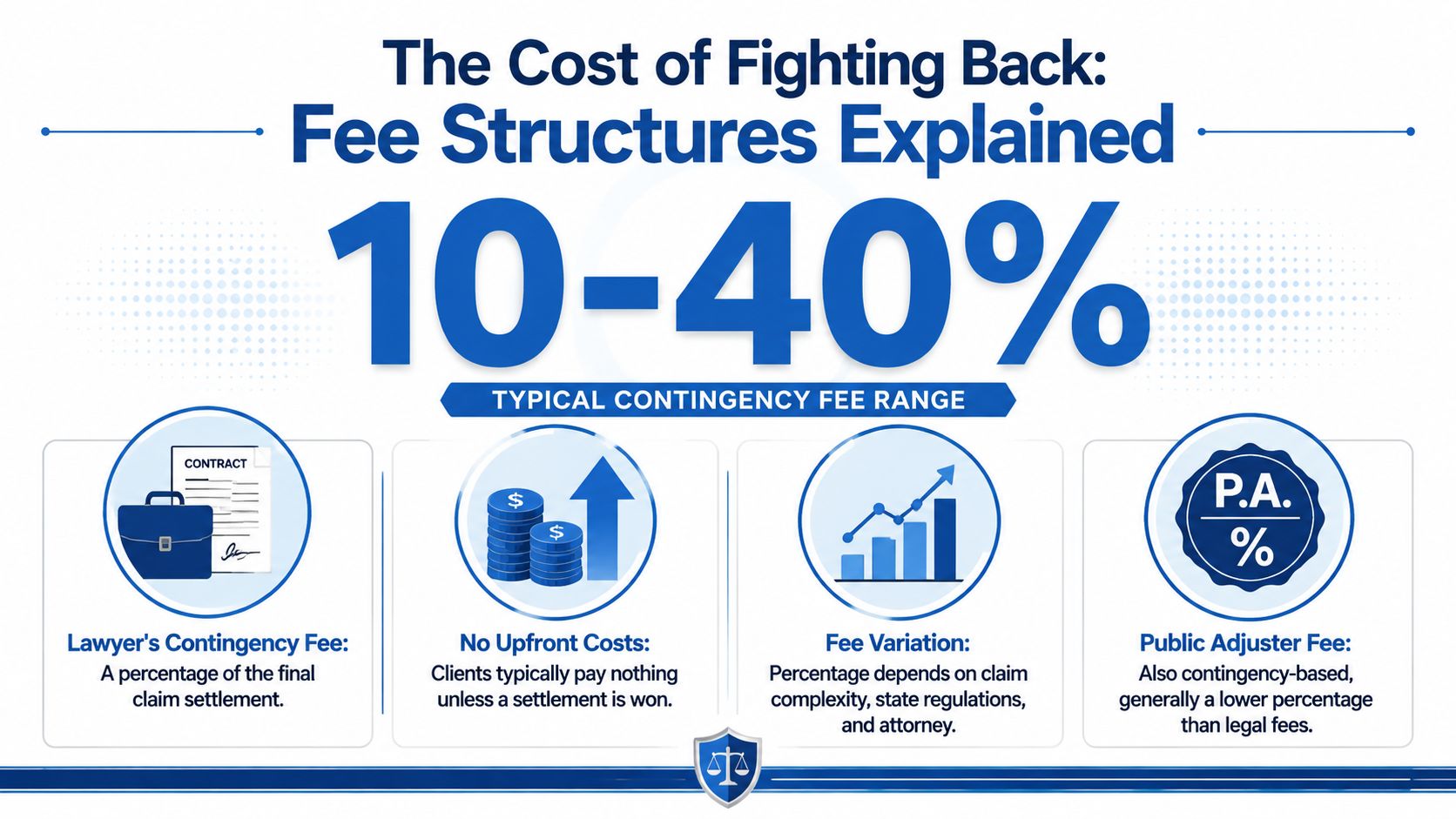

The Cost of Fighting Back Fee Structures Explained

Money matters. If you're considering a home insurance claim lawyer, you need to understand what that decision does to your net recovery.

What contingency fees really mean

Most home insurance claim lawyers work on a contingency fee, which means they get paid from the settlement rather than upfront. Typical fees run from 20% to 45% of the final settlement, according to Policygenius on whether you need a lawyer for a home insurance claim.

That's not a small haircut.

Policygenius also notes that for an average home insurance claim of about $15,100, a 33% fee takes nearly $5,000, leaving the homeowner with roughly $10,100. For a modest claim, that math matters. A lawyer can absolutely be worth it, but only when the legal advantage is likely to produce a significantly better outcome than you could get through claim preparation and negotiation.

Why cost should shape your strategy

This is why I tell homeowners to get the diagnosis right before hiring the most expensive weapon in the room.

If the insurer's mistake is a valuation problem, paying a large legal contingency may be unnecessary. A public adjuster can often attack the estimate itself, line by line, room by room, document by document. That preserves more of the payout for the person who has to rebuild.

Use this basic framework:

- High-value denied claim with legal issues: A lawyer may be worth every penny.

- Low-ball estimate with obvious scope gaps: A public adjuster is often the better first move.

- Potential bad faith case: Legal fees may be justified because the claim has moved beyond routine adjustment.

Don't ask only, “Can a lawyer help?” Ask, “Will the fee structure leave me with the recovery I actually need?”

That question keeps you from making an emotional hire when a strategic hire would serve you better.

Finding Vetted Claim Help in North Carolina and Virginia

If you own a home or business property in North Carolina or Virginia and the carrier is fighting your claim, don't start by chasing the loudest ad. Start by matching the professional to the actual dispute.

Who to call first

If the insurer accepted the claim but underpaid it, begin with a public adjuster. That's especially true for water, fire, smoke, wind, hail, hurricane, theft, and vandalism losses where the core issue is the scope and price of repairs.

If the dispute is about legal policy meaning, bad faith, or looming litigation, speak with a property insurance lawyer. If you're not sure which category fits, get the file reviewed by someone who works on policyholder-side property disputes every day.

For local help, homeowners and business owners looking for a public adjuster near them in North Carolina and Virginia should look for someone who handles residential and commercial property claims, understands carrier estimating platforms, and knows how to document a disputed loss from the ground up.

Questions to ask before you hire anyone

Don't be shy in the consultation. Ask direct questions.

- What kind of dispute do you think this is: Coverage or valuation?

- What property losses do you handle most often: Water, fire, smoke, storm, hail, hurricane, or commercial building damage?

- Who prepares the estimate and documentation: The person selling you the service, or someone else?

- How do you challenge low-ball estimates: Independent inspection, line-item scope review, policy analysis, expert input?

- If the claim turns legal, what happens next: Do you coordinate with counsel or stop at negotiation?

You should also pay attention to how they talk. If somebody can't explain your dispute in plain English, keep looking.

As for company reviews, the best ones usually sound the same in all the right ways. People mention responsiveness, clear communication, thorough inspections, strong documentation, and the feeling that somebody is finally on their side instead of the insurer's side. That's what you want. Not hype. Competence.

When your home is damaged and the carrier is dragging, low-balling, or denying, your first call should be the person most likely to identify the actual problem and preserve the most money in your pocket.

If you need straight answers on a denied, delayed, or underpaid property claim in North Carolina or Virginia, For The Public Adjusters, Inc. is a strong first call for homeowners and business owners who need real claim help, not insurance company talking points. Their team represents policyholders, not carriers, and helps assess damage, document losses, understand coverage, and push back when the insurer low-balls or mishandles a claim. Have your water damage claim questions answered at NO COST. Call 919-400-6440 to speak with a licensed Public Insurance Adjuster or Contact Us here with questions. WE Work For YOU… NOT Your Insurance Company!