After a fire, the person you hire to handle your claim is called a public adjuster, and they are your single most important ally. They are a state-licensed insurance professional who works only for you, the policyholder. They take over the entire nightmare of a claims process, from digging through the rubble to document every single loss to fighting your insurance company for the final settlement check. Their job is to make sure you get every penny you are owed.

Your Expert Advocate Against a Deceptive Insurance Company

The moment your insurance company learns about the fire, they will send their own adjuster out to the scene. You need to understand one thing from the very beginning: that person does not work for you. The insurance company adjuster works for the insurance company, and their primary goal is to protect their employer’s bottom line by paying you as little as legally possible.

Letting the insurance company's adjuster handle your claim is like walking into a courtroom and letting the other side's lawyer represent you. It's a fundamental conflict of interest. These adjusters, whether from State Farm, Allstate, or another carrier, are notorious for using company-mandated software designed to undervalue everything. They’ll apply harsh depreciation to your personal belongings and completely miss hidden damage from smoke, soot, and the water used to put out the fire, all in a calculated effort to reduce their payout.

This is exactly why hiring your own public fire claim adjuster is so critical. They exist to level the playing field. They are your professional advocate, bound by law and a code of ethics to fight for your best interests and yours alone.

The Role of Your Personal Adjuster in the Dispute

A public adjuster steps in and takes control of the confusing, exhausting, and emotionally draining claims process. This frees you up to focus on what matters most—piecing your life, family, or business back together.

Here’s what they do for you:

- A Deep-Dive Damage Assessment: The insurance company’s guy might do a quick walkthrough. Your public adjuster performs a forensic-level investigation. They document everything from the charred structural beams down to the invisible smoke particles that have contaminated your HVAC system and the inside of your walls.

- Meticulous Inventory and Valuation: Creating a list of every single item you lost is a heartbreaking task. Your adjuster manages this for you, but more importantly, they know how to properly value each item based on the specific language in your policy. They know how to fight back when the insurer tries to unfairly devalue your property.

- Decoding Your Insurance Policy: Insurance policies are dense legal contracts written to be confusing. Your adjuster is fluent in "insurance-speak." They find and apply every bit of coverage you're entitled to—for the structure, your personal property, and the costs of living elsewhere—to maximize your financial recovery. For a more detailed breakdown of their job, you can learn more about what a public adjuster is in our full guide.

- Negotiating From a Position of Strength: Your adjuster becomes the single point of contact with your insurance company. They build an ironclad claim backed by indisputable proof of your loss. They don’t just accept the first lowball offer; they negotiate aggressively to secure the full and fair settlement you deserve.

Unmasking the Insurance Company's Playbook

After a fire rips through your life, you count on your insurance company to be the safety net you've been paying for. But here's the hard truth: major carriers often see your claim not as a promise to keep, but as a cost to be managed. They have a well-worn playbook of delay, deny, and defend tactics designed to frustrate you into accepting less than you're owed.

Knowing these moves is your first line of defense. They are betting you're too exhausted, stressed, and unfamiliar with the process to fight back. A public fire claim adjuster, on the other hand, has seen this game played out hundreds of times and knows exactly how to break it down, piece by piece.

The Lowball Offer: A Calculated Strategy

Insurance companies have entire systems built to methodically undervalue your losses. These aren't just honest mistakes; they are deliberate strategies that protect their profits at your expense.

Some of their go-to moves include:

- Using Outdated Pricing: They'll often use pricing software for repairs that ignores the reality of today's local labor and material costs. The result is an estimate that can be thousands of dollars short of what a real contractor will actually charge.

- Aggressive Depreciation: When it comes to your personal belongings, they'll apply steep and often unfair depreciation, arguing that your property was worth a fraction of its true replacement value right before the fire.

- Ignoring Hidden Damage: The company adjuster frequently glosses over the long-term, corrosive damage from smoke and soot. This contamination gets into your HVAC system, insulation, and behind walls, leading to lingering health hazards and odors they conveniently leave out of their estimate.

An insurer's first offer isn't a fair assessment of your loss. It's a starting number in a negotiation, and it's always tilted in their favor.

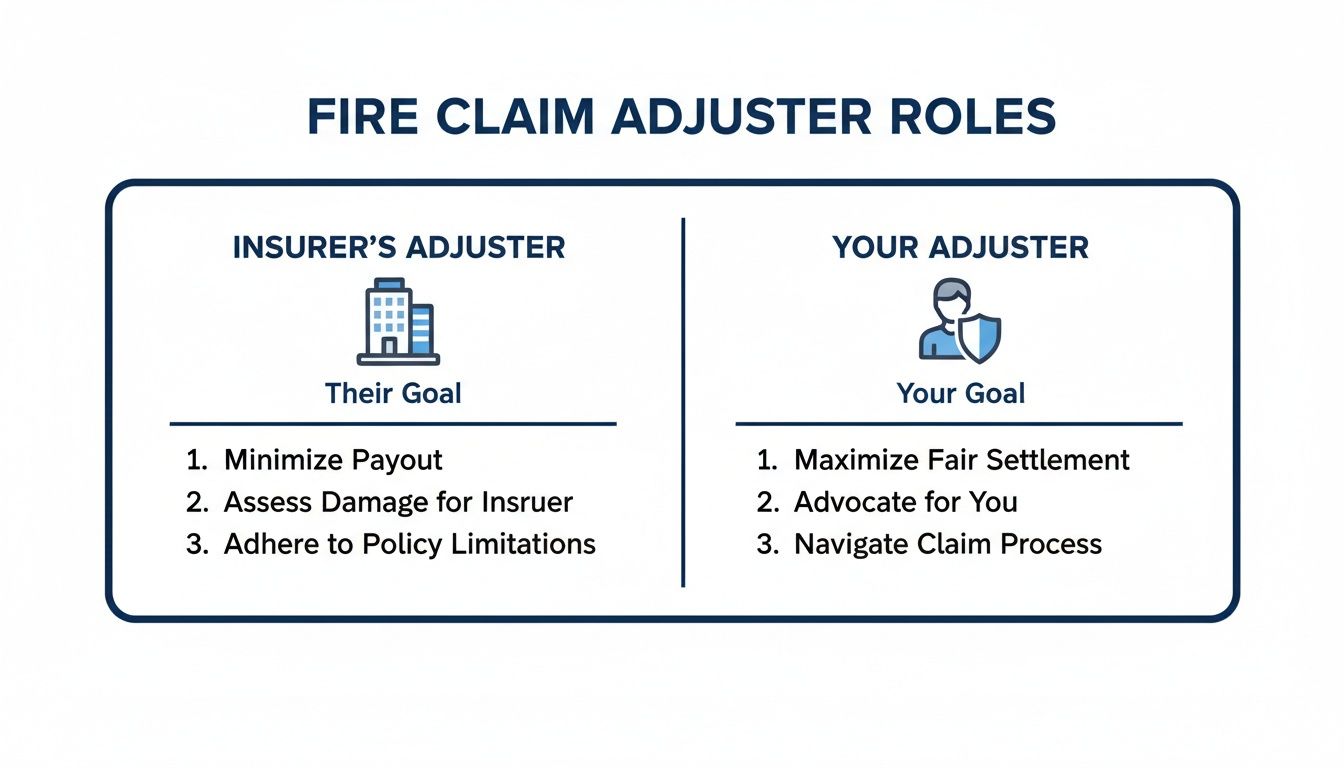

This is where the fundamental conflict of interest comes into play. The adjuster your insurance company sends works for them, not you. The one you hire works only for you.

As you can see, their goals are directly opposed. The insurance company adjuster is there to limit the payout. Your public adjuster is there to maximize it.

To spell it out even more clearly, here’s how their approaches differ on the key parts of your claim:

Insurer's Adjuster vs Your Public Adjuster

| Claim Component | Insurance Company's Approach | Your Public Adjuster's Approach |

|---|---|---|

| Damage Assessment | Focus on visible damage, often overlooking hidden issues like smoke, soot, and structural weakness. | Conducts a forensic, detailed inspection of all damage, including hidden and long-term effects. |

| Repair Estimates | Uses standardized pricing software that may not reflect current local market rates for labor and materials. | Gathers multiple, real-world bids from vetted local contractors to establish the true cost of rebuilding. |

| Personal Property | Applies aggressive depreciation and may group items into broad, low-value categories. | Creates a detailed, itemized inventory, finding evidence for the highest possible replacement cost value for each item. |

| Communication | Can be slow to respond, create delays, and control the flow of information to their advantage. | Manages all communication, forcing the insurer to adhere to policy deadlines and act in good faith. |

| Final Goal | Minimize the claim payout to protect the insurance company's bottom line. | Maximize the settlement to ensure you have the funds for a complete and proper recovery. |

The differences are night and day. One path leads to a quick, low settlement; the other leads to a fair and full recovery.

The Strategy of Intentional Delays

Beyond the lowball offer, the insurance company's most powerful weapon is time. They know you're displaced, under immense stress, and burning through your savings. By dragging their feet, they dial up the pressure, hoping you'll give in and take a fast, cheap payout just to get it over with.

They'll "lose" your paperwork. They'll ask for the same documents over and over. They'll go silent for weeks at a time. In more serious cases, they may demand an Examination Under Oath—a formal, intimidating interrogation run by their attorneys to catch you in a contradiction. Understanding the gravity of an Examination Under Oath is critical, as insurers use it as a tool to find a reason to deny your claim entirely.

A public adjuster immediately short-circuits these delay tactics. They manage all the communication, submit a perfectly documented claim from the start, and hold the insurer accountable to every deadline in your policy. They build a case so strong and so complete that the insurance company runs out of excuses to delay and has no choice but to pay what you are truly owed.

Why an Independent Adjuster Is More Critical Than Ever

In the chaotic aftermath of a fire, the ground has shifted under the feet of homeowners and business owners. Insurance policies are getting thicker and more confusing by the year, and with catastrophic events on the rise, insurance carriers are stretched dangerously thin.

This pressure cooker environment means their adjusters are overworked, rushed, and far more likely to make critical mistakes—errors that can easily cost you tens of thousands of dollars. When your insurance company sends its adjuster, you aren't just meeting a person. You're up against a massive corporate machine built to do one thing: control costs and minimize what they pay you.

This is exactly why having your own independent advocate—a public fire claim adjuster—has never been more important.

A Growing Industry with Conflicting Agendas

Let's be clear: the insurance claims industry is big business, and carriers have a powerful financial reason to pay out as little as possible. This isn't just a hunch; the numbers tell the story.

The global claims adjusting sector recently ballooned into an estimated $14.6 billion industry, posting 9.6% annual growth. This surge is fueled by more policies and, critically, more catastrophic events. You can see more details about the claims adjusting industry's growth on kentleyinsights.com.

This multi-billion dollar machine is not designed to be on your side. Every dollar they pay you is a loss on their spreadsheet. Their adjusters are trained inside this system, using company-mandated software and internal guidelines that almost always lead to underpayments.

Having an independent expert is the only way to cut through this built-in bias. A public adjuster works for you and only you, fighting for a settlement based on what was actually destroyed, not what the insurer’s software says it should cost. It's a critical difference, which you can learn more about by understanding the roles of an insurance adjuster vs public adjuster.

Your Shield Against Rushed and Flawed Inspections

After a major disaster like a wildfire or hurricane, insurance companies get hit with thousands of claims all at once. They deploy "catastrophe adjusters" from all over the country who are under enormous pressure to get through a high volume of claims as fast as humanly possible.

This rush creates a predictable pattern of costly mistakes:

- Superficial Inspections: They might spend less than an hour at your property, completely missing hidden smoke, soot, and water damage that will surface months down the road.

- One-Size-Fits-All Estimates: They lean on generic, pre-filled estimate templates that fail to capture the unique details of your home or the true cost of local labor and materials.

- Lack of Specialized Knowledge: Many of these adjusters aren't experts in the complex science of fire and smoke restoration, causing them to misdiagnose or totally ignore severe structural and cosmetic damage.

Your public adjuster is your shield against this. They act as your quality control expert and chief negotiator, conducting a forensic-level investigation of your loss. They document every single detail and build a claim so thorough and undeniable that your insurance company has no choice but to pay what is fair and what you are rightfully owed.

How Public Adjusters Secure Massive Settlement Increases

The real proof of a public fire claim adjuster's worth isn't in theory; it's in the cold, hard cash they put back in their clients' pockets. The gap between an insurer’s first lowball offer and the final check can literally be the difference between ruin and recovery for a family or business. These real-world outcomes pull back the curtain on just how hard insurance companies work to underpay what you’re rightfully owed.

Let's look at a real story. A family’s home was gutted by a kitchen fire. Their insurance company, one of the big names you see on TV, was quick to send their guy out. They were even quicker to cut a check for a measly $85,000. The company adjuster insisted most of the smoke damage was just "superficial" and could be covered up with a special coat of paint.

Feeling trapped and completely overwhelmed, the homeowners decided to hire their own advocate—a public adjuster. Their expert saw the insurer's game immediately and brought in independent environmental hygienists to test the air and surfaces throughout the entire house.

Finding the Damage They "Missed"

The results from the independent testing were exactly what the public adjuster suspected. Toxic soot and ash had worked their way deep into the drywall, the insulation, and even the HVAC system. It was a serious, long-term health hazard that the insurance company had conveniently chosen to ignore.

Armed with hard science, the public adjuster tore up the old claim and built a new one from scratch. He documented every last detail of the real damage and went to war with the carrier. The result? The insurance company was backed into a corner and forced to pay a final settlement of $240,000. That’s nearly three times their insulting first offer.

This wasn't a miracle. It was the direct result of having a true expert in their corner who refused to let the insurance company get away with cutting corners and endangering a family's health.

A public adjuster’s job is to find and prove the full, often hidden, scope of your loss. They force the insurance company to honor the actual policy you’ve been paying for, not the cheap version they'd prefer to pay out.

Saving a Business from a Wrongful Denial

The stakes get even higher when a business is on the line. Take the case of a local restaurant, a community favorite, that was ravaged by an electrical fire. The owner filed a business interruption claim to cover the massive income loss while they were forced to shut their doors. But their insurer flat-out denied the claim, pointing to some obscure clause they claimed got them off the hook.

The business was days away from having to close for good. The owner brought in a public adjuster who specialized in complex commercial policies. The adjuster immediately launched a forensic audit of the restaurant's books and dismantled the policy language the insurer was trying to hide behind.

He built an ironclad case proving the denial was entirely baseless and showed exactly how much revenue was lost. Faced with the very real threat of a bad faith lawsuit, the insurance company folded. They reversed their decision and paid the claim in full, saving the restaurant and the jobs of everyone who worked there.

The Nightmare Scenario: Fighting Your Wildfire Claim Alone

Wildfires aren't just bigger fires; they're a completely different kind of disaster. And when one sweeps through, it creates chaos that insurance companies are all too willing to use against you.

Think about it. A single wildfire triggers thousands of claims all at once, burying carriers like State Farm and Allstate. Their solution? Fly in "catastrophe adjusters" who have one job: clear claims off their desk as fast as possible. This means quick, surface-level inspections and sweeping, inaccurate estimates that leave families like yours holding the bag for massive repair costs.

Once the brave firefighters have done their job, your fight for financial survival is just beginning. It's a battle that demands an expert in your corner.

The Invisible Damage Your Insurer Will Ignore

The real damage from a wildfire isn't just what you can see. It's not just the charred walls or the melted belongings. The intense heat and toxic fallout create a host of expensive, complex problems that the insurance company's adjuster is neither trained nor motivated to find.

A public fire claim adjuster who specializes in these events knows exactly what to look for:

- Toxic Ash and Soot: This isn't just a mess you can wipe up. It’s a corrosive, hazardous cocktail that gets everywhere—your HVAC system, inside your walls, and deep into the soil. It requires specialized, professional remediation, an expense insurers love to deny.

- Soil Instability: The sheer heat of a wildfire can literally cook the ground your home sits on. This changes the soil's composition, creating a serious, long-term structural risk to your foundation that a rushed adjuster will absolutely miss.

- Compromised Concrete: Your foundation might look fine from a distance, but that searing heat can create thousands of microscopic cracks. This weakens the concrete, threatening the integrity of your entire home.

The company adjuster's goal is to close your claim using the cheapest, fastest path possible. They will ignore or outright dismiss these critical issues. A public adjuster’s only job is to document the total scope of your loss, bringing in engineers and environmental experts to build an ironclad case for what it truly costs to make you whole again.

How They Justify Systemic Lowball Offers

When a disaster causes massive losses for an insurance company, they go into self-preservation mode. They start systematically lowballing every single claim to stanch the financial bleeding. This isn't personal; it's just business. And that's precisely why having your own advocate isn't a luxury—it's a necessity.

Wildfire activity puts an unbelievable strain on insurance adjusters. A recent analysis found over 26,500 wildfires in the U.S. in just five months, impacting tens of thousands of properties. This creates a massive bottleneck, forcing rushed, inaccurate claim assessments.

That kind of pressure guarantees your claim won't get the careful attention it needs from the insurance company.

A public fire claim adjuster takes that entire burden off your shoulders. They meticulously build an evidence-based claim that punches holes in the insurer's lowball tactics and forces them to honor the policy you paid for.

Answering Your Questions About Hiring a Fire Claim Adjuster

Trying to make sense of your options after a fire is overwhelming. When you're thinking about bringing in an expert to fight for you, it’s only natural to have some questions.

Getting straight answers will give you the confidence you need to make the right call and secure the settlement you are owed. Let's clear up the most common concerns.

How Does a Public Adjuster Get Paid?

This is the most critical question people have, and the answer is simple. A public fire claim adjuster works on a contingency fee basis, which means you pay absolutely nothing out of your pocket, ever.

There are no upfront costs, no retainers, and no hourly bills piling up while you're trying to put your life back together.

Their fee is just a small, pre-agreed percentage of the final insurance settlement they win for you. This setup is powerful because it puts them on your side of the table—they only get paid when you get paid. The more money they recover for you, the more they earn.

In nearly every single case, the massive settlement increase an adjuster negotiates is far more than enough to cover their fee, leaving you with a much larger net payout than you could have ever hoped to get on your own.

Is It Too Late to Hire Help?

No, it's almost never too late to bring in a professional advocate. Many homeowners and businesses only realize they need help after their insurance company makes a shockingly low offer or starts using delay tactics to grind them down.

A public adjuster can step in and take over your claim at any point before you sign that final settlement agreement. They can immediately get to work to:

- Re-open negotiations armed with new evidence and documentation.

- File a supplemental claim for all the damages the insurance company’s adjuster conveniently “missed.”

- Force the insurer to answer for their mistakes and omissions.

While it's always best to get an adjuster involved from day one—before the insurance company can control the narrative—hiring an expert is a game-changing move at any stage of a frustrating claim.

Will My Insurance Company Punish Me for Hiring an Adjuster?

This is a common fear, but the answer is a hard no. It is completely illegal for your insurance company to retaliate against you for hiring a licensed professional to represent your own financial and legal interests.

They can't cancel your policy, jack up your rates, or treat your claim any differently just because you brought in help. In fact, your right to representation is legally protected.

Hiring a public fire claim adjuster doesn't create a fight; it levels the playing field. It sends a clear message to your insurer that you're serious about getting the full and fair settlement you're entitled to under the policy you paid for.

It tells them you won't be intimidated, lowballed, or worn down until you give up.

When your insurance company is delaying, denying, or underpaying your claim, you don't have to fight them alone. At For The Public Adjusters, Inc., we are your licensed advocates, fighting to get you the maximum settlement you are owed. If you’re struggling with a property damage claim in North Carolina or Virginia, contact us for a free, no-obligation claim review at https://forthepublicadjusters.com.