The fire is out, but the fight usually starts after the trucks leave.

If you're searching for a fire claim adjuster apex nc, you're probably already dealing with the part nobody warns you about. Smoke in the closets. Soot inside the HVAC. A carrier adjuster who sounds helpful on the phone, then sends an estimate that doesn't come close to what it will take to repair your home or reopen your business. That gap is where most disputes begin.

In Apex, homeowners and business owners don't usually need help "filing" a fire claim. They need help when the insurance company slows the process down, cuts out major parts of the damage, or acts like a first offer is the final word. It isn't.

Table of Contents

- The Inherent Conflict with Your Insurer's Adjuster

- Common Tactics Insurers Use to Deny and Low-Ball Fire Claims

- Know Your Rights Under North Carolina's Claim Laws

- The Local Apex Advantage with For The Public Adjusters

- Answering Your Toughest Fire Claim Dispute Questions

- Take Control of Your Fire Claim Recovery Today

The Inherent Conflict with Your Insurer's Adjuster

The insurance company adjuster who shows up after a fire is not your advocate. That's the first issue many property owners in Apex misunderstand, and it's the reason so many claims go off track early.

The carrier's adjuster works for the carrier. Their job is to inspect, evaluate, and resolve the claim in a way that protects the insurer's financial position. They may be polite. They may sound reassuring. None of that changes who they represent.

A public adjuster represents the policyholder only. That difference isn't a technicality. It's the center of the entire dispute.

Why this turns into a fight so quickly

After a fire, the scope of loss is rarely limited to what you can see standing in the living room. A company adjuster may focus on burned framing, obvious surface damage, and a short list of contents. But serious fire losses often include hidden smoke migration, residue inside mechanical systems, water damage from suppression, debris handling, code issues, temporary housing, and itemized contents loss.

When the insurer's side controls the inspection, the estimate, and the framing of the damage, they also control the starting number. That's why the first offer is so often low.

Practical rule: If the person evaluating your fire damage is paid by the company writing the check, you should assume their interests and yours are not aligned.

That doesn't automatically mean every adjuster is acting in bad faith. It does mean you should stop assuming they are there to maximize your recovery.

What works and what doesn't

What works is independent documentation, policy review, and direct challenge when the carrier leaves out line items or undervalues the loss.

What doesn't work is trusting verbal assurances such as "we'll take care of it" or "this is standard." Those phrases don't repair a house. They don't restore contents. They don't force payment for overlooked smoke damage.

If you want a clear breakdown of the difference in roles, this guide on insurance adjuster vs public adjuster lays out the conflict plainly.

A serious fire claim is an adversarial process whether the insurer admits it or not. Once you understand that, you stop waiting for fairness and start building a strong position.

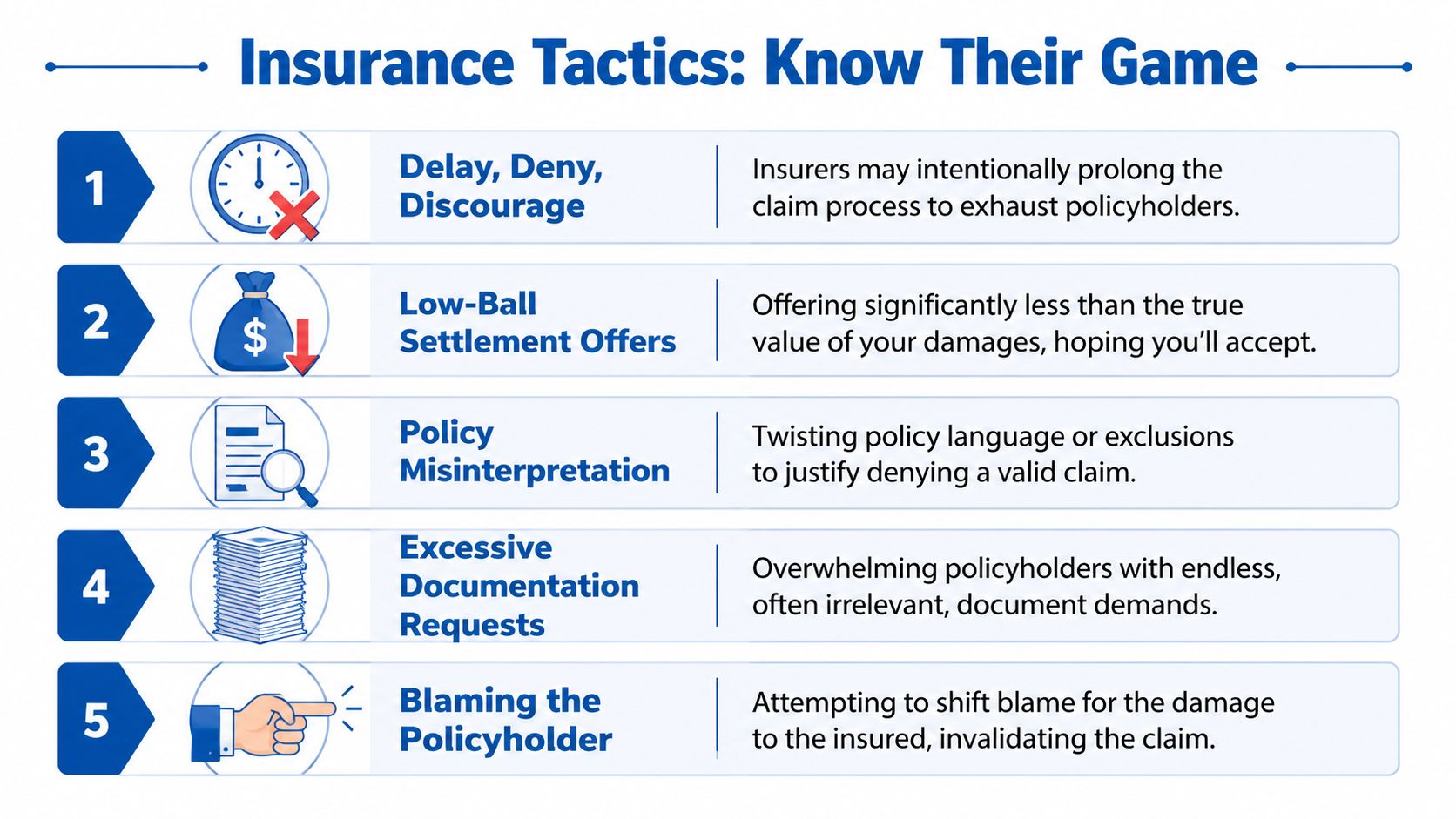

Common Tactics Insurers Use to Deny and Low-Ball Fire Claims

State Farm, Allstate, and other major carriers don't protect their profits by paying the full value of every fire claim without resistance. They protect profits by narrowing the loss, questioning the scope, and exhausting policyholders who just want to get home again.

That's the pattern behind most fire claim disputes in Apex.

They minimize smoke and soot because it's harder to see

Carriers often write for what photographs well. Burned cabinets. Blackened drywall. Char at the point of origin.

What they resist is the wider contamination pattern. Smoke doesn't stay politely in one room. It moves through returns, wall cavities, attic areas, textiles, and porous materials. When that spread isn't documented with the right tools, insurers treat it like minor cleaning instead of full restoration or replacement.

Public adjusters counter those low estimates with advanced documentation such as Matterport 3D scans and thermal imaging, which can prove hidden smoke infiltration and structural issues and can accelerate settlements by up to 50% when compared with incomplete visual inspections, according to Apex Public Adjusting's description of its documentation approach.

They leave out code-required work

A fire-damaged home isn't repaired in a vacuum. Rebuild work has to meet current code. That's where many insurers shave the claim.

They may price for basic replacement but leave out upgrades that become mandatory once damaged materials are removed and the rebuild starts. That gap hits hard on older homes and mixed-use buildings. The owner thinks the estimate covers the repair. Then the contractor starts opening walls and the true cost appears.

Commonly overlooked areas include:

- Electrical updates that become necessary during reconstruction

- Fire-rated assemblies required in repaired sections

- Alarm or detection components triggered by current code standards

- Ordinance and Law coverage that exists in the policy but wasn't applied properly

Smoke damage disputes are rarely just about cleaning. They're often about whether the carrier priced a cosmetic fix for a loss that actually requires code-compliant restoration.

They steer you toward controlled repair pricing

Another tactic is "helpful" contractor referral. The insurer recommends a preferred vendor, and the offer is framed like a convenience to you.

Sometimes that contractor does acceptable work. Sometimes the estimate is built to fit the carrier's number instead of the actual damage. That's the trade-off. The repair scope can become a budget exercise rather than a restoration plan.

A homeowner should be suspicious when the repair path arrives prepackaged before the full damage is even mapped.

They bury you in delay tactics and paperwork

Not every denial comes in the form of a denial letter. Some arrive as a stream of repeated document requests, partial responses, rotating desk adjusters, and long stretches of silence.

Those tactics pressure people into accepting less just to move on. A family displaced after a fire is vulnerable to that pressure. A business owner watching downtime expand is even more vulnerable.

Watch for these signs:

| Tactic | What it looks like in real life |

|---|---|

| Scope narrowing | The estimate covers visible fire damage but omits hidden smoke, water, or content losses |

| Exclusion pressure | The carrier points to isolated policy language while ignoring broader covered damage |

| Vendor steering | You're pushed toward insurer-connected contractors before the dispute is fully evaluated |

| Delay by repetition | The same information is requested more than once, or review restarts with a new adjuster |

If you're in a dispute, the answer is not louder frustration. It's better evidence, tighter documentation, and direct challenge to each unsupported cut.

Know Your Rights Under North Carolina's Claim Laws

A lot of homeowners think the insurer can move at whatever pace it wants after a fire. That's wrong.

North Carolina gives you a framework for holding the carrier accountable. Under N.C. Gen. Stat. § 58-63-15, insurers must acknowledge your fire claim within 15 days and make a payment decision within 30 days after receiving complete documentation, as noted in this North Carolina claim timeline summary.

The deadlines matter

Those deadlines don't mean every claim gets paid in full within a month. They do mean the carrier can't lawfully drift forever while your house sits damaged and your family absorbs the cost.

This matters in fire disputes because the insurer often benefits from delay. The longer you wait, the more likely you are to accept a partial payment, a smaller scope, or a bad contractor just to get movement.

North Carolina's law also prohibits conduct such as misrepresenting policy benefits or failing to affirm or deny coverage promptly. That gives you an advantage if the company keeps stalling while pretending the file is still under routine review.

A practical approach is simple:

- Track the claim notice date so there's no confusion about when the clock started.

- Confirm when the insurer says your documentation is complete.

- Keep every email and letter tied to requests, submissions, and responses.

- Log every phone call with the date, time, and the name of the adjuster or examiner.

- Challenge missed deadlines in writing rather than only by phone.

What you should document during a dispute

Fire claims become vulnerable when the paper trail is weak. If the insurer says it never received a report, didn't have enough support, or was still waiting on an item, you need records that cut that excuse off.

Use a basic dispute file that includes:

- Carrier communications including emails, letters, and claim portal messages

- Inspection records with dates, names, and what areas were inspected

- Photos and scans showing the full spread of smoke, soot, water, and structural damage

- Policy excerpts for dwelling, contents, loss of use, and code-related provisions

- Receipts and housing costs if you're displaced after the fire

The insurer's timeline gets much less flexible when your documentation is organized and their delays are visible.

If the carrier keeps dodging, legal escalation may become necessary. Homeowners dealing with that stage often benefit from understanding how North Carolina homeowners insurance claim lawyers fit into a broader dispute strategy.

A claim dispute is easier to win when you stop treating delays like inconvenience and start treating them like evidence.

The Local Apex Advantage with For The Public Adjusters

The fire is out. The trucks are gone. Then the carrier starts treating your Apex loss like a standard estimate file, even when the damage pattern says otherwise.

That is where local claim work matters.

Apex homes often present a mix of direct flame damage, heavy smoke spread, suppression water, HVAC contamination, and code-triggered repair issues. A generic desk review can miss that. A local public adjuster who knows how these losses develop in Wake County can challenge a shallow scope before it hardens into the carrier's final position.

Why local fire response data matters in a claim dispute

Apex gives you one fact that can matter in the story of your claim. In January 2021, the Apex Fire Department achieved an ISO Public Protection Classification of Class 1, placing it in the top 1% of fire departments nationwide, according to the Town of Apex announcement on the ISO Class 1 rating.

That does not prove value by itself. It does help frame the loss correctly.

I use facts like this when a carrier tries to flatten the timeline, minimize smoke migration, or suggest the condition of the property got worse because the response or suppression effort was somehow lacking. In Apex, that argument can fall apart fast. The local fire response standard is high, and that matters when the insurer starts building a theory that does not match the scene.

Homeowners who want a public adjuster near Apex for fire and property damage claims usually need more than estimate writing. They need someone who can tie local facts, damage documentation, and policy language together in a way the carrier cannot brush aside.

A real client experience

The review shown above makes the point clearly. The client describes For The Public Adjusters as professional, knowledgeable, and responsive, and credits the team with helping during a difficult claim process while keeping communication clear throughout. That kind of feedback matters in a fire dispute because confusion helps the insurer, not the policyholder.

A fire claim is a control fight. Who defines the scope of cleaning. Who decides whether insulation stays or comes out. Who challenges a contents number that ignores real replacement cost. Who pushes back when smoke damage is priced like light housekeeping instead of structural deodorization and restoration.

For The Public Adjusters works in that factual lane. The job is to document the loss thoroughly, read the policy closely, and force support for every carrier position that cuts value or delays payment.

Local knowledge helps when the insurer is counting on you not knowing what to question. In Apex, that can mean using the facts of the fire response, the condition of the property, and the full smoke and water spread to build a claim that is harder to underpay.

Answering Your Toughest Fire Claim Dispute Questions

The hard questions usually show up after the first estimate, after the delay letter, or after the denial. That's when people realize they aren't dealing with a simple repair claim. They're in a dispute.

What is the appraisal clause and when should you use it

The appraisal clause is a policy mechanism used when the primary fight is over value, not basic coverage. If both sides agree there is covered fire damage but sharply disagree on what the repairs, contents, or restoration should cost, appraisal may help break the stalemate.

It's usually worth considering when:

- Coverage is not the main issue and the dispute is about price or scope valuation

- You already have strong documentation from contractors, inventories, and inspections

- Negotiations have stalled and the carrier keeps recycling the same low number

It is usually not the first move if the insurer is denying large sections of the claim outright based on exclusions or causation arguments. In that situation, you first need to attack the denial basis itself.

What if the insurer says you failed to prevent further damage

That accusation is common after fires because suppression water, open roof areas, broken windows, and HVAC contamination can all worsen conditions after the initial event.

Your response should be evidence-based:

- Show what emergency steps were taken such as board-up, tarping, water extraction, or power shutoff

- Keep receipts and work orders from mitigation vendors

- Tie the timing together so the insurer can't rewrite the sequence after the fact

A carrier often raises this issue to shift part of the loss back onto you. That doesn't mean the accusation is valid.

If the insurer blames you for post-fire conditions, force the discussion onto dates, invoices, site notes, and photographs. General accusations collapse when the timeline is documented.

What if the claim is denied outright

A denial is serious, but it is not always final.

Start by demanding the exact policy basis for the denial in writing. Then compare that language to the actual damage evidence. One major area of dispute is smoke migration. Some insurers try to narrow or exclude it aggressively, but public adjusters challenge those positions with evidence such as independent thermal imaging for smoke residue validation, as described by For The Public Adjusters in discussing smoke migration disputes.

Later in the dispute, video explanations can also help clarify how these battles unfold in practice:

A denial should trigger a structured response:

- Get the denial letter and policy citations

- Build a rebuttal package with expert documentation and corrected scope

- Challenge unsupported exclusions or causation arguments

- Escalate if needed through appraisal, formal complaint channels, or legal counsel

The insurer wants a denial to feel final. It often isn't.

Take Control of Your Fire Claim Recovery Today

After a fire, the insurance company wants to control the pace, the scope, and the number. You don't have to accept that.

A disputed fire claim is winnable when the damage is documented correctly, the policy is read aggressively, and the carrier's omissions are challenged one by one. That includes the coverages insurers often underpay or skip. According to Apex Adjusting Group's discussion of fire claim recovery, public adjusters often recover 3 to 5 times the insurer's initial offer by identifying coverages such as Ordinance & Law and Loss of Use that company adjusters frequently underpay or ignore.

That doesn't mean every claim turns into a courtroom brawl. It means you should stop treating the first insurer position like a neutral one.

If you're rebuilding after a fire, prevention matters too. Homeowners looking to reduce future risk can review these Purified Air Duct Cleaning fire prevention insights, especially around common household fire causes and maintenance issues that often get overlooked.

Don't let your insurer dictate your recovery.

If your home or business fire claim in Apex is delayed, underpaid, or denied, get a no-cost review from For The Public Adjusters, Inc..