When you and your insurance company are at odds over your homeowner or business property damage claim, you’re in what’s called an insurance claim dispute. This usually means you’ve been hit with a flat-out denial, a frustrating delay, or—most commonly—a lowball settlement offer from a carrier like State Farm or Allstate that won’t come close to covering your repairs.

Getting through this isn’t about just getting angry. It's about understanding the game your insurer is playing, documenting everything, and knowing exactly when and how to fight back for the money you're rightfully owed.

Why Insurers Like State Farm and Allstate Deny Or Underpay Claims

It’s a story we’ve heard countless times from homeowners and business owners. You’ve paid your premiums like clockwork for years. But after a disaster strikes your property, the very company you trusted to make you whole seems determined to pay as little as possible.

This isn’t just a string of bad luck. It's often a calculated business strategy designed to protect their profits at your expense.

The major insurance carriers are publicly traded corporations. Their first legal duty isn't to you—it's to their shareholders. It's a simple, brutal equation: their profits go up when your claim payout goes down. This creates an immediate conflict of interest the moment you file a claim for damage to your home or business.

Their entire claims department is built around minimizing financial exposure. The adjuster they send out from State Farm or Allstate isn't a neutral third party; they work for the insurer. Their job is to find reasons to shrink your payout, whether that means digging up an obscure policy exclusion, slapping aggressive depreciation on your property, or just plain ignoring damage they decide isn't essential.

The Profit Motive Behind Every Denial

Insurance companies run on a basic model: take in more money in premiums than they pay out in claims. When a hurricane, wildfire, or other large-scale catastrophe happens, the pressure to control costs becomes immense. That pressure lands squarely on how your homeowner or business owner claim gets handled.

They know you’re exhausted, stressed, and probably haven’t read your insurance policy from cover to cover. Insurers are betting you'll just accept their first lowball offer without putting up a fight. It’s a strategy that saves them thousands, even tens of thousands, of dollars per claim—money that should have gone to rebuilding your life.

Let's get one thing straight: your insurance company is not your partner in recovery. The moment you file a claim, the relationship becomes adversarial. They have a team of experts protecting their financial interests. You need a strategy to protect yours.

Rising Storms And Increasing Disputes

This isn't just a feeling you have; the data proves it. The number of insurance claim disputes is skyrocketing, fueled by more frequent and more destructive weather events. As catastrophic losses pile up, insurers batten down the hatches, making it tougher than ever for honest policyholders to get a fair shake.

Between 2015 and 2024, global insured catastrophe losses exploded. Forecasts now predict they'll hit around $145 billion for 2025. That surge in costs from hurricanes, floods, and wildfires has led directly to a spike in disputed property claims. Insurers are now actively trying to limit their exposure by interpreting policy language as narrowly as possible and denying claims based on complex exclusions. It’s creating more friction than ever.

This reality means you have to be ready for a fight from day one. You can dive into our other resources for more on handling insurance claims and disputes, but the key takeaway is this: don't assume your loyalty as a customer will be rewarded.

Assume you'll have to fight for what you're rightfully owed.

Using Your Policy To Build An Ironclad Case

Let's be blunt: your insurance policy is the rulebook for your claim, and it's intentionally written in dense, confusing language. Carriers like Allstate and State Farm are banking on the fact that you’ll never actually read the fine print.

Not reading it is a massive mistake. That policy document is the most powerful weapon you have in a dispute.

Think of it this way—it's the contract that defines your entire relationship with the insurance company. When they deny or underpay your claim, they're essentially saying some clause in that contract gives them the right. Your job is to grab that same contract and prove them wrong, using their own words.

Decoding the Language Insurers Use to Confuse You

First things first, find your Declarations Page. This is usually the first page or two and acts as a summary. It lists your name, property address, policy number, and most importantly, your coverage limits. It gives you the big picture of what’s covered and for how much.

From there, you need to hunt down the sections that spell out the rules of the game—what you have to do, and what they're supposed to do.

- Duties After a Loss: This is a checklist of your responsibilities. It’ll tell you exactly what you must do after a loss, like giving them "prompt notice" and protecting the property from more damage. Insurers absolutely love to find a misstep here to justify a denial.

- Loss Settlement Provisions: This part explains how they calculate what they owe you. It's where you'll find critical terms like Actual Cash Value (ACV) and Replacement Cost Value (RCV), which are ground zero for most payment disputes.

This knowledge flips the script, turning the policy from a confusing mess into a clear roadmap for your fight.

An insurance policy is what’s legally known as a "contract of adhesion." This means you had zero input into its terms—you could only "adhere" to it by paying your premiums. Because of this, courts often rule that any vague or ambiguous language must be interpreted in favor of you, the policyholder. Never forget that.

Finding Hidden Coverage in Endorsements and Clauses

The real money is often buried in the endorsements and add-on clauses. These are modifications to the standard policy that can unlock thousands of dollars in coverage your adjuster conveniently "forgot" to mention.

You might have endorsements for things like bringing your property up to current building codes, covering debris removal, or providing an extended replacement cost buffer. These can dramatically increase your total settlement.

Comb through your policy and find these riders. I promise you, the insurance company will not volunteer this information. It’s on you to find the language that backs up your demand for a larger payout.

Case Study: A Business Owner's Victory Lap

A restaurant owner in Raleigh, NC, was hit by a devastating fire that shut him down for months. His insurance company’s initial business interruption settlement was an insult, arguing that his "period of restoration" was over the second the basic repairs were done.

But this owner had read his policy. He pointed to a single sentence in his Business Interruption clause stating the restoration period continued until his business was back to its "normal level of operations."

He proved that just because the doors were back open didn't mean his customer traffic had recovered. Armed with that one sentence, his public adjuster fought for and won a settlement nearly three times the original offer. It was enough to cover the full, painful period it took to rebuild his clientele. That’s how a few words in a contract can completely change the game.

Gathering Evidence Your Insurer Cannot Deny

Let's be clear: the insurance company's adjuster has already built a case against you. It’s a case meticulously designed to protect their financial interests and justify the lowest possible payout.

Now it's your turn. You need to build your own case—one founded on such undeniable proof that a giant like State Farm or Allstate can't just brush it aside.

This is where the real fight begins. It’s not about snapping a few quick photos. It’s about building a comprehensive evidence package that systematically picks apart the insurer’s lowball assessment and proves, dollar by dollar, what you are actually owed.

Creating an Airtight Inventory of Your Loss

Your first job is to document every single thing that was damaged or destroyed. Insurers thrive on vague claims because they’re easy to undervalue. Your mission is to get painstakingly specific.

Go room by room and create a detailed inventory list. For every single item, you need to include:

- Item Description: Be specific. Include the brand, model, and serial number if you have it. "Samsung 55-inch QLED TV" has power; "television" does not.

- Age and Condition: Be honest about the item's state before the loss.

- Original Purchase Price: Dig up receipts, bank statements, or credit card records.

- Replacement Cost: Research what it would cost to buy a new, similar item today. This is absolutely critical for Replacement Cost Value (RCV) policies.

I know this level of detail feels tedious, but it is non-negotiable in a serious dispute. Each line item adds up, transforming a fuzzy "contents damage" number into a hard, defensible figure that's much tougher for an adjuster to argue with.

The company adjuster walks in with a badge and a clipboard, but you have the home-field advantage. You know your property better than anyone. Use that knowledge to build a record so detailed it overwhelms their attempts to generalize and devalue your loss.

Securing Independent Estimates from Real Contractors

Never, ever accept the estimate from the insurer's "preferred contractor" as the final word. These vendors often have cozy relationships with the insurance companies that send them business, and their estimates can mysteriously align with the insurer's low settlement target.

You need to get your own independent estimates from reputable, local contractors who work for you, not the insurance company. Get at least two or three detailed bids for the repairs. These quotes must break down the costs for labor and materials line by line, giving you a real-world price for the work required to put your property back together the right way.

These competing estimates are one of the most powerful negotiation tools you have. They expose the insurer's lowball offer for what it truly is—an attempt to cut corners at your expense.

Building Your Communication and Evidence Log

From the second the damage happens, start a meticulous log of every single interaction related to your claim. Think of it as a communication journal that becomes a timeline of your case, capable of exposing an insurer's delay tactics or contradictory statements.

Document every phone call, email, and letter. Note the date, time, the name of the person you dealt with, and a quick summary of what was discussed. Save everything. This log is your official record, and it can be priceless if your dispute escalates.

Case Study: A Homeowner's Photos Dismantle the Insurer's Timeline

A homeowner in Virginia was facing a flat-out denial on a major water damage claim. The insurance company's story was that the damage was from long-term neglect, claiming their adjuster found evidence the leak had been happening for weeks.

But the homeowner was meticulous. He had taken timestamped photos of that exact area just five days before the pipe burst while he was changing a filter. The photos showed the wall was perfectly dry and intact. He handed his photo log over to his public adjuster.

Armed with this irrefutable, timestamped proof, the public adjuster completely dismantled the insurance company's narrative. The insurer's "expert" assessment crumbled. Faced with evidence that torpedoed their timeline, the company had no choice but to reverse its wrongful denial and pay the claim in full.

Writing A Dispute Letter That Gets A Response

Let's be clear: your formal dispute letter is not just a complaint. It's a legal document. It puts the insurance company on notice that you're not accepting their decision and are prepared to fight for what you're owed. Drafting a professional, evidence-backed letter is the first real move you make to take back control and force the carrier to give your claim a serious second look.

This isn't the time to vent your anger and frustration. That's what they expect. Instead, you're going to build a calm, logical, evidence-based argument that's simply too strong for them to brush aside. A firm but professional tone is critical—you want to be seen as a serious problem for their bottom line, not just another angry customer they can ignore.

The Bones Of A Letter They Can't Ignore

To get their attention, your letter has to be organized, direct, and easy to follow. Remember, you're dealing with a massive bureaucracy. They respond to structured information, not emotional stories. Every good dispute letter I've seen follows a specific framework designed to get right to the point.

Make sure your letter clearly includes:

- Your Claim Vitals: Start with the basics right at the top. Your full name, the address of the damaged property, the date of the loss, and—most importantly—your claim number. Put that claim number on every single page you send them.

- A No-Nonsense Statement of Disagreement: Get straight to it. In the first paragraph, state plainly that you are formally disputing their decision. For example: "I am writing to formally dispute the settlement offer of $35,000 detailed in your letter dated [Date], as it is grossly insufficient to cover the actual costs of repair."

- Throw Their Own Policy Back at Them: This is where you show them you've done your homework. Cite the specific sections of your policy that back up your claim. Refer to the "Loss Settlement Provisions" or a specific endorsement for "Code Upgrades." This immediately signals that you're basing your dispute on the legal contract between you, not just your opinion.

A well-structured letter forces them to address your specific points head-on. It makes it much harder for them to send you another generic form letter. This is how you start taking apart their weak arguments piece by piece.

A powerful dispute letter does one crucial thing: it shifts the burden of proof back onto the insurance company. By laying out your evidence and citing their own policy language, you are legally requiring them to justify their lowball offer with something more than their adjuster's opinion.

Laying Out Your Evidence

Think of your letter as the cover sheet for the mountain of proof you’ve gathered. Don’t just tell them you have evidence; build your argument around it. Your goal is to walk the claims manager step-by-step through your logic, from your initial disagreement to the dollar amount you are demanding.

You need to organize your points methodically:

- Introduce Your Contractor's Estimate: State that you have an independent estimate from a licensed contractor and that it is attached. Highlight the total amount and call out the major differences between their adjuster’s scope of work and yours.

- Point to Your Proof: Reference the documentation you've compiled. For example: "Attached you will find my 15-page inventory of damaged personal property, which totals $22,500 in replacement costs. This is substantially higher than the $8,000 allotted in your estimate." Mention your photo log, your damage journal, and anything else you have.

- Demand a Specific Number and a Deadline: This is non-negotiable. Don't end by asking them to "reconsider." You must end with a clear, specific demand. "I demand a revised settlement of $78,500, which reflects the true cost of repairs as documented in the attached contractor's estimate." Then, give them a deadline—15 business days is reasonable—to provide a full written response.

This creates urgency and stops them from just putting your file on the bottom of the pile. It turns your letter from a passive request into an active demand for the money you are contractually owed.

When To Escalate The Fight And Hire A Public Adjuster

You've done everything right. You’ve documented the damage, combed through your policy, gathered independent estimates, and even sent a powerful dispute letter demanding what you’re owed. And yet, the insurance company won't budge.

This is the moment most policyholders realize they aren't just in a disagreement. They're in a fight against a multi-billion dollar corporation that has stacked the deck against them from the start. This is when you stop going it alone and bring in a professional advocate: a public adjuster.

A public adjuster is an insurance company's worst nightmare. Unlike their adjuster who works to protect their bottom line, a public adjuster is a state-licensed professional who works exclusively for you. Their only goal is to force the insurer to pay the maximum, fair settlement you're entitled to under your policy.

Clear Signals It's Time For Professional Help

Knowing when to call for backup is crucial. You don't have to wait for a final denial to realize you're outgunned—the warning signs often pop up long before you hit a total dead end.

Here are the undeniable signals that it's time to hire a public adjuster:

- You've received a major lowball offer. If their offer is 25% or more below your contractor's detailed estimate, that's not a simple miscalculation. It’s a deliberate tactic.

- Your claim has dragged on for months. Delays are a classic strategy to wear you down. If your claim has stalled for more than 60-90 days without a clear path forward, they're hoping you’ll just give up.

- The adjuster is unresponsive or dismissive. Are your calls and emails being ignored? Is your evidence being waved away without a valid reason? That’s a clear sign of bad faith.

- The damage is complex and extensive. After a major fire, hurricane, or business interruption, the scope of the loss is massive. A public adjuster has the expertise to find and document all the damage the company adjuster will conveniently "miss."

The decision to bring in a pro is often tied to the scale of your loss. It's no surprise that policyholders are far more likely to hire a public adjuster for larger claims. That’s because contested items like building code upgrades, contents valuation, and business interruption calculations can swing the final settlement by 10% to 40% or more.

A Case Study In Turning The Tables

Think about a business owner in Apex, NC, whose commercial property suffered a catastrophic fire. Their insurer, a major national carrier, dragged their feet for months before finally presenting a settlement that wouldn't even cover half the rebuilding costs. Why? The company’s adjuster had completely missed critical smoke and structural damage hidden within the walls.

Frustrated and on the brink of financial ruin, the owner hired a public adjuster.

The P.A. immediately brought in his own team of engineers and smoke remediation experts. They ran a forensic-level investigation, using thermal imaging and moisture meters to uncover thousands in hidden damages. He then built an ironclad claim package, citing the specific policy language and building codes the insurer had conveniently ignored.

The result? The public adjuster reopened negotiations and secured a final settlement that was more than double the insurance company's original pathetic offer. This is the real-world difference an expert advocate makes. They level the playing field.

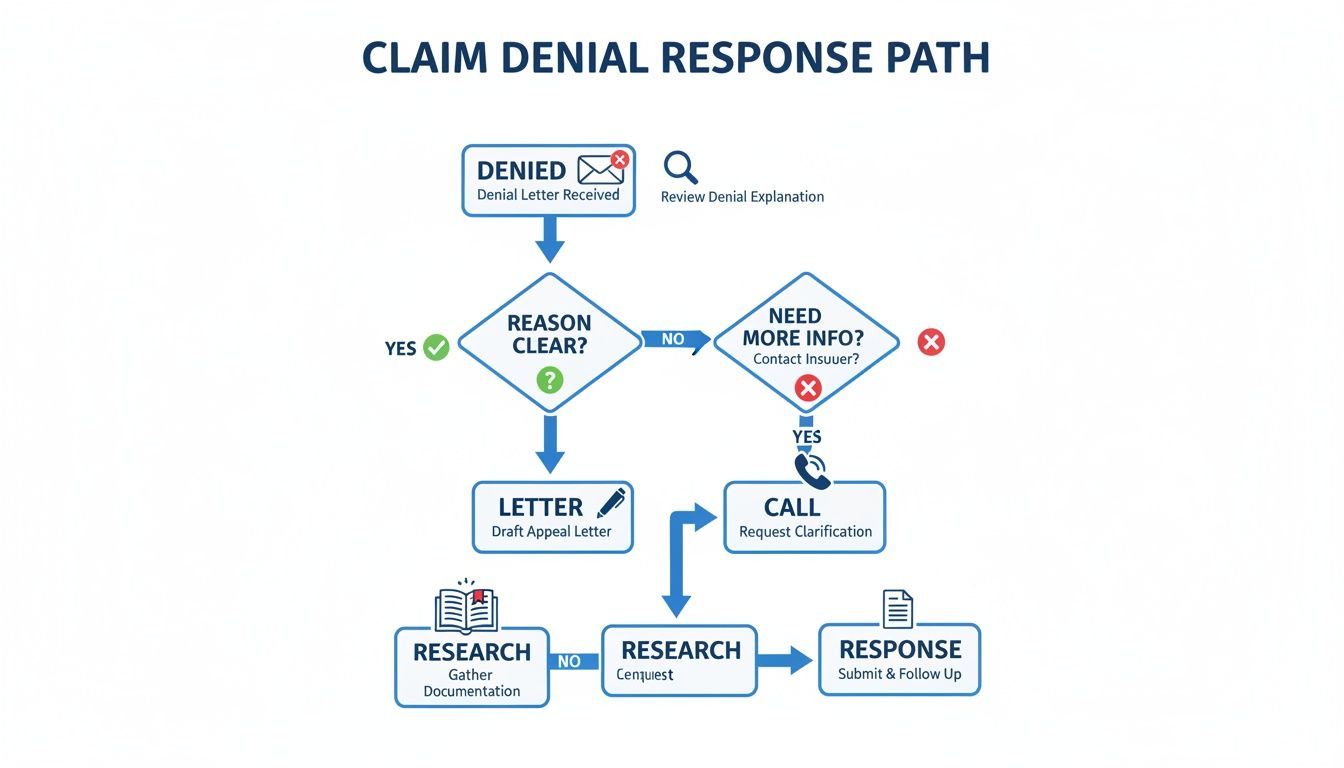

This visual decision tree gives you a simplified roadmap for what to do after getting that dreaded denial letter.

As the flowchart shows, your first move after a denial should always be a methodical, evidence-based response—not an emotional one. A public adjuster makes sure that response has the professional weight it needs to get their attention.

You don't have to just accept a bad-faith offer from giants like State Farm or Allstate. If you're getting the runaround, it's time to get an expert in your corner. If you want to dive deeper, you can learn more about what a public adjuster is and how they can help you with your insurance claim dispute. They know the tactics, they know the policy language, and they know how to make insurers pay what they rightfully owe.

Common Questions We Hear About Insurance Claim Disputes

When you’re trying to navigate an insurance claim dispute, it can feel like you've been dropped into a maze of legal jargon and stall tactics. Property owners who realize their insurer isn't playing fair almost always have the same urgent questions.

Here are some straightforward answers to the questions we get asked most often. Our goal is to give you clarity and confidence during what we know is a deeply stressful time.

How Long Do I Have to Dispute a Denied Claim?

This is a huge, time-sensitive question. In states like North Carolina and Virginia, you’re typically up against a statute of limitations that gives you three years from the date of the loss to take legal action against your insurer.

But don't let that fool you. Your policy itself is a contract, and it almost certainly contains a "Suit Against Us" clause. This provision often shortens your window to file a lawsuit to just one or two years. Read it immediately.

If you miss that contractual deadline, it’s game over. Your right to recover the money you’re owed is gone, no matter how solid your case is.

An insurer's denial letter isn't the end of the road; it's the start of a new clock. You have to act fast and know your deadlines, because companies like State Farm and Allstate are more than happy to let time run out on your rights.

What Is the Appraisal Clause and When Should I Use It?

The appraisal clause is a powerful but often misunderstood tool baked into most property insurance policies. Think of it as a form of alternative dispute resolution designed to settle one specific thing: disagreements over the amount of the loss. It doesn't deal with whether the damage is covered in the first place.

Here’s the process in a nutshell:

- You hire your own independent, competent appraiser, and the insurance company hires theirs.

- Those two appraisers then agree on a neutral third party, called an umpire.

- The two appraisers review all the evidence and try to agree on the value of the damage. If they can’t, they submit their differences to the umpire.

- An agreement between any two of the three (your appraiser and the umpire, for instance) results in a legally binding award.

You should push for appraisal when the fight is purely about the numbers—like the cost of materials, the scope of repairs, or the value of your damaged contents. It's almost always faster and cheaper than dragging the fight into a courtroom.

Can My Insurer Drop Me for Fighting Back?

This is a common fear. Policyholders worry that filing a dispute, hiring a public adjuster, or just pushing back will get their policy canceled or non-renewed.

While an insurance company can choose to non-renew a policy for various legitimate reasons (like filing way too many claims in a short time), it is flat-out illegal for them to drop your coverage as direct retaliation for disputing a single claim in good faith.

Laws in North Carolina, Virginia, and most other states stop insurers from punishing you just for exercising your contractual right to disagree. Fighting for a fair payout on a legitimate claim is not valid grounds for cancellation. If you think you've been dropped as a form of payback, you need to get professional advice right away.

Should I Hire a Public Adjuster or an Attorney?

This is a critical strategic decision. While both are on your side, they play different positions on the team.

A public adjuster is your best first move when the dispute is over the scope and value of your damages. We’re experts in assessing property damage, digging into the fine print of policy language, and going head-to-head with the insurance company's negotiators. We build the factual, evidence-based case for what you're truly owed.

An attorney enters the picture when the fight turns to purely legal issues. You need to lawyer up if:

- Your insurer has flatly and wrongfully denied coverage.

- You’re accusing the insurance company of acting in bad faith (like intentionally delaying your claim or misrepresenting facts).

- You’ve hit a wall and need to file a lawsuit to force their hand.

Often, the most powerful approach is a one-two punch. A public adjuster builds the ironclad case establishing the full value of your loss. If the insurer still refuses to pay up, that rock-solid evidence package gets handed to an attorney to use as ammunition in court.

Facing a stubborn insurance company can feel like an impossible fight, but you don’t have to do it alone. The team at For The Public Adjusters, Inc. has the expertise to dismantle the insurer's arguments and secure the full, fair settlement you deserve. If you're dealing with a denied, delayed, or underpaid claim in North Carolina or Virginia, contact us for a no-cost claim review today.