Let's get one thing straight before we dive in: your insurance policy isn't a friendly guide or a safety net. It’s a legal contract, engineered from the ground up by the insurance company’s lawyers to protect their bottom line—not necessarily your property.

This is a tough pill to swallow, but you have to accept it. Every word, every comma, and every clause in that massive document was chosen with a single goal in mind: limiting what the insurance company has to pay you when you file a claim.

Giant carriers like State Farm and Allstate have spent decades perfecting the art of confusing legal jargon. They bank on the fact that you'll never actually read the fine print until your house is flooded or a tree is sitting in your living room. By then, it's often too late, and they are masters of the delay, deny, and defend strategy.

That’s why you have to shift your mindset. See this document for what it is: a one-sided rulebook for a fight you might have to have. A simple misunderstanding of a term like "actual cash value" or a missed condition buried on page 47 could cost you tens of thousands of dollars on a perfectly valid claim.

This guide will walk you through how to dissect your policy with the healthy skepticism it deserves. It’s not about becoming an attorney overnight. It’s about learning to spot the traps so you can fight back effectively when your insurer isn’t playing fair. For a deeper dive into the basics, check out our guide on understanding homeowners insurance coverage.

The Strategic Reading Order

Don't just start on page one and read until your eyes glaze over. That’s what they want you to do. It’s overwhelming and completely ineffective. You need a battle plan.

The trick is to tackle the sections in the order of importance—the parts that hold the most power when there's a dispute with your insurance company.

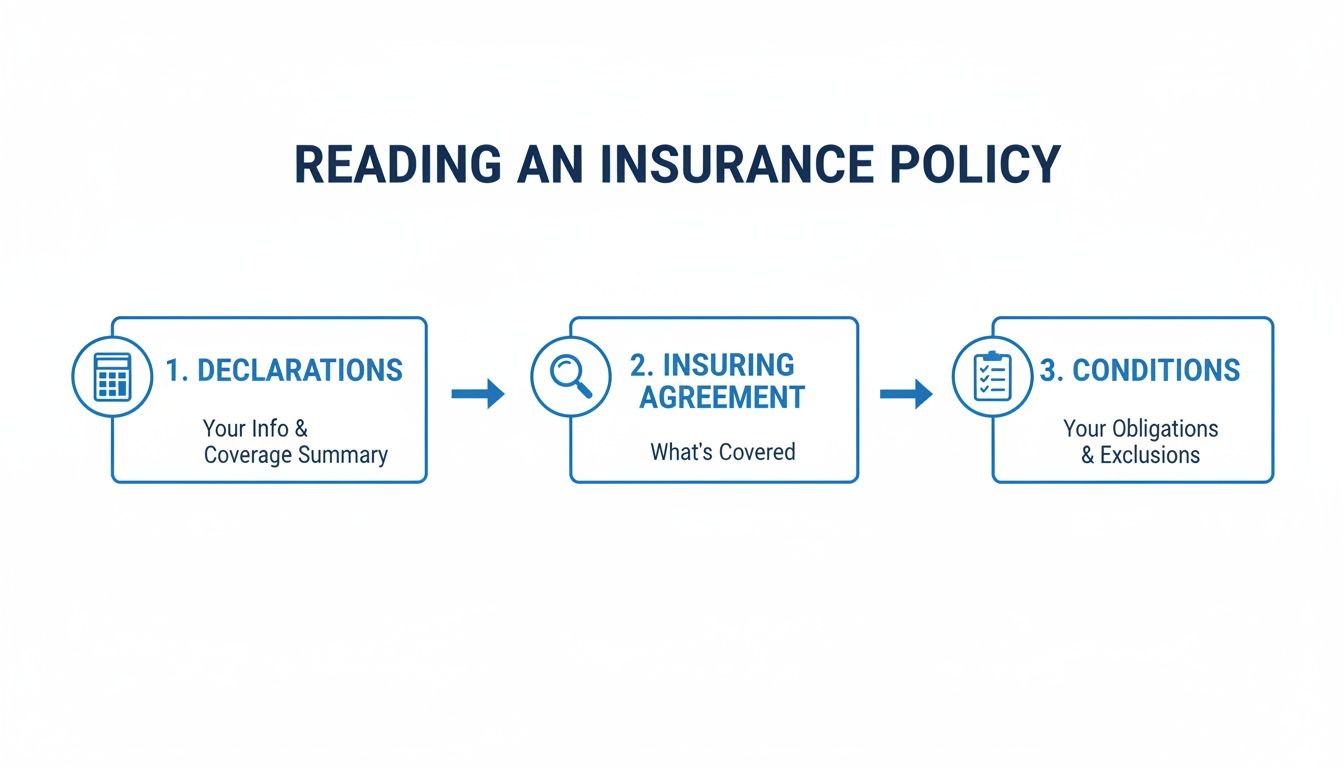

You always start with the Declarations Page to see your specific coverage numbers. Then, you move to the Insuring Agreement to understand the basic promise the company is making. Finally, you scrutinize the Exclusions, Conditions, and Endorsements—this is where they hide all the loopholes and rules you have to follow to dispute an underpaid claim.

Here's a quick overview of the essential parts of your policy and what they control. Understanding this structure is the first step to decoding your coverage.

The 5 Key Sections of Your Insurance Policy

| Policy Section | What It Tells You |

|---|---|

| Declarations | The "who, what, where, and how much" summary of your policy. It lists your name, property address, policy number, coverage limits, and deductibles. |

| Insuring Agreement | The insurance company's broad promise to cover you for specific types of losses (like fire or theft). This is the foundation of the contract. |

| Exclusions | The list of what is NOT covered. This is one of the most critical sections, detailing perils like floods, earthquakes, or neglect that are explicitly left out. |

| Conditions | The rulebook. It outlines your responsibilities after a loss (like mitigating further damage and providing documentation) and the insurer's obligations. |

| Endorsements | These are modifications or add-ons that change the standard policy. They can either add or remove coverage, so they're incredibly important to review. |

Approaching your policy with this strategic, skeptical mindset is the only way to truly understand what you're paying for and to prepare yourself for a fight if you ever have to dispute a major claim with your insurance company.

Start With the Declarations Page to Find the Numbers That Matter

If you only read one page of your entire insurance policy, make it this one.

The Declarations Page, or "Dec Page," is the cheat sheet for your whole policy. While the rest of the binder is packed with dense, confusing legal language, this front page boils it all down to the hard numbers that define your financial protection.

But I have to be blunt: it's also a minefield. It's the first place an insurance company's adjuster will look for an easy way out of paying your claim fairly.

An adjuster from a carrier like Allstate or State Farm is trained to hunt for discrepancies. A misspelled name, a wrong address, or an incorrect policy date isn't just a typo—it's a weapon they can use to delay, underpay, or flat-out deny your claim. They aren't looking for ways to help you; they are looking for reasons not to pay, because their performance is often judged by how little they pay out.

This is exactly why you have to master this page. It sets the financial boundaries for everything that follows and gives you the core facts you need to hold your insurer’s feet to the fire when you have to dispute their settlement offer.

Key Details to Verify Immediately

Your first move is a quick audit for accuracy. Never assume anything is correct just because your insurance company printed it. Mistakes happen constantly, and I can promise you, they will always work against you, not for you.

- Named Insured: Is your name spelled perfectly? If it’s a business, is the full, legal name listed? If your spouse or a business partner has an interest in the property, are they on there, too? An adjuster will use any mistake here to argue about who even has the right to the money.

- Property Address: Is the address listed the exact location of the damaged property? This seems basic, but you’d be shocked how often this is wrong, especially for rental properties or businesses with multiple locations.

- Policy Period: Check the effective and expiration dates. If your loss happened one day outside of this window, your claim is dead on arrival. It's an instant denial.

Getting these details right is foundational. If they’re wrong, you’re starting the fight with one hand tied behind your back.

Scrutinize Your Coverage Limits and Deductibles

Beyond the basics, the Dec Page lays out the most critical financial figures in your policy. This is where the insurance company loves to hide nasty surprises in plain sight, counting on the fact that most people won't understand what they're looking at.

When you open a personal or commercial insurance policy, the Declarations Page is the single most important page to read first because it condenses all the key numeric terms. You must verify that the policy period dates are correct, confirm the named insured is spelled exactly right, check the stated coverage limits, and ensure the deductible amount matches what you agreed to, as mismatches here are a common source of claim disputes. For a broader look at how these numbers shape the industry, you can explore these global insurance market insights.

Case Study: A Public Adjuster Uncovers a Costly Deductible Trick

A public adjuster worked with a homeowner in Raleigh, NC, who thought they had a simple $1,000 deductible. After a hailstorm ripped through their neighborhood, causing $40,000 in damage, they filed a claim. The insurance company adjuster immediately pointed to a "1% Wind/Hail" deductible listed on their Dec Page. Since their home was insured for $500,000, their actual out-of-pocket cost for that storm was $5,000. The homeowner was shocked, but their public adjuster had spotted this on day one and was prepared to fight, ensuring the insurance company didn't lowball the rest of the repair costs to make up for the high deductible.

This is why you have to dig into the most important numbers on the page:

- Coverage Limits: These are the absolute maximum dollar amounts the insurer will pay for different types of losses (like your house itself, your personal belongings, or your business equipment). Does that "Dwelling" limit actually reflect what it would cost to rebuild your home today? Insurers often rely on outdated software that leaves you dangerously underinsured from the start.

- Deductibles: This is what you have to pay before the insurance company pays a single dime. But look closer—it's rarely just one number. You might have a standard deductible for a fire, but a much larger, separate percentage-based deductible for hurricanes, wind, or hail. It's a common trick, especially in coastal states like North Carolina and Virginia, designed to shift huge costs back onto you.

Where the Real Fight Begins: Decoding Your Policy's Fine Print

Once you've confirmed the numbers on your Declarations Page are correct, you have to dive into the core of the policy itself. This is where the real work—and the real risk—lies. You’re now entering the territory of the Insuring Agreement, Definitions, and Exclusions.

This trio of sections is precisely where insurance companies build their case to shrink, delay, and flat-out deny claims.

The Insuring Agreement seems simple enough. It’s the carrier’s broad promise to cover you for a "direct physical loss." But don’t get comfortable, because that promise is almost immediately dismantled by the pages that follow.

Think of it this way: the Insuring Agreement is the big, shiny promise they make on the front page. The Definitions and Exclusions are the pages of fine print that take most of it back. This is how a seemingly comprehensive "all-risk" policy suddenly becomes riddled with loopholes you never knew existed, giving the adjuster ammunition to use against you.

How Insurers Weaponize Definitions Against You

In the world of insurance, words mean exactly what the company says they mean. The Definitions section isn't just a helpful glossary; it's a minefield where carriers twist everyday language to protect their bottom line. Understanding these definitions is non-negotiable, because a single word can be the difference between a paid claim and a denial letter.

Here are a few terms they absolutely love to manipulate:

- "Collapse": You’d think this means your roof caved in. Simple. But many policies define it as an "abrupt falling down or caving in…with the result that the building…cannot be occupied." An adjuster can—and will—argue that a bowing, unstable wall hasn't technically "collapsed," leaving you with a denied claim on a home that’s no longer safe.

- "Flood": This is the big one. To your insurer, a "flood" is surface water that enters your home from the outside. A pipe bursting and soaking your first floor is a water loss, not a flood. That distinction is everything, because nearly every standard homeowners policy excludes all flood damage.

- "Occurrence": This term determines how many deductibles you have to pay. Let’s say a hurricane's high winds rip shingles off your roof on a Saturday, and the rain that follows on Sunday causes a massive interior leak. Your carrier might try to call these two separate "occurrences," forcing you to pay two separate, and often very large, deductibles.

These definitions aren't there by accident. They are carefully engineered legal traps. The carrier’s adjuster is trained to apply the most narrow, restrictive interpretation possible to limit the company’s payout.

The Exclusion Section: Your Adjuster's Playbook for Denial

This is it. This is the section that lists everything your insurance company will not pay for, period. For the company adjuster, the Exclusions section is their best friend. For you, it’s a list of potential knockout blows to your claim dispute.

Case Study: The Mold Exclusion Battle.

In a notable court case, De-Graw Construction, Inc. v. Travelers Indemnity Co. of America, the insurance company tried to deny a claim based on a mold exclusion after water damage occurred. The court, however, sided with the policyholder, ruling that if the mold was a direct result of a covered event (like a pipe burst), the exclusion didn't apply. This shows how crucial it is to fight back against an adjuster's initial denial, as they often rely on broad exclusions that may not hold up under scrutiny.

Pay close attention to these common, and costly, exclusions:

- Ordinance or Law: If your home is damaged and the city requires you to upgrade the plumbing or electrical systems to meet current building codes, your standard policy won't pay for it. You need a specific endorsement for that.

- Wear and Tear: Insurers don't pay for things that fail because they're old. Adjusters love to use this to deny claims for older roofs or plumbing systems, even when it was a storm or sudden event that delivered the final blow.

- Earth Movement: This knocks out coverage for earthquakes, landslides, and sinkholes.

- Water Damage: This is a tricky category. It typically excludes damage from floods (see above), sewer backups, and slow, gradual leaks. These gaps can leave you exposed to tens of thousands of dollars in uncovered damages.

The Unforgiving World of Federal Flood Policies

If your home is damaged by a flood, you’re not dealing with your friendly neighborhood insurance agent. You’re in the world of the National Flood Insurance Program (NFIP), and it is a completely different, unforgiving beast. These claims are handled by FEMA through a Write Your Own (WYO) company adjuster, and they are notoriously difficult.

NFIP policies are rigid, federally regulated contracts. The adjusters who handle these claims are experts at sticking to the letter of the law, which is designed to limit payouts. They will deny payment for almost anything in a basement besides a furnace or a washer/dryer. They are notoriously strict about what they’ll pay for debris removal and additional living expenses.

Trying to fight an NFIP denial on your own is, frankly, a losing battle. The system is designed to be confusing and wear you down. A public adjuster who specializes in NFIP flood claims is often the only way to cut through the federal bureaucracy and get the fair settlement you deserve.

Uncovering Hidden Financial Traps in Your Policy

That big, reassuring Dwelling Coverage number you saw on your Declarations Page? It’s often more of a marketing tool than a promise. It gives you a false sense of security while the real, much smaller numbers are buried deep within the policy's fine print.

These are called sub-limits, and they are one of the most effective financial traps insurers use to gut your claim. Think of it as a cap—a smaller dollar amount for a specific type of damage that overrides your main policy limit.

It’s a classic bait-and-switch. Your policy might boast a $500,000 dwelling limit, but when a sewer line backs up and floods your basement, the adjuster will gleefully point to a tiny sub-limit for "Water Backup and Sump Pump Overflow." Suddenly, your payout is capped at a mere $5,000 or $10,000. That won't even scratch the surface of the cleanup and repair costs.

Hunting for Deceptive Sub-Limits

Insurance companies know exactly which disasters are common and costly, so they build in sub-limits to protect their bottom line on those very claims. You need to actively hunt for these capped amounts to effectively dispute a lowball offer. They’re often hidden within the main policy forms or tacked on via endorsements.

Here are the usual suspects where insurers sneak in low sub-limits:

- Mold Remediation: After a water loss, mold is almost a given. But many policies cap the cleanup at $5,000—a fraction of what a real remediation job costs.

- Debris Removal: After a fire or major storm, hauling away what’s left of your property can be shockingly expensive. This is often capped at a small percentage of your total loss.

- Ordinance or Law: This coverage, if you have it at all, is often limited to just 10% of your dwelling limit. That's rarely enough to cover mandatory code upgrades during a major rebuild.

- Business Interruption: For business owners, the standard coverage period might be far too short to get your operations back up and running, leaving you with a massive, uncovered income loss.

Policies often list one big limit and then multiple sub-limits that gut your recovery for specific events. As insurers face rising costs, they are leaning more and more on these traps to manage their losses, according to global insurance trends. It’s on you to find them before you have to dispute a claim.

Endorsements: The Insurer's Secret Weapon

If sub-limits are hidden traps, endorsements are the insurer's secret weapon. An endorsement is just an amendment or add-on to your standard policy. It can either expand your coverage or, more frequently, take it away.

Insurers love using endorsements to quietly introduce new exclusions or change the rules of the game. An adjuster will treat an endorsement as if it's the most important page in your policy because it overrides whatever the standard form says. It’s their trump card.

Success Story: Overcoming a Devastating Endorsement with a Public Adjuster

A business owner in Virginia had what he thought was a great policy with a low deductible. After a severe hailstorm destroyed his commercial roof, he filed a claim. The adjuster from his carrier arrived and immediately pulled out an endorsement titled "Amendatory Endorsement – Windstorm or Hail." Buried in that single page was a clause that changed his deductible for hail damage from a flat $2,500 to 5% of the building's insured value. His $1.5 million building now had a $75,000 deductible. The business owner hired a public adjuster who immediately took over the dispute. The PA proved the insurance company undervalued the total cost of replacement by over $100,000, forcing a much larger payout that covered the massive deductible and saved the business from financial ruin.

This is exactly why you must read every single endorsement. Look for language that adds new exclusions, imposes massive percentage-based deductibles for specific perils like wind or hail, or alters how your property is valued. Understanding the difference between payment methods is crucial; for more detail, you can learn how ACV vs. RCV impacts your claim payout here.

Ignoring these seemingly boring add-on pages is a guaranteed way to be blindsided by a lowball settlement offer when you need your coverage the most.

How Adjusters Weaponize Your Policy Conditions

You’ve made it past the maze of definitions and exclusions, only to land in the "Conditions" section. Think of this as the insurance company's rulebook—a list of duties you absolutely must perform perfectly after a loss.

This isn’t friendly advice. It’s a list of tripwires. Any misstep, no matter how small, gives the adjuster a contractual reason to delay, slash, or outright deny your claim.

Adjusters from big carriers like State Farm and Allstate are not your partners in recovery. They are highly trained to pick apart your every move, searching for any failure to comply with these conditions. For them, this section is a weapon, and they know that a homeowner under the extreme stress of a disaster is bound to make a mistake.

The Insurer's Playbook for Denial

The "Conditions" section lays out all your duties after a loss. While complying is mandatory, how you comply will either protect your right to a fair settlement or hand the insurance company the very excuse it needs to kill your claim.

Your most critical post-loss duties usually include these three things:

- Prompt Notice: Your policy will say you must report the claim "promptly" or "as soon as practicable." Those vague words are there for a reason. An adjuster can argue that waiting a few weeks to report water damage you just discovered wasn't "prompt" enough, giving them an immediate reason to deny coverage.

- Protecting Property: You have a duty to mitigate further damage. That means getting a tarp on a busted roof or boarding up a shattered window. If you don't, and a rainstorm causes more damage inside, the insurer will refuse to pay for that subsequent damage. They’ll blame your inaction, not the original storm.

- Cooperating with the Investigation: This is the most dangerous condition of all. On the surface, it sounds reasonable: provide records, answer questions, and allow inspections. In reality, it’s a blank check for the adjuster to make endless, overwhelming demands.

Fighting Back Against Unreasonable Demands

Insurance companies often treat the "cooperation" clause as your total surrender. It's not.

An adjuster might hit you with a demand for a 50-page inventory of every single item you own, right down to the last sock, and give you an impossibly short deadline to produce it. This is a setup. They know you'll fail, allowing them to claim you were "uncooperative."

They'll also pressure you for a recorded statement immediately after the loss. They want to catch you while you're stressed and confused, hoping you'll misspeak or guess at an answer. They will twist your words and use any inconsistency to accuse you of misrepresentation and deny the claim.

Never give a recorded statement without first talking to a public adjuster. It's a cross-examination, not a friendly chat. The adjuster’s questions are engineered to find contradictions, not to help you.

Watch out for a Reservation of Rights letter. This is a formal notice that the insurer is investigating your claim but is reserving the right to deny it later. This is a massive red flag. It means they are actively building a case against you. You must understand what this document means for your claim.

For example, when dealing with water damage, an adjuster will use policy conditions to question the timing of the loss. Knowing the eight common signs of water damage in walls can help you anticipate their arguments that the damage is "long-term" and therefore not covered.

Success Story: The Business Owner Who Fought Back Against Delay Tactics

A North Carolina business owner had a devastating fire. The insurance company's adjuster buried him in demands for years of financial records, most of which were irrelevant, all while dragging the investigation to a halt. The owner hired a public adjuster. We immediately took over, provided only the legally required documents, and sent a formal letter demanding the insurer stop the bad-faith delay tactics. Faced with a professional who knew the policy and the law, the carrier’s tone changed overnight. The claim was paid in full, saving the business from being bled dry by the delay.

Common Questions About Fighting Your Insurance Claim

Even after you get a handle on reading your policy, you’re going to hit roadblocks. It’s inevitable. When an insurer decides to make things difficult, homeowners and business owners almost always run into the same old tactics designed to wear them down. Here’s how you fight back.

For a deeper dive into the claims process from start to finish, this guide to navigating home insurance claims is an excellent resource. It gives you the bigger picture for the specific battles we're about to cover.

Knowing your rights—and more importantly, the insurer's obligations—is ground zero for fighting back effectively.

What Is the Difference Between RCV and ACV?

This is a big one. It's probably the most common source of underpayment I see, and the difference can be tens of thousands of dollars on your final check.

- Replacement Cost Value (RCV): This is the bottom line. It's the full, real-world cost to repair or replace your property with similar materials at today's prices. No funny math, no depreciation.

- Actual Cash Value (ACV): This is the number your insurance company wants to talk about. It’s the replacement cost minus depreciation for age and wear-and-tear.

Insurers love to pay only the ACV upfront. They cut you a check that isn't even close to enough to actually get the work done. They then hold back the rest of the money, called recoverable depreciation, and basically dare you to come and get it. It creates an immediate cash-flow crisis for you.

To get that depreciation money released, you have to prove you’ve finished the repairs, which often means paying out of your own pocket first. You fight this by documenting every single penny you spend and aggressively challenging their depreciation math. An adjuster might try to say your 15-year-old roof is 75% depreciated, but we can argue that the roof had years of functional life left, forcing them to use a much more reasonable number.

My Insurer Is Delaying My Claim. What Can I Do?

Let me be blunt: delay tactics are a core strategy for big insurance companies. This isn't an accident or a backlog in the office. The goal is to make you so frustrated and financially desperate that you'll take any lowball offer they throw at you just to be done with it.

Your best weapon against this is relentless, obsessive documentation. You need to build a rock-solid timeline of their failure to act in good faith.

- Log every phone call: Write down the date, time, the person's name, and what was said. Every single time.

- Save all emails: Create a specific folder for every piece of digital communication. No exceptions.

- Use certified mail: For anything important—a request for an update, a demand for a decision—send it via certified mail with a return receipt. This creates a legal paper trail they can't deny receiving.

This isn't just about keeping good records. You're building the foundation for a potential bad faith insurance claim. In states like North Carolina and Virginia, there are specific laws about how fast an insurer has to respond. A public adjuster can take over these communications, citing the exact statutes needed to force their hand and hold them accountable.

Why Hire a Public Adjuster if the Insurer Provides One?

This is the most critical thing to understand. The adjuster your insurance company sends out does not work for you. Period. They are a company employee, and their job is to protect the insurance company’s money. Their goal is to find reasons to pay you as little as possible.

A public adjuster works exclusively for you, the policyholder. We are your licensed advocate, hired to level a playing field that is intentionally tilted in the insurance company's favor.

We are your expert in the fight. We conduct our own damage assessment, read every word of that policy to find coverage you didn't know you had, and handle the entire negotiation to get the maximum settlement you are owed. The numbers don't lie: policyholders who hire a public adjuster consistently get significantly higher payouts—even after our fee—than people who try to fight a multi-billion-dollar corporation on their own.

When you're facing a denied, delayed, or underpaid claim, you don't have to fight alone. The team at For The Public Adjusters, Inc. is ready to review your claim at no cost and show you how to get the full and fair settlement you deserve. Contact us today to take control of your claim. https://forthepublicadjusters.com