When you ask, “will insurance cover roof replacement,” the honest answer is a frustrating maybe. But you need to understand that your insurance company’s goal is often to turn that “maybe” into a hard “no.”

They aren’t on your side. Companies like Allstate and State Farm operate from a calculated playbook designed to delay, underpay, or flat-out deny legitimate claims for storm damage. It’s all about protecting their bottom line, not your property.

The Real Reason Your Insurer Denies Roof Claims

Think of your homeowner’s or business owner’s policy as a rulebook for a high-stakes game. On your side of the board, you have “covered perils”—these are the sudden, accidental events like hailstorms, windstorms, fires, or falling trees that your policy is supposed to protect you from.

On their side, they have “exclusions,” which are all the loopholes, exceptions, and fine print they use to weasel out of paying. Their entire strategy is built around shoving your clear-cut storm damage into that exclusions box.

One of their favorite moves is to dismiss obvious storm damage as simple “wear and tear.” An adjuster, trained to minimize payouts, will walk your roof, look at hail-dented shingles or wind-lifted tabs, and confidently declare it’s just due to age. This is a deliberate tactic designed to make you foot the entire bill for a new roof.

Distinguishing Covered Perils From Insurer Excuses

Getting paid what you’re owed hinges on understanding the difference between what your policy actually covers and the excuses your insurer will invent. A covered peril is a sudden and accidental event. A hailstorm that barrels through and batters your roof in a single afternoon is the textbook definition.

“Wear and tear,” on the other hand, is the slow, gradual decline of materials over many years. Insurers intentionally blur this line because it works to their financial advantage.

The entire fight often boils down to one question: Did a specific, covered event cause the damage, or was the roof already failing? Your insurer will almost always argue it was failing, because that argument saves them a fortune.

This isn’t just a hunch. A 2022 analysis by Quadrant Information Services revealed that a staggering 34% of all property insurance claims in the U.S. are for wind or hail damage. It’s the most common and fiercely contested type of claim out there. This is precisely why insurers have built such aggressive strategies to shut these claims down. You can explore more on how insurers handle these common claims here.

To help you see the game for what it is, here’s a breakdown of legitimate damage versus the excuses you’re likely to hear.

Covered Peril vs. Common Insurer Excuse

| Damage Type | What Your Policy Should Cover | The Insurer’s Likely Excuse |

|---|---|---|

| Hail Damage | Dents, cracks, or granular loss on shingles caused by hailstones hitting the roof. | “That’s just blistering or normal aging. It’s cosmetic, not functional damage.” |

| Wind Damage | Shingles that are lifted, creased, torn, or completely blown off by high winds. | “Those shingles were improperly installed or have reached the end of their lifespan.” |

| Falling Object | Damage from a tree or large branch falling on the roof during a storm. | “The tree was dead or dying, so this is a maintenance issue, not a storm issue.” |

| Sudden Water Leaks | Interior water damage resulting from a storm creating an opening in the roof. | “The leak is from old, deteriorated flashing. That’s a pre-existing maintenance problem.” |

Seeing these excuses in black and white makes it clear: the insurance company’s response is often a pre-scripted denial, not an objective assessment of the facts.

Common Tactics to Deny Your Claim

Insurance companies have a go-to list of arguments they use to fight paying for a full roof replacement. Recognizing their playbook is the first step to beating them at their own game.

They will almost certainly claim one of the following:

- Lack of Maintenance: They’ll say you neglected your roof, and that your neglect—not the F2 tornado that just came through—is the real reason it failed.

- Pre-Existing Damage: The adjuster might assert the damage was already there before the storm, conveniently without any proof to back it up.

- Cosmetic vs. Functional Damage: This is a huge one for metal roofs. They’ll label widespread hail dents as “cosmetic” and refuse to pay, arguing the roof still technically sheds water.

- Manufacturer Defect: In a real stretch, they’ll sometimes try to blame the shingle manufacturer for faulty materials, kicking the can down the road and leaving you in the middle.

You have to understand this adversarial dynamic from the very beginning. When you file a claim, you are not entering a partnership. You are starting a negotiation against a multi-billion dollar company that views your claim as a loss on its balance sheet. Your job is to prove, with overwhelming evidence, that the damage falls squarely under a covered peril, leaving them no room to hide behind their well-worn excuses.

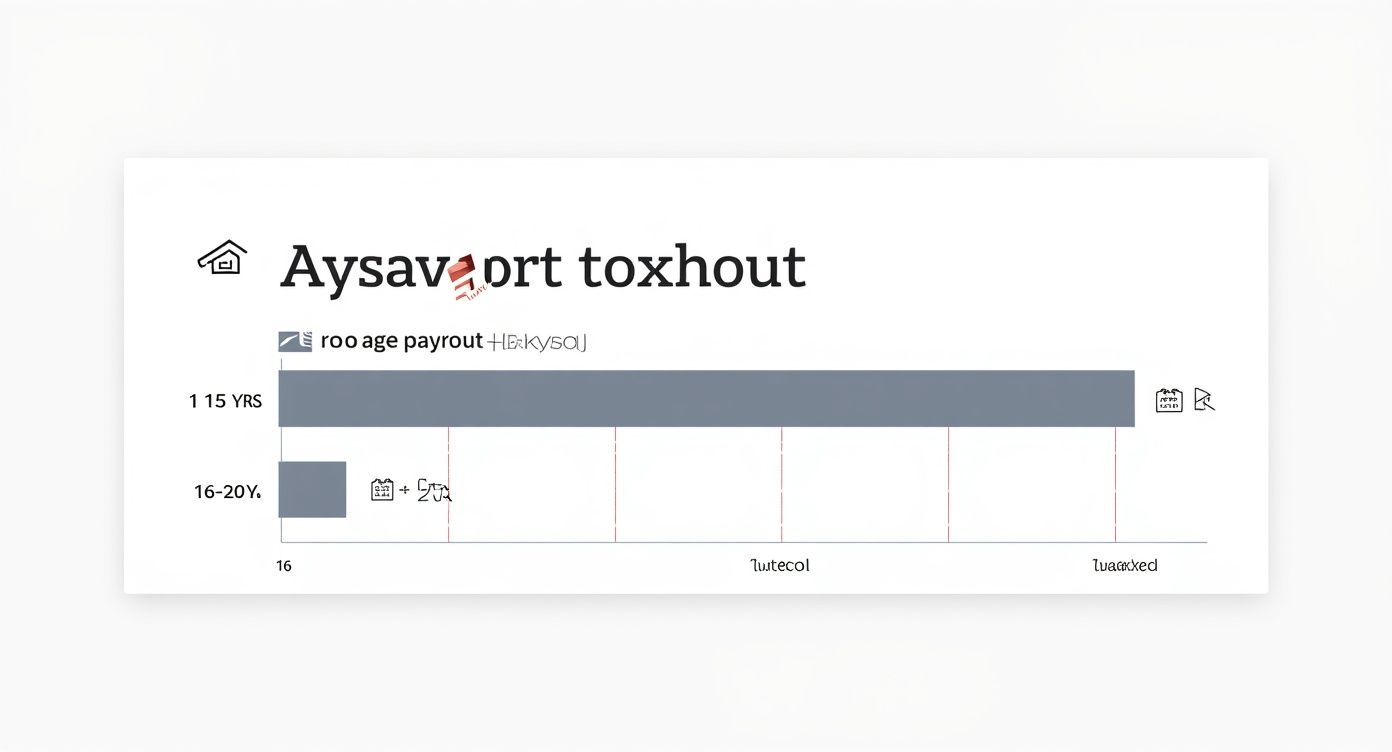

How Insurers Use Your Roof’s Age Against You

One of the sneakiest weapons insurance companies have in their arsenal is your roof’s age. It’s a calculated play. They’ll gladly collect your full premium payments year after year, all while knowing they have a system in place designed to slash their payout if that same aging roof gets hit by a storm.

This isn’t about being fair; it’s about shifting the financial burden right back onto your shoulders.

This trap is often buried in the fine print of your policy, sometimes called a “roof payment schedule” or “age-based depreciation.” It’s a contractual escape hatch that lets them off the hook for a full replacement, even when you have a perfectly valid storm damage claim. They’ve built a system where the longer you stay a loyal customer, the less your policy is actually worth when you need it most.

The Depreciation Game

Insurance giants love this model. It gives them the power to penalize you simply for having a roof that has done its job for more than a decade. The logic is brutally simple: the older your roof gets, the more they can subtract for “depreciation”—their term for normal wear and tear.

They treat your roof like a used car, chipping away at its value every single year.

This becomes a disaster after a hailstorm or major wind event. You see a roof shredded by a covered storm, but your adjuster sees an old, depreciated asset that’s already lost most of its value. They aren’t calculating the cost to make you whole again. They’re calculating the absolute bare minimum they are contractually forced to pay for an old roof.

And this approach is getting more aggressive. Insurers are now far more likely to attack claims for any roof over 15 years old. Some policies now enforce a harsh payment schedule where a roof aged 16 to 20 years might only get you 40% of its replacement cost. If it’s over 21 years old, that can plummet to as low as 20%—and that’s before they subtract your deductible. You can learn more about these damaging roof coverage changes that could gut your homeowner renewal.

The Financial Gut-Punch You Never Saw Coming

Let’s run the numbers to see how devastating this tactic really is. Imagine a windstorm destroys your 18-year-old roof. The contractor gives you a quote for $20,000 for a full replacement.

You file your claim, thinking you’re covered. But then the adjuster points to that “roof payment schedule” buried in your policy. Here’s how it plays out:

- Total Replacement Cost: $20,000

- Insurer’s Payout (40%): $8,000

- Your Out-of-Pocket Cost: $12,000 (plus your deductible!)

Just like that, you’re on the hook for more than half the cost of a new roof, even though you’ve paid your premiums on time for years. This is exactly what the insurance company wanted. Their strategy is designed to leave you with a massive financial shortfall, forcing you to drain your savings to fix storm damage that should have been their responsibility.

This isn’t a mistake in the system; it’s the system working exactly as the insurance companies designed it. They’ve created a policy structure that guarantees they collect maximum premiums while being exposed to minimum risk, especially for homeowners with roofs over 15 years old.

The question, “will insurance cover roof replacement?” gets a lot more complicated when your insurer can legally argue they only owe you for a fraction of the cost. They aren’t protecting your property; they are protecting their profit margins by weaponizing the natural aging process of your home against you. This is why you have to understand every word in your policy and be ready to fight their depreciation games.

Navigating the ACV vs RCV Policy Trap

Let’s be clear: insurance policies are designed to be confusing. They’re packed with dense terminology, and two of the most weaponized terms they use to slash your payout are Actual Cash Value (ACV) and Replacement Cost Value (RCV).

Getting this wrong isn’t just a minor mistake. It can leave you with a financial gap of tens of thousands of dollars when you’re desperately trying to get a straight answer to, “will insurance cover my roof replacement?”

The Real-World Impact of an ACV Policy

Insurance carriers like State Farm and Allstate absolutely love selling ACV policies because they have a built-in excuse to pay you less. An ACV policy gives them the contractual right to subtract depreciation—a fancy word for the value your roof has lost over time just by getting older—from your settlement check.

This means they aren’t paying for what it costs to put a new, working roof over your family’s head today. They’re only paying for the leftover value of your old, storm-battered roof, leaving you to cover a massive shortfall.

Here’s how this trap springs shut in the real world. A hailstorm smashes your 15-year-old roof, and a trusted local roofer gives you a $25,000 quote for a full replacement.

If you have an ACV policy, the adjuster will do some quick, self-serving math:

- Total Replacement Cost: $25,000

- Depreciation Subtracted (60%): -$15,000

- Actual Cash Value (ACV) Payout: $10,000

- Your Out-of-Pocket Cost: A gut-wrenching $15,000 (plus your deductible).

This is the ACV trap in action. You’ve paid your premiums faithfully for years, only to discover your policy was never meant to make you whole. It was written to pay out as little as legally possible.

The infographic below shows just how brutally an aging roof can sink your claim payout.

As you can see, the older your roof gets, the more financial risk the insurance company dumps back on you, no matter how bad the storm was.

Why RCV Coverage is Non-Negotiable

A Replacement Cost Value (RCV) policy is what you thought you were paying for. It’s structured to cover the full cost of replacing your roof with new materials of similar quality, minus your deductible. It’s the only way to be made whole.

With an RCV policy, the insurer typically pays you in two checks:

- First Payment: An initial check for the Actual Cash Value (ACV) of your damaged roof.

- Second Payment: The rest of the money, called recoverable depreciation, is paid out after you’ve had the work done and sent them the final invoice.

But even this two-step process can turn into a battle. Insurance companies are notorious for delaying that second payment or picking apart the contractor’s final bill, hoping you’ll just get exhausted and give up on the money you’re owed.

Crucial Takeaway: An RCV policy is the only real protection you have from a catastrophic financial loss after a storm. An ACV policy is a near-guarantee that you will be underpaid.

To show just how different these outcomes are, let’s compare them side-by-side.

ACV vs. RCV Payout Scenarios

| Metric | Actual Cash Value (ACV) Scenario | Replacement Cost Value (RCV) Scenario |

|---|---|---|

| New Roof Cost | $25,000 | $25,000 |

| Depreciation | $15,000 (Subtracted) | $15,000 (Recoverable) |

| Deductible | $2,000 | $2,000 |

| Initial Payout | $8,000 ($25k – $15k – $2k) | $8,000 ($25k – $15k – $2k) |

| Final Payout | $0 | $15,000 (after repairs) |

| Total Insurer Payout | $8,000 | $23,000 |

| Your Out-of-Pocket Cost | $17,000 | $2,000 |

The numbers don’t lie. The difference between these two policy types is a staggering $15,000 that either comes out of the insurer’s pocket or yours.

You need to pull out your policy declarations page right now and confirm if you have ACV or RCV coverage for your roof. If it’s ACV, you need to prepare for a fight. If it’s RCV, you have to be ready to hold your insurer’s feet to the fire to get every last penny of that recoverable depreciation. Gaining a deeper understanding of why the difference between ACV and RCV matters so much is the first, most critical step in winning this fight.

How to Fight Back Against a Lowball Offer

Let’s be blunt: that laughably low settlement offer from your insurance company isn’t an accident. It’s an opening bid. It’s a calculated move in a negotiation you didn’t ask for, and carriers like State Farm and Allstate are banking on you being too overwhelmed to push back.

This is your game plan. It starts the second the storm passes. If you want to force them to pay what you’re actually owed, you have to build an airtight case from the ground up, starting now. Don’t wait for their adjuster to show up and tell you what they think your damage is worth.

Step 1: Document Everything Immediately

Before you even think about dialing your insurer’s 800-number, your one and only job is to create a complete record of the damage. This evidence is the only weapon that works against an adjuster who is paid to minimize your claim.

Here’s your checklist. Don’t skip a thing.

- Take Hundreds of Photos: Seriously, you can’t have too many. Get wide shots of the whole roof from every angle you can safely manage. Then get right up on the details—dented or creased shingles, lifted tabs, cracked tiles, and beat-up flashing.

- Shoot Timestamped Video: Walk your property with your phone recording. Narrate what you’re seeing, state the date and time, and describe the storm that just came through. A narrated video provides context that photos alone can’t. It’s a powerful, real-time log.

- Start a Claim Journal: Grab a notebook or open a new document. Log every single phone call, email, and interaction you have with the insurance company. Write down the date, time, who you spoke to, their title, and a summary of the conversation. This journal is your defense against delays and contradictions later on.

This initial evidence is how you prove the damage was sudden and caused by a covered storm, shutting down the carrier’s go-to excuse of “pre-existing wear and tear.”

Step 2: Get Your Own Independent Estimates

I’m going to say this once because it’s the most important rule in this entire process: NEVER accept the estimate from your insurance company’s adjuster as the final word. It’s not a fair assessment; it’s a document engineered to justify paying you as little as possible.

They use outdated pricing software and conveniently “forget” to include critical line items like bringing your roof up to code, replacing all the flashing, or ensuring proper ventilation. It happens every single day.

Your insurance company’s adjuster works for them, not you. Their primary job is to protect the company’s bottom line. To fight their lowball offer, you need estimates from professionals who work for you.

You need to get at least two, preferably three, detailed estimates from trusted, local roofing contractors. Do not use the “preferred” contractor your insurer recommends. They have a built-in conflict of interest—they keep their estimates low to stay in the insurance company’s good graces and keep the referrals coming.

A real, independent estimate will break down every single cost, including things like:

- Labor and Materials: The specific type and quantity of shingles, underlayment, and everything in between.

- Code Upgrades: The work required to bring your roof up to current local building codes, which is often mandatory and covered under most policies.

- Permit Fees: The cost for all necessary municipal permits.

- Debris Removal: The labor and disposal fees for tearing off and hauling away your old, damaged roof.

These quotes aren’t just for your own information; they are your primary ammunition. When you submit these to the insurer, you’re not just asking for more money—you are challenging their lowball number with hard data from the real world. This forces them to justify why their numbers are so far off from what it actually costs to do the job right.

For any homeowner or business owner reeling from a storm, knowing how to properly manage your property damage claim from day one can make all the difference between a small check and a full recovery.

When You Need a Public Adjuster in Your Corner

Trying to fight your insurance company alone is like walking into a courtroom to argue against a team of seasoned lawyers. They know the rules, they wrote the playbook, and their only goal is to protect their bottom line.

Their adjusters, their managers, and their internal processes are all built for one purpose: to minimize claim payouts. This is a game they play every single day.

When your roof claim is delayed, underpaid, or flat-out denied, it’s almost never an honest mistake. It’s a calculated business decision. That’s the moment you need to stop playing their game and bring in a professional who fights exclusively for you.

Recognizing the Red Flags to Call for Help

You don’t have to wait for the official denial letter to arrive to know you’re in a fight. The second your insurer starts using stall tactics or making excuses, it’s time to get help. These moves are clear signals they’re building a case against you, not for you.

Here are the undeniable red flags that mean you need a public adjuster, effective immediately:

- The Lowball Offer: Their adjuster hands you an estimate that’s a fraction of what your trusted local roofer quoted. This isn’t a simple disagreement—it’s a deliberate attempt to undervalue your loss.

- Going Silent: You leave voicemails and send emails, but days turn into weeks with no real answers. This is a classic “delay and deny” tactic designed to frustrate you into giving up or accepting a bad offer.

- Dismissing Real Damage: The carrier’s adjuster calls obvious hail impacts or wind-lifted shingles “cosmetic damage,” “normal wear and tear,” or a “pre-existing issue.” This is their go-to excuse for denying a full roof replacement.

- Blaming Your Contractor: They try to discredit your roofer by claiming their estimate is “inflated” or includes “work that isn’t necessary.” It’s a strategy to create conflict and make you doubt the people trying to help you.

- The Never-Ending Paperwork Game: They keep demanding more photos, more forms, and more records, burying you in a mountain of bureaucracy to stall the claim indefinitely.

If you recognize any of these tactics, your insurance company has shown its hand. They are not on your side. They are protecting their profits at your expense.

The Power of a Local Public Adjuster

A public adjuster is a state-licensed claims professional who works only for you, the policyholder. Unlike the insurance company’s staff adjuster (who works for them) or an independent adjuster (who is hired by them), a public adjuster’s loyalty is never divided. Our one and only job is to document your loss, negotiate with the insurer, and settle your claim for the absolute maximum you’re owed under your policy.

You can get a deeper dive into the role by reading our guide on what a public adjuster is and how they can help you.

Having a local expert is a massive advantage. A public adjuster in North Carolina or Virginia isn’t just an insurance pro; they’re an expert on the unique challenges in our area.

A local public adjuster knows the specific building codes in your town, the common games insurers play in our states, and the actual cost of materials and labor right now, right here. That local knowledge is a weapon against an out-of-state carrier trying to use outdated national pricing data.

We level the playing field because we speak their language. A public adjuster dissects your policy, builds a claim using the same software the insurers use (but with correct, real-world data), and forces the carrier to pay by citing the exact policy language and state regulations they are violating.

When you’re asking, “how do I make my insurance cover my roof replacement,” a public adjuster is the one with the right answer and the power to make them listen.

Answering Your Critical Roof Claim Questions

When you’re going head-to-head with your insurance company over a damaged roof, it’s easy to feel overwhelmed and alone. They rely on that confusion. This section cuts right through their tactics to give you straight answers to the most urgent questions we hear from homeowners and business owners when their insurer refuses to do the right thing.

Can an Insurer Refuse to Renew My Policy After a Roof Claim?

Yes, and it’s a classic intimidation tactic. While it’s usually illegal for an insurance company to cancel your policy mid-term just for filing a legitimate claim for storm damage, they absolutely can opt for non-renewal when your policy is up. They see a major claim, especially for something as expensive as a roof, and suddenly decide your property is too “high-risk.”

It’s a dirty, but perfectly legal, trick. You pay them premiums for years, but the moment a storm forces them to actually hold up their end of the deal, they punish you for it by showing you the door. This is just one more reason to fight for every single dollar you are owed on your current claim.

What If My Neighbors Got Their Roofs Replaced But Mine Was Denied?

This is incredibly common, and it’s one of the most powerful pieces of evidence you can have. Think about it: if a hailstorm was bad enough to destroy multiple roofs on your street, it makes absolutely no sense that your home was somehow magically protected.

An adjuster who denies your claim in this situation is throwing up a massive red flag. It tells you they aren’t looking at your actual damage; they’re following a script designed to deny claims and save the company money. If this happens, you need to act immediately:

- Document Everything: Get photos of your neighbors’ new roofs being installed.

- Talk to Their Contractor: The roofer who handled the other claims can be an incredible source of information, maybe even providing a report on the storm’s severity in your specific area.

- Put the Insurer on the Spot: A formal letter showing that all your neighbors’ claims for the exact same storm were approved puts immense pressure on your carrier to explain why you’re the exception.

Do I Have to Accept the Contractor My Insurance Company Recommends?

Absolutely not. In fact, you should be extremely suspicious of their “preferred” contractor list. It might sound like they’re trying to be helpful, but it’s a massive conflict of interest. These contractors get a steady flow of work from the insurance company, so they have a big incentive to write low estimates and keep the insurer happy—not you.

You have the absolute right to choose your own independent, trusted, local contractor. Your roofer works for you, not the insurance company.

A truly independent contractor writes an estimate based on what it actually costs to fix your roof correctly. That includes accounting for local building codes and using quality materials—details the insurer’s preferred guy might conveniently ignore.

What Happens If My Roof is Old?

Get ready for a fight, because insurers weaponize your roof’s age against you. If your roof is more than 15 or 20 years old, their first move will be to claim the damage is just normal wear and tear, not from the storm. They’ll also likely try to pay you only the Actual Cash Value (ACV)—the depreciated value of your old roof—leaving you on the hook for the difference.

But a valid storm claim is a valid storm claim, period. If a covered event like hail or a windstorm wrecked your roof, they owe for that damage based on the policy you paid for. Don’t let them bully you out of a legitimate claim just because your roof wasn’t put on last year. This is where a public adjuster becomes essential—to force them to honor the contract you have with them.

Why is the Insurance Company Calling the Damage ‘Cosmetic’?

“Cosmetic damage” is a favorite loophole for insurance companies, especially with metal or tile roofs. They’ll admit a hailstorm left hundreds of dents all over your metal roof, but then argue that because it’s not actively leaking right now, the damage isn’t “functional.” Based on that, they’ll claim they don’t have to pay for a replacement.

This is a dishonest game. Serious cosmetic damage tanks your property value, can void your manufacturer’s warranty, and often leads to premature rust and failure. You didn’t pay premiums for a dented, compromised roof. You have to fight this ridiculous classification and demand they pay for the loss in value and integrity to your property.

When your insurance company’s excuses don’t make sense, you need an advocate who knows their entire playbook. The team at For The Public Adjusters, Inc. fights exclusively for policyholders in North Carolina and Virginia to get the full and fair settlement you are owed. If you’re facing a denied, delayed, or underpaid roof claim, contact us for a no-cost claim review at https://forthepublicadjusters.com.