You searched what is Itel. Fair question. But if you're in the middle of a property claim, that search may be pointing you toward the wrong problem.

Generally, the term 'itel' refers to the phone brand. Homeowners and business owners in a claim dispute often run into a very different ITEL. That one can show up in a roof, siding, or flooring claim and suddenly become the excuse for a low-ball payment, a mismatch repair, or a denial of full replacement. That's where things get expensive.

The confusion is understandable; existing content rarely clarifies the difference between itel Mobile, a Transsion Holdings subsidiary ranking as a top handset brand in emerging markets, and specialized industry services like ITEL Laboratories that operate in entirely different sectors like insurance claims, as noted by CB Insights on itel Mobile.

If your insurer is waving around an ITEL report, stop treating it like gospel. It's evidence. It can be challenged. And in the wrong hands, it's a shortcut to paying you less than your policy owes.

Table of Contents

- What Is Itel and Why Are You Here

- First Things First The Itel Smartphone Brand

- The ITEL Report That Slashes Your Insurance Payout

- How Insurers Weaponize ITEL Reports Against You

- Your Claim Dispute Plan for a Bad ITEL Valuation

- Denied or Low-Balled Because of ITEL Get Claim Help Now

What Is Itel and Why Are You Here

There are two answers to what is Itel. One is harmless. The other can cost you real money.

The first is itel Mobile, a consumer electronics brand. The second is ITEL in the insurance world, the name many policyholders encounter when a carrier wants to justify a cheaper material, a partial repair, or a lower payout on a dwelling or commercial property claim.

That difference matters because claim disputes don't turn on brand names. They turn on bargaining power, documentation, and policy language. If your adjuster says, "ITEL found a match," what they're really saying is, "We're relying on a third-party report to limit what we'll pay."

Practical rule: If an insurance company uses any outside report to reduce scope or price, ask for the full report, the sample basis, and the exact policy language they're relying on.

A lot of property owners miss the danger because the word sounds technical and neutral. Neutral isn't the same as correct. And correct isn't the same as covered. A report can still be incomplete, outdated, disconnected from what is installed, or irrelevant to your policy's matching and replacement obligations.

Why this search matters in a claim

If you're dealing with storm damage, water damage, or a business property loss, ITEL usually shows up after the easy part is over. The carrier has inspected. The estimate is short. The adjuster starts talking about "comparable" materials. That's when the fight begins.

Here's the simple version:

- If you're shopping phones: Itel is a handset brand.

- If you're disputing a property claim: ITEL may be the report being used against you.

- If the insurer cites it to limit payment: you need to challenge the conclusion, not just complain about the number.

The policyholder who wins this fight is usually the one who stops arguing in general terms and starts attacking the weak points in the report itself.

First Things First The Itel Smartphone Brand

If you came here asking what is Itel in the consumer tech sense, here's the straight answer.

Itel Mobile is a Hong Kong-based Chinese smartphone manufacturer under Transsion Holdings. It was established in 2007 and became one of the top 3 mobile brands in Africa by 2016 after selling 50 million devices, according to The Sun's profile of Itel Mobile. By 2018, it was recognized as the 16th most-admired brand in Africa, which shows the extent of its penetration into emerging markets in a short period.

What the brand is known for

Itel built its name by selling affordable phones aimed at buyers who care about price, battery life, and practical daily use more than premium specs. Its strategy has focused on markets where consumers need durable devices, long battery performance, and dependable connectivity at a lower cost.

That identity is completely separate from the insurance-related ITEL that shows up in property claims.

Why that distinction matters

People often search the word once and assume they're looking at one company. They aren't. The phone brand belongs in a consumer electronics conversation. The insurance version belongs in a claim dispute conversation.

If your issue involves a roof, siding, flooring, or interior finishes after a covered loss, the smartphone brand isn't your problem. The problem is whether an insurance company is using an ITEL-related analysis to pretend a non-matching or lower-grade substitute satisfies your policy.

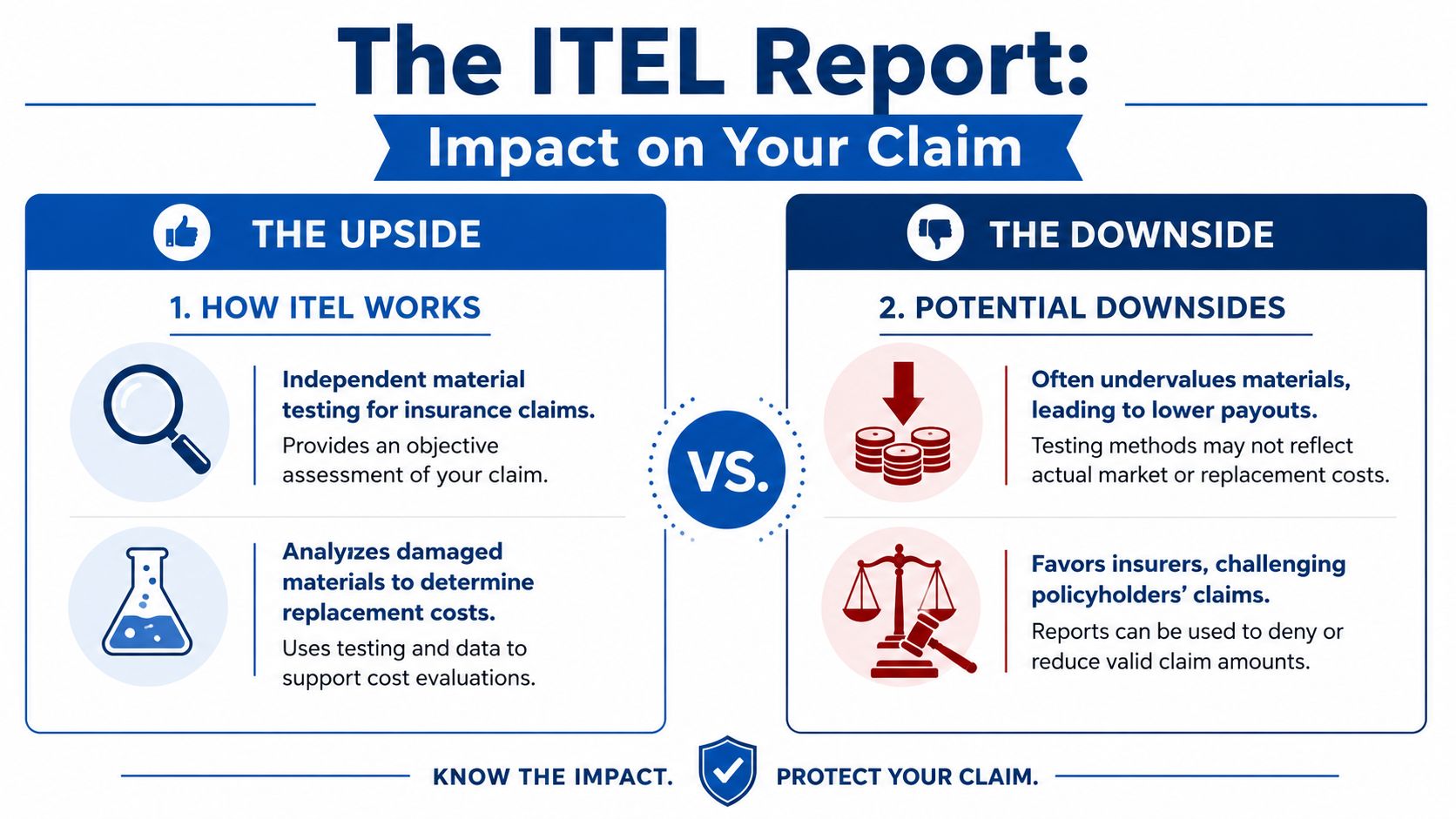

The ITEL Report That Slashes Your Insurance Payout

The version of ITEL that matters in a property claim is the report used to analyze damaged materials and identify a supposed replacement. Carriers use it in roofing, siding, and flooring disputes because it gives them a paper trail.

What insurers say ITEL does

The insurer's pitch is simple. They say ITEL helps determine a replacement material of like kind and quality. On paper, that sounds reasonable. In practice, policyholders often get handed a report that supports a cheaper path: patch the damaged area, install something "close enough," and move on.

That "close enough" language is where carriers save money and property owners get stuck with the consequences.

A low valuation problem usually ties into a bigger payment problem. If you need a quick breakdown of how carriers try to reduce settlement amounts through depreciation and pricing tactics, read this explanation of insurance actual cash value. Many bad ITEL outcomes end up feeding that same underpayment machine.

Where the fight starts

A report is only as good as the assumptions behind it. If the sample is wrong, if the product is discontinued, if the substitute won't match, or if local availability is shaky, then the report can become a weak foundation for a bad claim decision.

Homeowners hear phrases like these all the time:

- Commercially similar: Not the same thing as a true match.

- Repairable area only: Convenient for the insurer, ugly for the property owner.

- Available alternative: Often detached from visual consistency or policy obligations.

- Comparable product: A favorite phrase when the original material can't be replaced exactly.

A report that helps the carrier justify a partial fix isn't the end of the claim. It's the start of your rebuttal.

Later in the process, insurers may act as though the report settles the issue. It doesn't. Your policy controls. The physical condition of the building controls. And if a partial repair leaves a mismatch or lowers the property's appearance, function, or marketability, you have grounds to dispute the carrier's position.

A short video can help clarify how these valuation reports affect real property losses and why policyholders push back:

How Insurers Weaponize ITEL Reports Against You

Insurers don't need a report to be perfect. They just need it to sound technical enough that a frustrated policyholder gives up.

The roof claim trap

A storm damages one slope of your roof. The original shingle is older and no longer readily available in a true visual match. Instead of paying for a full roof section or a broader replacement where matching is the primary issue, the carrier leans on an ITEL-style report and says a "similar" shingle exists.

Then the adjuster offers payment for the damaged area only.

That's how you end up with one roof that looks like two different roofs. One side weathers differently. One side reflects light differently. The repaired section may stand out from the street, from the driveway, and definitely when you try to sell the house.

If you're already getting stonewalled by the carrier's field adjuster or desk adjuster, this guide on dealing with an insurance adjuster will help you tighten up your response and stop making the common concessions insurers count on.

The flooring version is just as bad

Flooring disputes can get even uglier because continuity matters room to room. The carrier says only one area was affected. They use a pricing or matching report to argue they can replace that section only. The result is a visible transition, uneven wear pattern, and a repair that may technically fill space but doesn't restore the property to a consistent condition.

That gap between what sounds efficient and what restores the property is the problem. As one source puts it, the strategic disconnect is stark: while the Itel phone brand innovates with itelOS to improve user experience on low-spec devices, the ITEL analysis service is often perceived as a tool that degrades the homeowner's experience by justifying subpar repairs and creating claim disputes, as noted in Wikipedia's Itel Mobile entry.

The carrier's estimate is often written to defend a payment decision first and solve your property problem second.

Here's the pattern I see again and again with major insurers and smaller carriers alike:

| Claim stage | What the insurer says | What it often means |

|---|---|---|

| Material testing | "We're verifying a match" | They're looking for a basis to limit scope |

| Estimate revision | "Only part of the area is affected" | They want to avoid full replacement |

| Settlement offer | "This is all the policy owes" | They're betting you won't challenge it |

You don't beat this by arguing emotionally. You beat it by proving the substitute doesn't restore uniformity, doesn't satisfy policy language, or doesn't reflect the actual installed material.

Your Claim Dispute Plan for a Bad ITEL Valuation

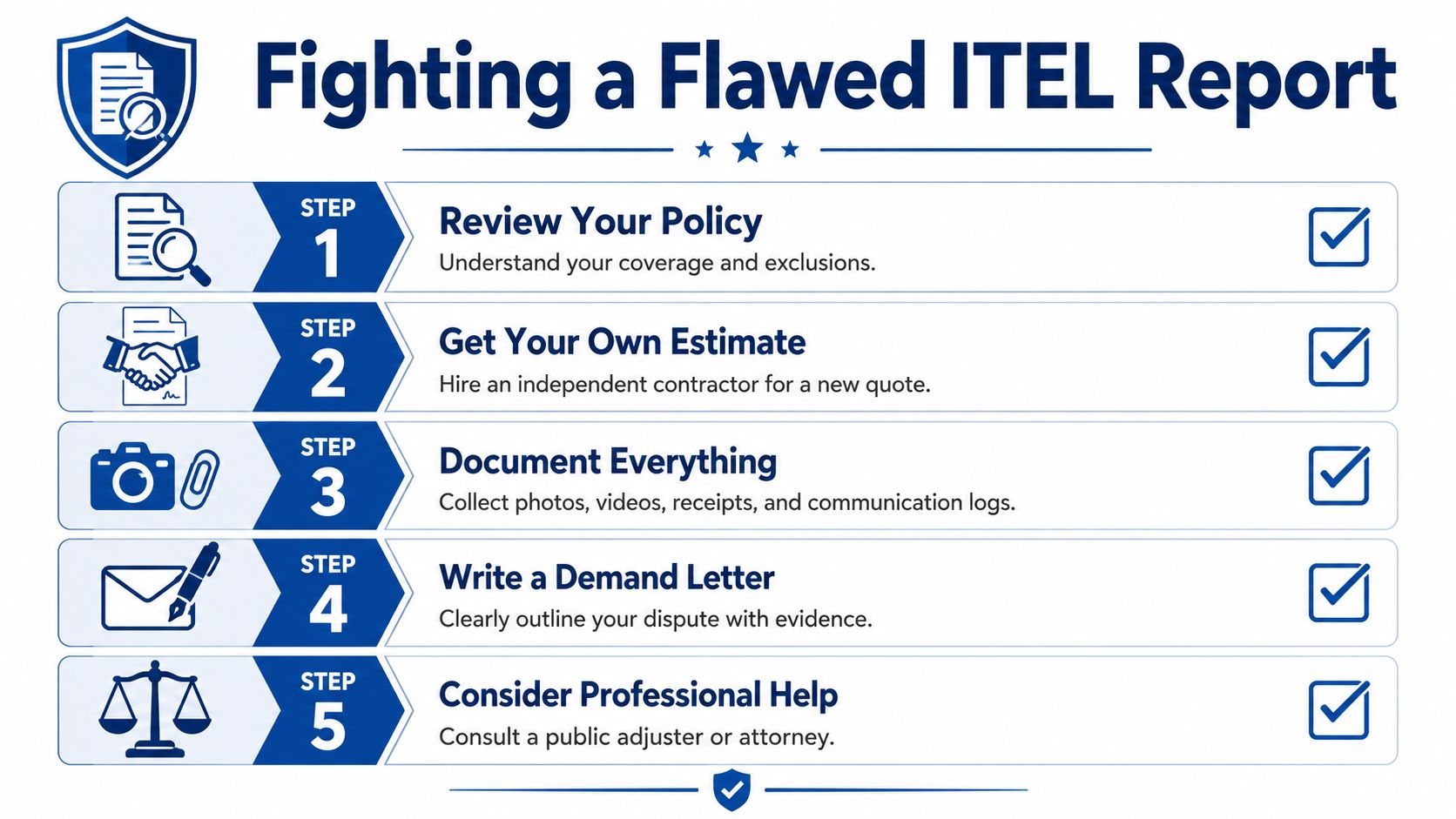

You don't need to accept a bad ITEL-based decision just because it arrived on official-looking paper. You need a cleaner record, stronger evidence, and pressure in the right places.

What to demand from the adjuster

Start with documents. Not summaries. Not a phone call recap. The actual material.

- Ask for the full report. You want the complete ITEL valuation or matching report, not the carrier's interpretation of it.

- Request the basis for the sample. Find out what was submitted, who submitted it, and whether it came from the damaged material at your property.

- Pull the policy language. Matching, uniform appearance, replacement cost terms, exclusions, limitations, and endorsements all matter.

- Get an independent contractor assessment. A roofer, flooring contractor, or siding professional can often identify real-world problems that a lab-style report glosses over.

- Photograph the mismatch issue clearly. Wide shots, close-ups, transitions, elevations, and lighting differences all help.

How to build pressure that works

You need a written dispute, not a string of irritated calls. Put the carrier on notice that the report doesn't settle the loss.

Use a demand letter that does three things:

- Challenge the substitute material: explain why it isn't a true match in appearance, composition, size, texture, or installation result.

- Tie the dispute to the policy: force the insurer to identify exactly where the policy permits the lower scope.

- Attach outside support: contractor letters, photos, estimates, and product availability details matter.

A lot of property claim strategy overlaps with other valuation fights. If you want to see how a structured challenge can help a policyholder maximize your total loss claim, that resource shows the same basic principle. Insurers count on quick acceptance. Disputes get stronger when you document market reality and force a line-by-line review.

Action point: Never argue that the offer feels unfair. Argue that the scope is incomplete, the match is defective, and the carrier's interpretation of the policy is wrong.

I've seen these disputes turn when a policyholder stops debating the adjuster and starts building a file. A contractor says the roof can't be reasonably matched. A flooring expert confirms the replacement line differs in finish and dimensions. The carrier realizes the paper defense won't hold up under scrutiny. That's when positions change.

Denied or Low-Balled Because of ITEL Get Claim Help Now

If you came here asking what is Itel, you now know the answer depends on why you're asking. One Itel is a phone brand. The other can become a serious problem inside a homeowner or business property claim.

When an insurer relies on ITEL to justify a patch, mismatch, or stripped-down payment, don't assume the report is final. It isn't. It's one piece of the insurer's file, and plenty of low-ball offers hide behind paperwork that looks more authoritative than it really is.

If your loss involves roofing, outside contractor support can help expose scope and matching issues early. For roof-specific documentation and repair-side guidance, review ZEV Roofing & Construction's claim services. If you're still deciding whether you need your own advocate, learn what a public adjuster is and why policyholders bring one in when the carrier stops playing fair.

One review says it plainly:

"For The Public Adjusters made the entire process stress-free. After my insurance company used a report to say they only had to replace half my floor, FTPA stepped in. They fought for me and got the whole floor replaced with a perfect match. I can't recommend them enough!" – Jane D., Raleigh, NC

Have your water damage claim questions answered at NO COST. Call 919-400-6440 to speak with a licensed Public Insurance Adjuster or Contact Us here with questions. WE Work For YOU… NOT Your Insurance Company!

If your homeowner or commercial property claim has been delayed, underpaid, or denied because the insurance company is hiding behind an ITEL report, For The Public Adjusters, Inc. can step in and fight for the full scope of damage your policy covers. They represent policyholders in North Carolina, not insurance companies, and they know how to challenge bad estimates, weak matching decisions, and settlement offers that don't come close to restoring the property properly.