The storm is over. The fire trucks are gone. Your contractor tells you the damage is serious but repairable, and you finally expect your insurance company to do what you paid it to do.

Then the letter arrives.

The check is nowhere near enough. Not enough to replace the roof. Not enough to rebuild the damaged rooms. Not enough to put your business equipment back in service. The carrier calls it insurance actual cash value. You call it what it feels like: a low-ball.

That shock is common for homeowners and business owners in North Carolina and Virginia. The insurer acts like the number is objective and final. It usually isn't. ACV is one of the most common ways carriers reduce what they pay, especially after fire, water, wind, hail, and hurricane losses. If you're staring at a settlement that doesn't come close to real repair costs, the fight isn't over. It's just started.

Table of Contents

- The Low-Ball Letter Your Insurance Actual Cash Value Shock

- What Is ACV and Why Insurers Use It to Undervalue Your Claim

- The Deceptive Math How Insurers Calculate ACV Depreciation

- ACV vs Replacement Cost The Policy Trap You Must Understand

- Real-World Battles ACV in NC & VA Homeowner Claims

- Your Fight Plan How to Dispute a Low ACV Settlement

- When to Call for Reinforcements Get Help From For The Public Adjusters

The Low-Ball Letter Your Insurance Actual Cash Value Shock

A lot of policyholders think the worst part is the loss itself. It isn't. The worst part is often opening the insurer's estimate and realizing the company has valued your damaged property as if it were half-used junk, even when it was fully functional, maintained, and still serving its purpose the day before the loss.

That first ACV payment often feels like a betrayal because it is wrapped in technical language. The carrier points to depreciation, age, condition, useful life, and valuation method. The paperwork looks polished. The number looks official. The result is the same. You get pushed into a financial hole while the insurer protects its bottom line.

For homeowners, this usually shows up after roof, interior water, smoke, or storm claims. For business owners, it hits building components, contents, machinery, tenant improvements, and specialty items that the desk adjuster barely understands. The insurer knows policyholders are stressed, busy, and under pressure to move on quickly. That's why low ACV offers are so effective.

Practical rule: If the first payment doesn't match the real-world cost to repair or replace damaged property, treat the offer as a position in a negotiation, not the final word.

The mistake people make is assuming the insurance company already did a fair evaluation. Often, it did an insurer-friendly evaluation. Those aren't the same thing.

Carriers also benefit from confusion. Many policyholders don't realize the number on the first check may reflect a heavily depreciated value rather than what today's materials and labor will cost in reality. Others assume their adjuster inspected everything carefully when the estimate was built from shortcuts, templates, or broad assumptions.

If you've received a low ACV payment, don't spend weeks arguing in circles over feelings. Shift the fight to proof, valuation method, depreciation inputs, and policy language. That's where claims get turned around.

What Is ACV and Why Insurers Use It to Undervalue Your Claim

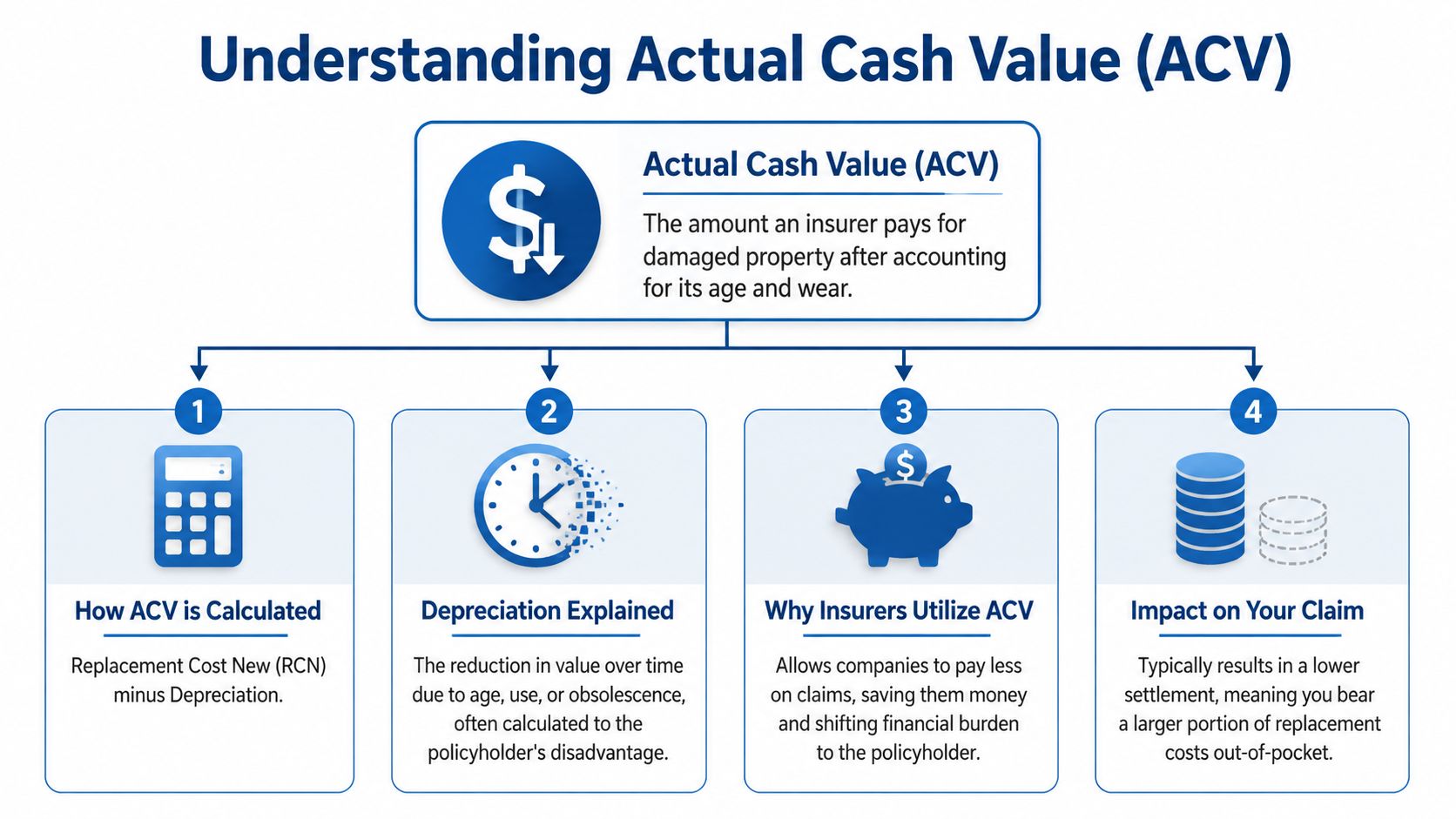

Actual cash value sounds neutral. It isn't neutral in practice. It's the valuation method carriers use to reduce payouts by subtracting depreciation from replacement cost, and that depreciation number is where the underpayment starts.

North Carolina's Department of Insurance says ACV is the amount needed to fix a home, minus the decrease in value because of age or use, and contrasts it with replacement cost value, which is based on today's building-supply prices or the current cost of a like item. It also notes that insurers often pay ACV first and only reimburse the remaining amount after repair or replacement is completed and receipts are submitted, as explained in the North Carolina Department of Insurance guide on ACV vs. RCV.

ACV is simple on paper and slippery in practice

In plain English, insurance actual cash value usually means replacement cost minus depreciation. But that still doesn't make it straightforward. Some authorities also recognize that insurers may use fair market value or the broad evidence rule depending on the policy and jurisdiction, which is why ACV disputes often become technical fights over method, not just math, as noted in this actual cash value glossary explanation.

That flexibility helps carriers. If the policyholder sees ACV as a clear formula, the insurer may treat it as a moving target. One item gets valued by age and useful life. Another gets pushed toward market value. Another gets reduced because the company claims obsolescence. The result is lower money out.

Why insurers lean on depreciation

The carrier's favorite word in an ACV claim is depreciation because it gives the company room to make judgment calls that usually run one way. Against you.

An adjuster can look at a roof, cabinet set, hardwood floor, HVAC component, or piece of business property and assign wear, age, or functional decline in a way that sounds technical but isn't tied to your actual pre-loss condition. That's how a maintained property ends up valued like a neglected one.

Here's where policyholders need to get aggressive:

- Challenge age assumptions: Insurers often work from estimated ages, not verified installation dates.

- Challenge condition assumptions: A well-maintained item should not be treated like one that was at the end of its useful life.

- Challenge blanket depreciation: Damaged property must be evaluated item by item when the facts support it.

- Challenge vague labels: “Obsolete,” “aged,” and “worn” should be backed by specifics, not adjuster shorthand.

The fight over ACV usually isn't about whether depreciation exists. It's about whether the insurer inflated it.

If you're dealing with State Farm, Allstate, or any other large carrier, assume the estimate was built to control payout first. Read it that way. Review every line that reduces value. That's where the money is being lost.

The Deceptive Math How Insurers Calculate ACV Depreciation

When a carrier says it “applied depreciation,” that can sound like a clean accounting exercise. It usually isn't. It's a chain of assumptions about useful life, age, wear, maintenance, and obsolescence, and every assumption can push the settlement lower.

Depreciation is where the fight lives

Insurers commonly estimate depreciation from useful life expectancy, age, wear and tear, and market or obsolescence factors. One industry example values a laptop at 60% of replacement cost when it is two years into a five-year useful life, and another example notes that a heavily used machine of the same age will be depreciated more than lightly used equipment, as explained in this breakdown of ACV depreciation inputs.

That matters because these are not fixed truths. They are inputs. If the adjuster uses the wrong installation date, ignores maintenance, misstates use, or assumes a short useful life, the ACV drops. Fast.

For dwelling and business owner claims, the pressure points are usually obvious once you know where to look:

- Roofing and exterior items: The carrier may focus on age while ignoring maintenance and remaining service life.

- Interior finishes: Cabinets, flooring, trim, and paint often get grouped into broad categories with little attention to actual condition.

- Business contents and equipment: The insurer may treat specialized property like generic property.

- Obsolescence claims: Adjusters sometimes use “obsolete” as a shortcut to deeper depreciation without proving why.

A useful starting point is to compare the depreciation line with the replacement line. If replacement pricing looks close to reality but ACV is far too low, depreciation is likely the lever the insurer pulled hardest. If you want a deeper look at how that process works in property claims, review this explanation of depreciation on insurance claims.

Labor depreciation is a major pressure point

Some of the most serious ACV disputes involve whether depreciation can be applied to labor, not just materials. Policyholders usually assume labor shouldn't lose value the same way a physical item does. Carriers have pushed the opposite argument.

A North Carolina case discussed in 2020 involved an insurer's ACV estimate of $933,429.37 after subtracting $79,658.39 in depreciation, which was about 8%, from a $1,013,087.76 replacement cost estimate. The same litigation summary notes that the “actual cash value” issue is still relatively young in insurance law, and that some courts have confirmed depreciation can even apply to labor, as discussed in this North Carolina ACV case analysis.

That should get your attention. When insurers depreciate labor, the payment gap can widen even more, especially on large structural losses.

This short video gives a useful overview of how depreciation disputes show up in real claim handling.

The key point is simple. Depreciation is not just arithmetic. It's an opinion dressed up as arithmetic. That means it can be challenged with better evidence, better scope, and better valuation work.

ACV vs Replacement Cost The Policy Trap You Must Understand

Most policyholders don't realize how dangerous the difference is until after the loss. ACV coverage pays on a depreciated basis. Replacement cost coverage is built around today's cost to repair or replace with like kind and quality, subject to the policy terms. That gap can decide whether you recover or stall out.

The trap is that many people think replacement cost means the insurer will write a full check once damage is confirmed. That's not how it usually works.

What the payout difference looks like

Here is a simple claim comparison using a roof loss example. This table is illustrative in structure, not a statement of depreciation percentages or guaranteed outcomes.

| Metric | Actual Cash Value (ACV) Policy | Replacement Cost Value (RCV) Policy |

|---|---|---|

| Loss example | $50,000 roof damage | $50,000 roof damage |

| Initial valuation basis | Replacement cost minus depreciation | Often ACV first, with remaining amount potentially recoverable later |

| Up-front payment impact | Lower initial payment | Higher total potential recovery if policy conditions are met |

| Out-of-pocket pressure | Usually heavier | Often reduced, but cash flow can still be a problem |

| Main dispute | Whether depreciation was inflated | Whether holdback is being released properly and full scope is recognized |

North Carolina regulators make the distinction plainly. ACV is the amount needed to fix the home minus the decrease in value because of age or use, while RCV is based on today's cost. They also note insurers often first pay ACV and then reimburse the remaining depreciation only after repair or replacement is completed and receipts are submitted, as described in the North Carolina DOI explanation of valuation methods.

That “pay now, maybe pay later” structure creates a serious problem for families and businesses without ready cash. If the insurer holds back a large portion of the money, you may have to finance repairs yourself before the carrier releases what the policy may owe.

The holdback problem

Recoverable depreciation sounds harmless. It isn't. It turns your claim into a reimbursement process.

That means you may need to sign contracts, order materials, pay deposits, and keep work moving before the insurer releases the full amount. If the scope is large, that can be brutal. The policy may say replacement cost is available, but the carrier's payment process still leaves you funding the gap up front.

If your policy includes replacement cost, don't assume the insurer's first check reflects the full value of the claim. It often doesn't.

For policyholders trying to understand that difference in more detail, this overview of the difference between actual cash value and replacement cost is worth reviewing.

A related lesson comes from outside property claims. Specialized coverage often looks straightforward until valuation and policy conditions start limiting recovery. That same pattern shows up in niche risk policies too, including resources like the Dronedesk guide to drone insurance, where valuation terms and exclusions change what gets paid after a loss. The principle is the same. If you don't understand how the policy values property, the carrier has the advantage.

Real-World Battles ACV in NC & VA Homeowner Claims

The insurance company doesn't need to deny a claim outright to cause damage. It only needs to underpay badly enough that you can't finish repairs, replace contents, or reopen your business on time.

That's what ACV fights look like in practice. The carrier accepts the loss, issues a check, and acts like the matter is mostly resolved. Meanwhile, the homeowner can't hire the right contractor, and the business owner is left juggling cleanup, operations, and a settlement that doesn't match the property that was damaged.

What these disputes look like on the ground

A common homeowner scenario in North Carolina starts with wind, hail, or water damage. The adjuster writes a quick estimate, applies steep depreciation to older components, leaves out related repairs, and presents the ACV payment as reasonable. It isn't denial by letter. It's denial by math.

Commercial claims can get even uglier. A business owner may have damaged interiors, custom finishes, stock, tenant improvements, and equipment that don't fit neatly into a standard pricing template. If the insurer treats specialty property like ordinary property, ACV gets crushed.

That is usually when policyholders realize the carrier's adjuster is not there to advocate for them.

Customer feedback matters because it shows how these disputes feel from the policyholder side. Reviews of public adjusting firms often mention the same pattern. The insurer undervalued the loss, communication dragged, and the claim didn't move until someone pushed back with documentation and negotiation pressure.

A low ACV offer often tells you less about your property and more about how aggressively the insurer is cutting the claim.

Why catastrophe claims get worse

ACV disputes become more severe after hurricanes and widespread storm events. Rising construction costs and repeated severe weather events in states like North Carolina widen the gap between depreciated value and actual replacement expense, making underpayment more common in fire, wind, and hurricane claims, as discussed in this North Carolina-focused ACV and replacement cost article.

When carriers are handling a large volume of claims at once, speed often replaces precision. Broad assumptions get used across many files. Depreciation gets applied in patterns. Local market pricing gets missed. Scope details get shaved down.

That creates the same outcome across towns and counties. The insurer says the settlement is technically correct. The policyholder looks at contractor pricing and knows it isn't enough.

Virginia policyholders run into the same kind of fight after major wind and water losses. The names of the carriers may change, but the playbook doesn't. Tight estimates. aggressive depreciation. delayed movement unless someone forces the issue.

Your Fight Plan How to Dispute a Low ACV Settlement

You don't beat a low ACV offer by telling the insurer it feels unfair. You beat it by attacking the assumptions that created the number.

Start with the carrier's math

Your first move is simple. Demand the full basis for the ACV calculation.

Ask for the estimate, the depreciation worksheet, the stated age of each major item, the useful-life assumptions, the condition assumptions, and any notes supporting obsolescence or labor depreciation. Insurers estimate depreciation from useful life expectancy, age, and wear, and a heavily used item can be depreciated more than a lightly used item of the same age. That is exactly why policyholders disputing a low ACV should request the carrier's depreciation worksheet and the basis for those assumptions, as explained in this guide to how insurers estimate ACV depreciation.

Don't ask casually. Ask in writing.

Use direct questions:

- What age did you assign to the roof, flooring, cabinets, equipment, or contents item?

- What useful life did you assign?

- What facts did you rely on for condition?

- Did you depreciate labor? If yes, identify each line where that occurred.

- What valuation method did you apply to each category of property?

If the adjuster won't answer clearly, that's a warning sign. The insurer may be relying on broad assumptions it doesn't want examined.

Build a file the insurer can't ignore

Your best evidence is specific evidence. Not general complaints.

Gather what supports the pre-loss condition and current replacement need:

- Photos and videos: Pull pre-loss images from your phone, listing photos, inspection files, maintenance logs, and social media if necessary.

- Receipts and invoices: Installation records, remodel invoices, service calls, and prior contractor work can help prove age and upkeep.

- Independent contractor estimates: Get local scope and pricing from people who perform the work in your market.

- Product details: Brand, model, grade, finish, and quality level matter. Generic substitutions help the insurer, not you.

- Maintenance proof: Cleaning, servicing, repairs, and upkeep can directly undermine excessive depreciation.

Then compare your evidence against the insurer's estimate line by line. Not globally. Line by line.

Claim tactic: The more specific your evidence gets, the harder it is for the carrier to hide behind generic depreciation.

Your dispute letter should be structured, not emotional. Identify the disputed items, state the insurer's assumption, present your contrary evidence, and attach supporting documents. If the scope is wrong, say why. If pricing is wrong, show the local estimate. If depreciation is overstated, point to condition, maintenance, and actual use.

A few more hard rules help:

- Don't cash-flow the insurer's mistake: If the payment is too low, preserve your objection instead of acting like the amount is acceptable.

- Don't rely on phone calls: Important disputes belong in writing.

- Don't let the claim shrink over time: Carriers benefit when policyholders get tired and move on.

- Don't argue in generalities: “This is too low” is weak. “You applied excessive depreciation to maintained oak flooring and omitted required detach-and-reset work” is stronger.

If the dispute involves significant dwelling damage, major contents loss, or commercial property with complex valuation issues, get professional claim help before the record hardens against you.

When to Call for Reinforcements Get Help From For The Public Adjusters

Some claims can be corrected with a sharp written dispute and better documentation. Others won't move because the carrier has already decided what it wants to pay.

Signs you're being stalled or undercut

Call for help when the pattern looks like this:

- The insurer won't provide worksheets: If the company hides the depreciation basis, it knows the math won't hold up well under scrutiny.

- The adjuster keeps changing positions: One call says more documents are needed. The next says the estimate is final.

- The scope is obviously incomplete: Structural damage, moisture-related damage, smoke contamination, code-related items, or business property details are being glossed over.

- The carrier is dragging communication out: Long delays wear policyholders down and help insurers close files cheaply.

- The offer is presented as take-it-or-leave-it: That's usually a pressure tactic, not the last lawful word on the claim.

These red flags matter most in fire, water, hurricane, wind, and hail losses affecting homes, dwellings, and business properties. Those claims produce the biggest valuation gaps and the biggest documentation fights.

What professional claim help changes

A public adjuster works for the policyholder, not the insurance company. That changes the entire dynamic. Instead of reacting to the carrier's estimate, the claim gets rebuilt from the loss outward through inspection, scope development, valuation support, and negotiation.

If you're trying to understand that role, this explanation of what a public adjuster does for a property claim gives the basics.

One option for NC and VA property claims is For The Public Adjusters, Inc., a licensed public adjusting firm that handles homeowner, dwelling, and business owner property losses and provides claim review, documentation, estimate preparation, and negotiation support. That kind of help matters when the issue isn't whether damage exists, but whether the insurer is valuing it fairly.

You do not need to keep arguing with a carrier that is hiding the numbers, trimming the scope, or using insurance actual cash value as cover for an underpayment. At that point, the smart move is to put a professional between you and the insurer's process.

If your home or business claim in North Carolina or Virginia has been delayed, underpaid, or reduced through a low-ball ACV calculation, get a no-cost claim review from For The Public Adjusters, Inc.. They represent policyholders, not insurance companies, and can help review the carrier's estimate, challenge improper depreciation, document the full scope of damage, and push the claim toward the amount owed.