You paid for coverage. Then the insurance company sends its adjuster, narrows the damage, blames part of it on wear, part on water, part on “old issues,” and the settlement doesn’t come close to what it takes to repair your home.

That’s where most homeowners get trapped. They ask, what does the homeowners insurance cover, but the better question is this: what is the carrier trying not to cover on your claim?

I’m going to answer this the way a public adjuster should. Straight. Your policy can protect your home, detached structures, belongings, and temporary living costs. It can also become a weapon against you when the insurer twists definitions, applies the wrong deductible, or shrinks the scope of damage.

If you’re in North Carolina or Virginia and you’re fighting a denied, delayed, or low-ball property claim, you need more than a glossary. You need to know where the carrier cuts corners and how to push back.

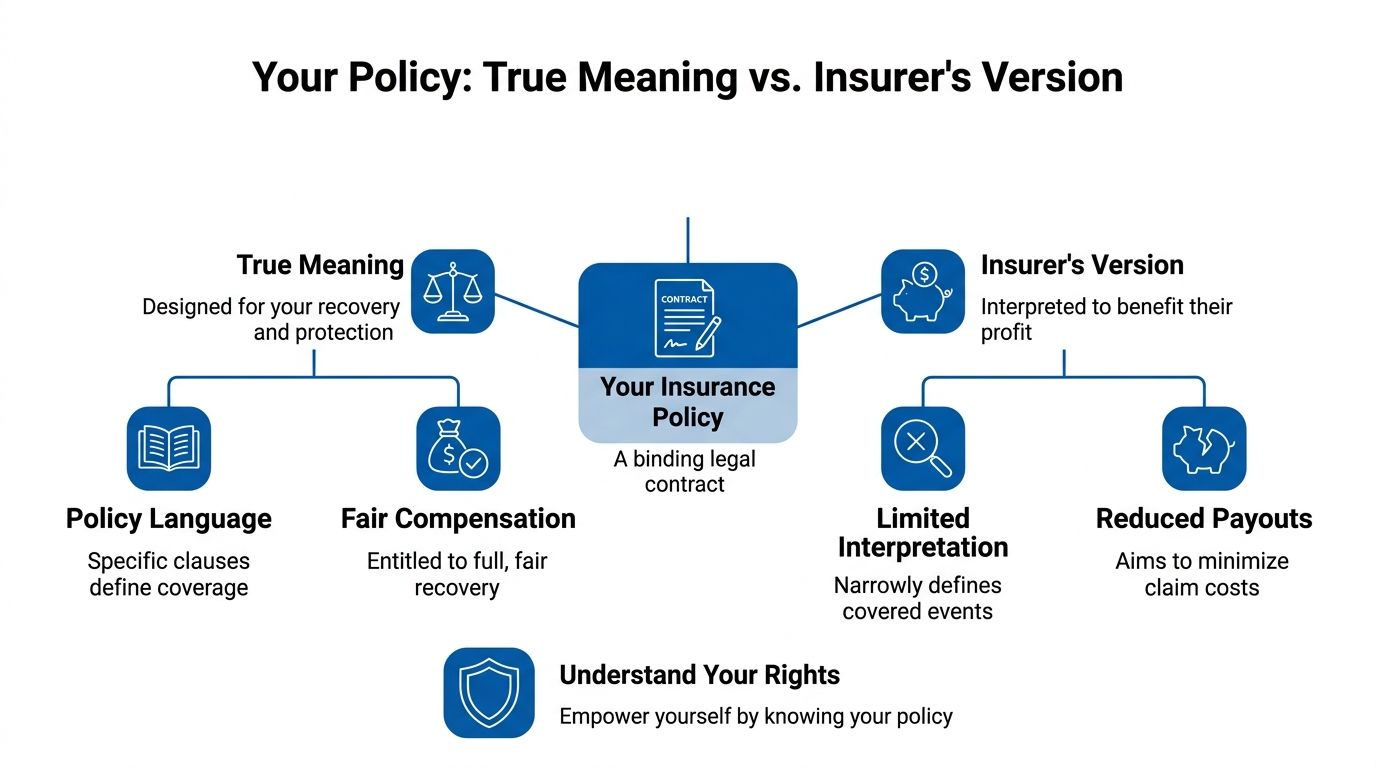

Your Policy’s True Meaning Versus The Insurer’s Version

Your homeowners policy is a contract. That’s the good news.

The bad news is that insurers frequently treat it like a flexible script. When the loss is large, they become very interested in narrow readings, exclusions, sub-limits, depreciation, and technical wording that somehow always benefits them.

The core coverages that matter in a real dispute

In standard homeowners coverage, Dwelling pays to rebuild the house itself. Other Structures coverage typically starts at a fraction of the dwelling limit. Personal Property coverage typically falls within a common range of the dwelling limit. Loss of Use is often 20% to 30% of the dwelling limit, according to the Insurance Information Institute facts on homeowners and renters insurance at https://www.iii.org/fact-statistic/facts-statistics-homeowners-and-renters-insurance.

Those categories sound simple. They aren’t simple once a claim is on the table.

Here’s how the fight typically breaks down:

- Dwelling Coverage gets cut by scope: The carrier writes for patching instead of replacing. It leaves out overhead, profit, code issues, hidden water migration, or full-room matching.

- Other Structures get ignored: Fences, sheds, detached garages, and similar structures are easy for insurer adjusters to skip or under-measure.

- Personal Property gets depreciated hard: The insurer wants age, condition, and value interpreted in the cheapest possible way.

- Loss of Use gets squeezed: Temporary housing costs get challenged, delayed, or treated like they should end before the home is livable.

Practical rule: If the insurer wrote the estimate before fully documenting every damaged area, the payment is probably too low.

What the insurer’s version usually looks like

Property damage claims are common, with wind/hail at 22% and water damage at 17% of claims in the cited III data, and in storm-prone NC and VA, 30% to 40% of claims face initial denials or delays in the same source at https://www.iii.org/fact-statistic/facts-statistics-homeowners-and-renters-insurance. That matters because delay is not an accident. Delay gives the carrier an advantage.

Insurers know many homeowners don’t read the entire policy. They read the declarations page, see a limit, and assume they’re protected.

That’s not enough.

You need the full form, endorsements, deductibles, and exclusions. If you’ve never been shown how to decode those pieces, start with this guide on https://forthepublicadjusters.com/blog/how-to-read-insurance-policy/.

If you’re comparing carriers before a loss or reviewing whether your current policy is thin in key areas, a practical reference like Florida homeowners insurance comparison can help you spot how coverages and deductibles vary from one insurer to another.

What your policy should mean in practice

A fair reading of the contract means this:

| Coverage area | What you should demand |

|---|---|

| Dwelling | Full repair scope for all covered physical damage |

| Other Structures | Separate inspection of detached items, not assumptions |

| Personal Property | Item-by-item review, not blanket undervaluation |

| Loss of Use | Actual living expenses for the period the home is not fit to occupy |

The insurer’s first estimate is not always the full story. It’s an opening position.

If you understand that early, you stop treating the carrier’s number like a verdict. You start treating it like something to challenge.

Covered Perils And The Loopholes They Exploit

A standard HO-3 policy covers 16 named perils, including fire, lightning, windstorm, hail, explosion, riot, smoke, vandalism, theft, falling objects, accidental discharge of water, and several others, as outlined in Bankrate’s North Carolina homeowners insurance coverage breakdown at https://www.bankrate.com/insurance/homeowners-insurance/north-carolina/.

That sounds broad. It is broad on paper.

In a live claim, the insurer hunts for a way to reclassify covered damage into an excluded category.

Fire, water, and wind are where the excuses start

Fire claims are expensive, and the insurer knows it. Nationally, fire and lightning accounted for 28% of property claims from 2020 to 2024 and averaged $83,991 per claim, according to the Bankrate summary based on industry data at https://www.bankrate.com/insurance/homeowners-insurance/north-carolina/. That’s why carriers fight contamination, smoke spread, and full replacement questions so aggressively.

With water damage, the typical tactic is to admit the event happened but argue the visible deterioration proves long-term seepage, poor maintenance, or neglect. They try to turn a sudden loss into a maintenance issue.

With wind damage, they love the phrase “wear and tear.” Missing shingles become age. Creased tabs become installation defects. Interior staining becomes an old leak.

If wind opened the roof system and water entered after that opening, the causation analysis matters more than the carrier’s first opinion.

The loophole language you should challenge

Insurers frequently lean on these arguments:

- “It was pre-existing.” That’s often based on a rushed inspection or selective photos.

- “It’s cosmetic only.” Cosmetic to them can still mean functional damage to roofing, siding, or interior finishes.

- “It was gradual.” That conclusion falls apart when the damage pattern matches a sudden event.

- “It’s below the deductible.” Sometimes that’s because the estimate itself is artificially stripped down.

Here’s the practical issue. The policy may cover the peril, but the insurer narrows the cause, the scope, or the price of repair until the claim becomes too small to matter.

What evidence beats those arguments

You don’t win these disputes by arguing in general terms. You win them with disciplined documentation.

A strong rebuttal typically includes:

- A room-by-room damage map that ties each condition to the covered event.

- Exterior and interior photo sequencing that shows the path of damage.

- Repair logic explaining why partial work won’t restore the property.

- Independent contractor or expert support where the carrier blamed age or neglect.

If your roof is part of the dispute, routine maintenance records can help neutralize the “poor upkeep” argument. That’s one reason homeowners review practical upkeep resources such as how roof cleaning can benefit your insurance. Maintenance doesn’t create coverage, but it can help block the insurer’s favorite excuse.

Don’t let covered peril become uncovered story

The fight is rarely over whether fire, wind, or sudden water is listed. The fight is over the story the insurer tells about how the damage happened.

That’s where homeowners lose money. They accept the carrier’s narrative before testing it.

Don’t do that. If the policy covers the peril, force the insurer to explain, in writing, exactly why it thinks your actual damage falls outside that coverage.

How to Fight Unfair Deductibles And Low-Ball Limits

The declarations page has two numbers that can wreck a claim if you don’t challenge them. Your deductible and your coverage limit.

Insurers use both to shift the financial burden back onto you.

The split deductible trap

In North Carolina, many homeowners policies frequently use a split wind/hail deductible. A lower flat deductible may apply to losses like fire, but wind and hail claims often trigger a percentage deductible of 1% to 5% of the dwelling coverage limit, according to Callahan & Rice’s discussion of hurricane deductibles in North Carolina at https://www.callahanrice.com/does-my-homeowners-insurance-cover-hurricanes-in-north-carolina/.

For a home with $300,000 in dwelling coverage, a 2% wind deductible means $6,000 out of your pocket before the insurer pays anything, based on that same source.

That deductible issue becomes a dispute when the carrier applies the wind deductible too broadly, uses it to cut a marginal payment down to almost nothing, or hides behind it while ignoring parts of the covered damage.

How carriers use low limits against you

A lot of homeowners assume the dwelling limit reflects current rebuild cost. That assumption is dangerous.

Sometimes the limit is outdated. Sometimes the carrier never pushed hard enough to increase it. Sometimes a homeowner accepted lower limits to control premium without understanding what it would mean after a major loss.

The result is predictable. The insurer says, “We paid according to the policy.” Meanwhile, the policy itself may have been too thin for the actual rebuilding job.

What to challenge first: whether the insurer is using the right deductible for the right peril, and whether its estimate ignores covered work that would move the claim well above that deductible.

Replacement cost versus low-ball valuation

You also need to know whether the insurer is paying replacement cost value or trying to hold the claim down through actual cash value logic. In plain English, one approach is closer to what it costs to repair or replace. The other strips value out based on age and condition.

That difference can change the entire negotiation.

Use this coin insurance explainer to understand how policy math can affect payment disputes: https://forthepublicadjusters.com/blog/what-is-a-coinsurance/

Here’s a simple comparison:

| Issue | Carrier tactic | Homeowner response |

|---|---|---|

| Wind deductible | Apply higher percentage deductible and move on | Demand the exact policy language and endorsement relied on |

| Coverage limit | Treat current limit as untouchable | Review whether endorsements or valuation language create additional arguments |

| Valuation | Start from depreciated figures | Push for full covered scope and proper replacement cost handling |

Clear recommendations

Don’t accept a deductible explanation over the phone. Get it in writing.

Don’t assume the declarations page tells the whole story. Read the endorsements.

Don’t let the insurer shrink the estimate first and then tell you the claim falls below the deductible. That’s a classic low-ball move.

If the carrier’s estimate feels engineered to land just under the threshold, trust that instinct and have the scope reviewed line by line.

The Flood And Wind Damage Traps In Your Policy

This is the harshest part of the homeowners policy and the part carriers exploit hardest after hurricanes and major storms.

Standard homeowners insurance does not cover flood damage.

Not shallow flooding. Not storm surge. Not rising water that enters through the door, foundation, or lower wall assembly. If it’s flood under the policy definition, the homeowners carrier will point to the exclusion and shut that door fast.

Where the flood exclusion becomes a claim weapon

Flood coverage usually requires a separate NFIP policy, and the NFIP dwelling cap is $250,000, as summarized in The Zebra’s hurricane damage coverage discussion at https://www.thezebra.com/homeowners-insurance/coverage/does-homeowners-insurance-cover-hurricane-damage/.

After a hurricane, the fight often becomes wind versus water. The insurer looks for any evidence of rising water and then tries to push as much damage as possible into the flood bucket.

In coastal areas of NC and VA, insurers often deny up to 40% of claims when a flood policy isn’t also in place, according to that same source at https://www.thezebra.com/homeowners-insurance/coverage/does-homeowners-insurance-cover-hurricane-damage/. Their argument is simple. They say water caused it, not wind.

Why causation decides the money

If wind damages the roof, wall system, windows, or doors first, and wind-driven rain enters through that opening, that can be a homeowners claim issue rather than a flood issue.

That distinction is everything.

Public adjusters and other claim professionals often use engineering analysis and meteorological data to prove the sequence of damage. The question isn’t just whether water was present. The question is how it entered and what failed first.

Wind-created opening arguments can force coverage where the insurer wanted to blame everything on excluded water.

If you’re dealing with storm-related damage and the carrier is playing games with causation, this storm damage claim resource is worth reviewing: https://forthepublicadjusters.com/blog/storm-damage-insurance-claim/

NFIP and last-resort wind coverage are different battles

NFIP claims are rigid. The forms are rigid. The documentation standards are rigid. The adjuster may be working under rules that feel more bureaucratic than practical.

Coastal wind coverage can be just as frustrating when you’re placed into a residual market or last-resort setup. The deductibles are often painful, and the claim process can feel designed to wear people down.

Here’s the problem many homeowners run into:

- They assume one policy handles all storm damage

- They don’t know which carrier should pay which portion

- They let the insurers argue with each other while repairs stall

The recommendation I give homeowners

If there is any chance your loss involves both wind and flood, do not let the homeowners carrier define the entire claim before the evidence is fully documented.

Get the timeline of the storm. Get photographs of openings. Get elevations, water lines, roof conditions, and interior entry paths documented. The difference between flood and wind causation can decide whether you recover meaningful money or almost nothing under the homeowners policy.

This is one area where a sloppy inspection costs homeowners significantly.

From Low-Ball To Full Recovery A Public Adjuster Case Study

Low-ball offers typically follow a pattern. The insurer inspects fast, writes narrow, and pays as if the visible damage is the whole loss.

That approach gets dangerous when the policyholder is also underinsured and doesn’t know it.

The underinsurance problem hidden inside the claim

The Philadelphia Fed has identified coverage neglect as a significant issue, where homeowners can be substantially underinsured because policy limits haven’t kept up with rebuilding costs. The same research found that every 10 percentage point increase in underinsurance reduced the likelihood of filing a rebuilding permit within one year of a major wildfire by 4 percentage points, according to the Philadelphia Fed at https://www.philadelphiafed.org/consumer-finance/coverage-neglect-in-homeowners-insurance.

That matters in a property claim because the insurer seldom volunteers this problem early. It benefits the carrier when the homeowner discovers the gap late, after the low estimate, after the partial payment, and after the contractor pricing comes in.

What a real claim fight looks like

A homeowner calls after a storm loss. The carrier has already inspected. The estimate is thin. Major line items are missing. The insurer acts like the disagreement is just a pricing issue.

It is not always just pricing.

A serious re-evaluation frequently uncovers things the carrier skipped:

-

- Structural impact hidden above finished ceilings or in attic spaces

- Insulation, sheathing, or framing damage that wasn’t included

- Detached structure damage omitted from the original scope

- Coverage limit problems that increase settlement pressure on the homeowner

At that point, the dispute changes. It’s no longer “why is your number higher?” It becomes “why did the insurer ignore obvious damage and fail to evaluate the loss correctly?”

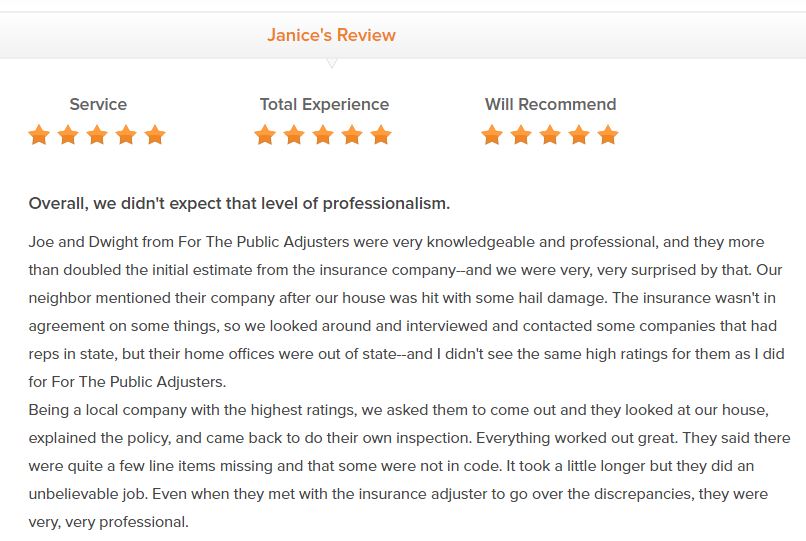

A review that says a lot

A strong client review frequently tells you what happened without legal jargon. The common themes are familiar. The carrier delayed. The estimate was short. The homeowner felt outmatched. Then someone competent documented the loss properly and pushed the claim back where it belonged.

That’s the value of independent claim analysis. Not cheerleading. Documentation.

A low-ball offer isn’t proof your claim is weak. It often proves the insurer controlled the first version of the facts.

What changes the outcome

When a claim is reworked correctly, the process typically includes:

- Policy analysis to identify every applicable coverage part and endorsement.

- A fresh scope built from actual observed damage, not insurer shortcuts.

- Repair pricing support tied to the actual work required.

- A causation argument where the carrier blamed excluded conditions.

- Escalation through appraisal or formal dispute channels if the insurer refuses to move.

For homeowners who need outside help, For The Public Adjusters, Inc. is one option that performs claim review, policy interpretation, damage documentation, estimate preparation, and negotiation for NC property losses.

The opinion homeowners need to hear

Insurers count on exhaustion. They count on confusion. They count on the fact that many people have never handled a major property claim before.

That’s why low-ball settlements frequently happen.

The turning point is when the homeowner stops arguing emotionally and starts presenting a stronger file than the insurance company’s own adjuster prepared. Once that happens, the carrier has to deal with facts instead of assumptions.

Your Game Plan To Dispute A Low-Ball Offer Or Denial – What Does The Homeowners Insurance Cover?

If the insurance company already gave you a number that won’t cover the work, or denied part of the damage, stop reacting and start building your file.

That’s how you regain an advantage.

Step one gets skipped too often

Get the complete policy, not just the declarations page.

You need the form, endorsements, deductible provisions, exclusions, and any special language tied to wind, hail, water, or replacement cost. If the insurer is quoting policy language but won’t send the whole document promptly, that’s a warning sign.

Then read the denial letter or estimate like an opponent would. Circle every phrase that narrows the claim. Words like “appears,” “wear and tear,” “long-term,” “not storm related,” and “below deductible” are not conclusions. They are positions.

Build your own evidence file

Do not rely on the carrier’s photos, notes, or measurements.

Create your own claim record with:

- Wide and close photos: Exterior elevations, roof slopes if safely visible, each damaged room, and all transitions where water traveled.

- Video walkthroughs: Narrate what you’re seeing and date the recording.

- A communication log: Keep names, dates, times, and a short summary of every call.

- All receipts and mitigation records: Emergency dry-out, tarping, debris removal, temporary repairs, lodging, and meals where applicable under the policy.

At this point, homeowners often realize the insurer’s inspection was nowhere near complete.

Respond in writing, not by phone alone

If the offer is low, dispute it in writing.

Keep it tight. State that you disagree with the carrier’s scope, pricing, causation position, deductible application, or combination of those issues. Attach supporting photos, contractor estimates, expert notes, or any documentation that directly rebuts their position.

Written disputes matter: Phone calls disappear. Letters and emails create a record the carrier can’t deny later.

A simple structure works well:

| What to include | Why it matters |

|---|---|

| Claim number and property address | Prevents “we never got it” confusion |

| Specific dispute points | Forces the carrier to answer the actual issues |

| Supporting documents | Shifts the conversation from opinion to evidence |

| Request for revised evaluation | Makes your demand clear |

Know when the fight has become technical

Some disputes are too technical for a homeowner to carry by themselves.

That’s especially true when:

- The loss involves structural components

- The carrier raises causation issues

- The estimate misses entire categories of damage

- The insurer issues a reservation of rights

- The policy language is being used against you in a selective way

At that stage, you need more than a contractor price. You need claim strategy.

This video gives a practical view of how policyholders can think about the dispute process:

What not to do

Don’t cash a check and assume the matter is over without reading any release language.

Don’t let the insurer rush you into agreeing that the damage is minor.

Don’t assume the company’s adjuster is neutral. That adjuster may be polite, but the carrier controls the payment decision.

Final recommendations

Ask for explanations in writing.

Challenge unsupported conclusions.

Organize your evidence before the insurer organizes its defense.

And if the dispute is getting more technical by the day, stop trying to outlast a company that handles claims for a living. Bring in someone who handles property claim disputes for policyholders.

If your homeowners, dwelling, or commercial property claim has been delayed, denied, or low-balled, contact For The Public Adjusters, Inc.. They work for policyholders in North Carolina, not for the insurance company, and they can review the policy, inspect the damage, document the full scope, and help dispute an underpaid settlement.