Let’s be honest. When you’re dealing with a USAA claim after your property has been damaged, you’re not just dealing with a simple process. You're up against a calculated strategy designed to pay you as little as possible.

Like any other major insurer, USAA sends out adjusters whose real job is to protect the company's money. It’s an inherent conflict of interest that turns what should be a straightforward recovery into a frustrating, uphill battle for homeowners and business owners across North Carolina and Virginia.

Why Your USAA Claim Might Be an Uphill Battle

After a fire, storm, or burst pipe wrecks your home or business, you expect your insurance company to be your partner. You’ve paid your premiums on time, every time. Now you need them to hold up their end of the deal.

But so many policyholders find out the hard way that filing a USAA claim isn't a team effort. It's a fight. The company's goal is almost always to minimize their payout, which puts you at a huge disadvantage from the very first phone call.

The adjuster they send over might seem friendly, but their loyalty is to USAA's profits, not your recovery. Their entire job is to pick apart your policy, find loopholes, lowball the cost of repairs, and second-guess the true extent of your losses. This isn't an accident. It's their business model.

Tactics USAA May Use to Weaken Your Claim

Insurance companies are experts at the "delay, deny, defend" game. They know that the longer they can drag out your claim, the more likely it is that you—stressed out and financially drained—will just give up and take whatever lowball settlement they throw at you.

Here are a few of the classic tactics you can expect:

- Twisting Your Policy Language: USAA might point to some obscure, confusing clause in your policy to argue that certain types of damage aren't actually covered.

- Lowballing Repair Costs: The adjuster’s first estimate will almost certainly use cheap materials and rock-bottom labor rates that no reputable local contractor would ever accept.

- Creating Endless Delays: They might ask for the same information over and over again or just stop responding for weeks at a time, hoping you’ll get tired and go away.

- Arguing About the Cause of Damage: With water damage, for example, they love to argue that it was caused by long-term neglect, not a sudden accident. This is a common problem in fire claims, too—you can learn more about the common reasons insurance companies deny fire claims in our detailed guide.

The reality of this strategy was put on full display in Parr v. USAA. In this case, a Texas court found USAA had acted in bad faith by lowballing a homeowner's legitimate storm damage claim. The jury sided with the policyholder, awarding significant damages and sending a clear message that these tactics are unacceptable. This is just one example of how insurance companies can lose when homeowners fight back.

The Role of a Public Adjuster

This is where you can flip the script. While the USAA adjuster works for them, a public adjuster works only for you.

A public adjuster is a state-licensed professional who becomes your advocate, fighting on your behalf to make sure you get a fair and just settlement. They level the playing field by bringing their own deep expertise in policy language, damage estimating, and negotiation to your side of the table.

From the moment you hire one, a public adjuster takes over. They start with their own detailed inspection, meticulously document every single loss, and build a rock-solid file of evidence. They manage all the phone calls and emails with USAA, shutting down their lowball tactics with hard facts and expert analysis.

When you bring in an advocate who knows the insurer's playbook inside and out, you protect yourself from the very beginning and dramatically increase your odds of a successful financial recovery.

Your First 48 Hours After a Property Loss

The chaos right after a fire, hurricane, or busted pipe is disorienting. But what you do in those first two days is absolutely critical. These actions set the entire tone for your claim and can put you in control before the USAA adjuster—whose job is to limit the payout—ever sets foot on your property.

Your policy requires you to do one thing immediately: mitigate further damage. This is non-negotiable. It simply means taking reasonable steps to stop the problem from getting worse.

If a tree smashed through your roof, you need to get it tarped. Now. If a supply line floods your kitchen, you call a water extraction company to start the drying process before mold gets a foothold.

But here’s the crucial distinction: you mitigate, you don't repair. Tarping the hole is mitigation. Hiring a roofer to start replacing shingles is a permanent repair. USAA will absolutely use premature, unauthorized repairs as an excuse to deny your claim, arguing they never got to see the "real" damage.

Start Your Claim Journal Immediately

From the moment you dial USAA's number, you need to become a relentless record-keeper. Grab a notebook or open a new document and log every single interaction. This journal is your best weapon against the delays, confusion, and "he said, she said" games insurance companies play to wear you down.

For every single phone call, write down:

- The date and time.

- The full name and title of the USAA rep you spoke with.

- A clear summary of the conversation, especially any promises or deadlines they gave you.

- Any next steps you or they are supposed to take.

Save every email. Every letter. This log creates an undeniable timeline. It makes it nearly impossible for USAA to later claim a conversation never happened or that you misunderstood. It’s your proof if you ever need to argue they created unreasonable delays.

Keep every single receipt for any out-of-pocket expense. Tarps, plywood, a hotel room if you’re displaced, even meals. These are often covered under your policy, but without a receipt, it’s your word against theirs.

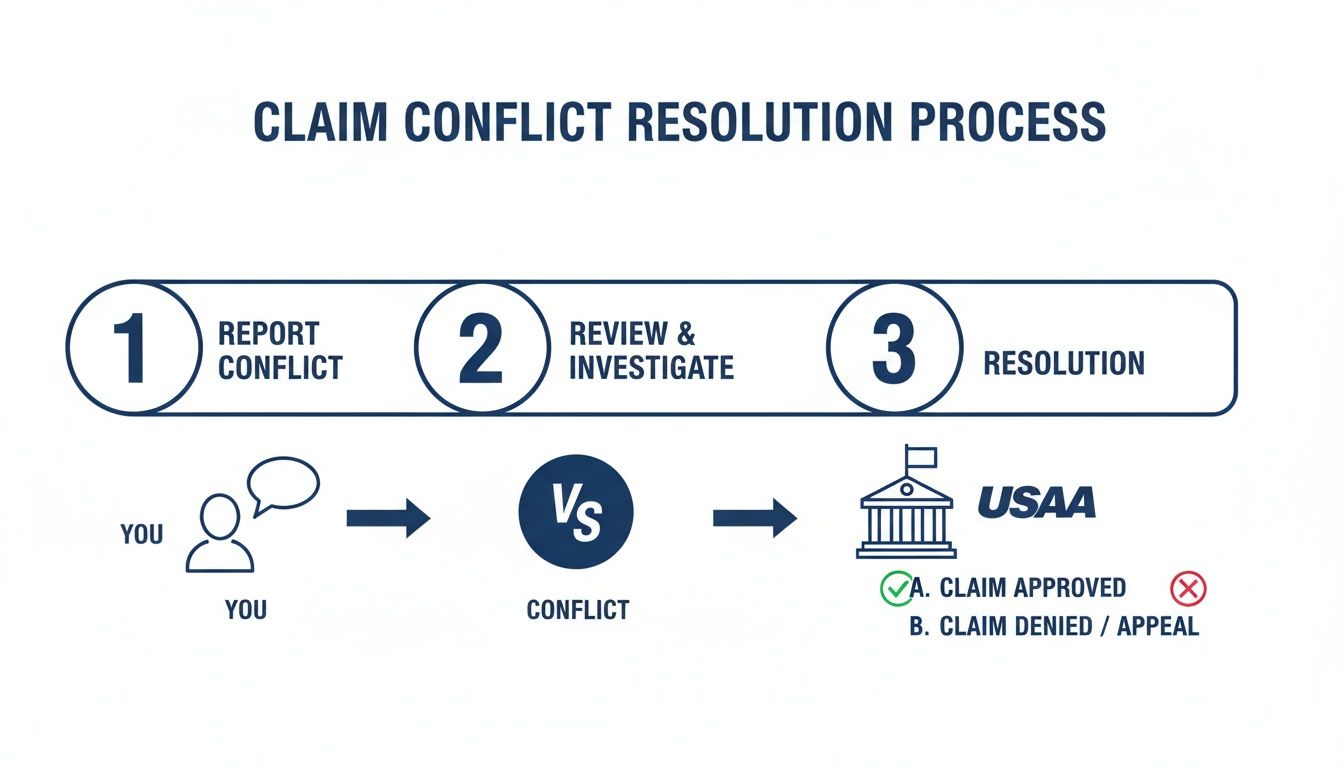

The infographic below shows how quickly a simple claim report can devolve into a conflict between what you need and what the insurance company wants to pay.

This is why having your own documented evidence from day one is so important. When you get to the "Review" phase, you’re not just relying on their assessment—you have your own.

Submitting Formal Documentation

Soon after you report the claim, USAA will send you a "Sworn Statement in Proof of Loss" form. Don't be fooled by the generic name. This is a legally binding document where you state the facts and value of your loss under oath.

Do not rush this. Any mistake, any omission, can and will be used against you later.

Accuracy is everything. You are legally swearing that the information is true. This is one of those moments where getting an expert, like a public adjuster, to review the document before you sign can save you a world of hurt. You need to understand exactly what a Proof of Loss form is and the traps it contains. Getting this document right from the start builds a foundation for your claim that USAA can’t easily tear down.

Building an Evidence File USAA Cannot Ignore

Let’s be blunt. A successful USAA claim isn't won with a few blurry photos you snapped in a panic. It's won with a mountain of undeniable proof that tells the complete, devastating story of your loss.

Your goal is to build an evidence file so thorough, so detailed, that it leaves the USAA adjuster with zero room to argue, undervalue, or deny what you're rightfully owed. Think of yourself as an investigator building a case. The adjuster's job is to find holes in your story to minimize their payout; your job is to make your case airtight.

This isn't just about taking pictures. It's about creating a powerful narrative that proves what you lost, what it was worth, and why you are owed a full and fair settlement under the policy you paid for.

Mastering Photographic and Video Documentation

Right now, your smartphone is your most important tool. Don't just point and shoot—be strategic. Your documentation needs to capture the big picture and the tiny details that prove the full scope of your damages.

Start by recording a slow, narrated video walkthrough of your entire property. Go room by room, speaking out loud about what you're seeing as you film. Be sure to open every cabinet, closet, and drawer. This video sets the stage and provides crucial context for the detailed photos to follow.

When you switch to taking photos, stick to this method:

- Go Wide, Then Get Close: Take wide shots of each room to show the overall scene. Then, move in for medium shots and tight close-ups of every single damaged item and structural problem.

- Show the Scale: Place a ruler, a coin, or even your car keys next to smaller damaged areas like cracks or water stains. This gives the adjuster an undeniable sense of scale they can't ignore.

- Capture It All: Photograph damaged walls, floors, ceilings, furniture, appliances, and personal belongings. Don't forget to look up—those water stains on the ceiling are often the first sign of hidden roof damage or a major plumbing leak.

Don’t just document the damage. You have to prove the "before" picture, too. Dig through your phone, old social media posts, and family photo albums for any pictures or videos that show your home and belongings before the disaster. A single photo from last year's Christmas party showing your living room in perfect condition can instantly shut down an adjuster’s attempt to claim the damage was pre-existing.

Creating an Unshakable Personal Property Inventory

Documenting the structure of your home is only half the battle. For most families, the contents inside—the furniture, electronics, clothing, and memories—are worth just as much. This is precisely where USAA will try to slash your settlement, arguing your things were old or not worth much.

Your best defense is a painfully detailed inventory. Create a spreadsheet and, for every single item damaged or destroyed, list the following:

- Item Description (e.g., "Samsung 65-inch 4K Smart TV, 2022 model")

- Manufacturer/Brand

- Model & Serial Number (if you can find it)

- Age of the Item

- Original Purchase Price

- Estimated Replacement Cost (find current prices online today)

- A direct link to a comparable new item for sale

Yes, this is tedious work. But it is absolutely critical. A vague entry like "TV" might get you a check for a few hundred dollars. A fully documented entry with a model number and a link to its $1,500 replacement on Best Buy’s website is almost impossible for USAA to fight.

Homeowner Documentation vs Public Adjuster Evidence File

While any policyholder can put together a good file, a professional public adjuster operates on an entirely different level. We know exactly what insurance company lawyers look for, what software they use, and how to present evidence in a way that forces a fair and honest evaluation. The difference is stark.

| Evidence Type | Typical Homeowner Approach | Public Adjuster Professional Standard |

|---|---|---|

| Damage Photos | Takes general photos of the obvious damage with a smartphone. | Uses high-resolution cameras, moisture meters, and infrared thermal imaging to uncover and document hidden water and structural damage behind walls. |

| Contents Inventory | Creates a basic list of major items, often from memory. | Conducts a forensic, room-by-room inventory, detailing every single item down to the last fork, sock, and spice jar, then values it properly. |

| Repair Estimates | Gets one or two simple estimates from local contractors. | Prepares a highly detailed, line-item estimate using industry-standard software like Xactimate that insurers are required to recognize and respect. |

| Policy Analysis | Reads the policy summary to understand the basics. | Scrutinizes every line of the policy to find all applicable coverages, endorsements, and building code requirements that maximize the claim's final value. |

At the end of the day, the strength of your evidence file directly dictates the size of your settlement check. By being this meticulous, you shift the power dynamic back in your favor. You're sending a clear message to USAA: you know what your claim is worth, and you won't accept a penny less.

How to Dispute a Lowball Offer or Denial

That settlement offer from USAA finally hits your inbox, and your stomach drops. The number is insultingly low. Or worse, it’s an outright denial.

Your first feeling is probably despair, but you need to switch gears fast. This isn’t the end of your claim. It’s the start of the real fight.

Let’s be blunt: a lowball offer or denial is a business tactic. USAA is making an opening bid in a negotiation they hope you’re too exhausted and overwhelmed to engage in. They are betting you'll just take what you can get and go away.

Your job is to prove them wrong.

Make Them Justify It—In Writing

Your first move is to put the burden of proof squarely back on USAA’s shoulders. Forget arguing on the phone; it's a waste of time and energy.

Instead, send a formal, written request (an email is perfect because it creates a paper trail) demanding two very specific things:

- The Exact Policy Language: Tell them to point to the specific sections, clauses, and exclusions in your policy that justify their decision. Make them show you the precise words in the contract.

- All Their Evidence: Demand copies of every report, estimate, photograph, and expert opinion they used to come up with their number. You have a right to see the "evidence" they're holding against you.

This one simple act forces them to stop hiding behind vague excuses like "that's not covered" and puts them on the defensive. It also gives you the exact blueprint you need to dismantle their argument, piece by piece.

Build Your Counter-Offensive

Once you have USAA’s reasoning in hand, it’s time to build your counter-attack. That detailed evidence file you’ve been compiling? It’s now your most powerful weapon. Your response needs to be a professional, point-by-point rebuttal that systematically tears down their assessment.

Your rebuttal package must include:

- Your Detailed Inventory: Your comprehensive list of every damaged item, complete with current replacement costs and links to comparable new products.

- Independent Contractor Estimates: Get at least two detailed, line-item estimates from trusted local contractors. These real-world numbers from pros who actually work in your area will instantly expose how unrealistic USAA's estimate is.

- Expert Reports: If the situation calls for it, bring in your own engineer, industrial hygienist, or certified roofer. A professional report that directly contradicts the findings of USAA's adjuster is incredibly powerful.

When you're fighting a low offer on roof damage, proving the market rate is critical. Having data on the average cost for roof replacement in your area gives you a solid, factual baseline to counter an insurer's low figures.

Success Story: Turning the Tables in Virginia

A Virginia homeowner got a lowball offer of just $22,000 from USAA after a hailstorm destroyed his roof and siding. The USAA adjuster insisted the damage was "minor." The homeowner hired a public adjuster who immediately brought in a certified engineer. The engineer’s report confirmed widespread, storm-created damage requiring a full replacement to meet current building codes. Armed with this expert report and a detailed contractor estimate, the public adjuster reopened negotiations. The final settlement was over $75,000—more than triple the initial offer. This demonstrates how an expert advocate can completely change the outcome of a claim.

Unleash the Appraisal Clause

If USAA still won’t budge, your policy contains a powerful but rarely used tool: the Appraisal Clause. This is a formal dispute resolution process built right into most homeowner policies, designed for situations just like this.

Here’s how it works:

- You hire an independent, impartial "appraiser" (this is often a public adjuster or a highly experienced contractor).

- USAA hires their own independent appraiser.

- The two appraisers review all the evidence and try to agree on the actual amount of the loss.

- If they can’t agree, they select a neutral "umpire" who listens to both sides and makes a final, binding decision.

Invoking appraisal yanks the decision out of the hands of the USAA adjuster who lowballed you. It forces the claim to be judged by outside experts based purely on the facts you’ve so carefully put together. This move alone signals that you are serious and will not be pushed around, often leading to a much better offer before the appraisal process even finishes.

When You Need a Public Adjuster in Your Corner

Let’s be blunt: trying to go head-to-head with a corporate giant like USAA after a major property loss is a recipe for disaster. You’re already emotionally shattered and financially strained. That’s not a weakness; it's a reality. And it's precisely the state your insurer is counting on.

They know an exhausted and overwhelmed homeowner is far more likely to accept a lowball offer just to make the nightmare end. But there's a tipping point where you realize this isn't a negotiation—it's a fight you can't win alone. That’s the moment hiring a professional advocate becomes non-negotiable.

Red Flags That Signal You Need Help Now

Some moves from USAA aren't just frustrating administrative hurdles; they are calculated tactics meant to grind you down and underpay your claim. If you see any of these, it’s time to bring in a public adjuster.

- An Outright Denial: This is USAA’s nuclear option. They are betting you lack the expertise and sheer willpower to fight their decision. A public adjuster’s first order of business is often to force USAA to reopen a claim they wrongfully denied.

- Significant Damage (Over $25,000): The moment your claim crosses a certain financial threshold, USAA’s incentive to delay and undervalue skyrockets. For any substantial loss, getting an expert on your side from day one is critical.

- Complex or Hidden Issues: Is your claim tangled up with hard-to-prove damage from smoke, mold, or widespread water intrusion? You can bet the company adjuster will try to minimize the scope of repairs. These issues demand specialized knowledge to document correctly.

- Unexplained Delays: Is your adjuster suddenly ghosting you? Are they requesting the same documents for the third time? These are classic stall tactics designed to make you desperate enough to take whatever they offer.

Don’t confuse a friendly tone for a fair process. The company adjuster’s job is to protect USAA’s bottom line, period. When the stakes are high, you need someone whose only job is to protect yours.

How a Public Adjuster Takes Control of Your USAA Claim

Bringing a public adjuster into the fight immediately flips the script. Instead of you chasing USAA for answers, their adjuster now has to answer to a licensed professional who speaks their language and knows every trick in their playbook.

A public adjuster takes complete command of the claim for you. They start by conducting their own forensic-level inspection, often uncovering significant damage the company adjuster conveniently “missed.” They document every single detail of your loss to build an undeniable case for the true, full cost of your recovery.

Most importantly, they take over all communications. No more agonizing phone calls or confusing email chains. They decipher the complexities of your policy, quarterback all negotiations, and systematically dismantle USAA's lowball arguments with hard evidence and expert estimates. To really grasp their impact, it helps to understand what a public adjuster does at every stage.

A Partnership Focused on Your Maximum Recovery

For homeowners and business owners in North Carolina and Virginia, public adjusters are state-licensed professionals who work on a contingency fee basis. This is a game-changer.

You pay nothing upfront. Their fee is a small, agreed-upon percentage of the final settlement they secure for you. This means their motivation is singular and powerful: to get you the absolute maximum payout possible. If they don’t win for you, they don’t get paid.

This model perfectly aligns their interests with yours, creating a powerful partnership against the insurance company. It ensures you have an expert fighting for every single dollar you are owed under your policy, finally leveling a playing field that was designed to be tilted against you from the start.

Your Top Questions About USAA Claims Answered

When you're fighting USAA over a claim, the stress and uncertainty can be unbearable. You’re suddenly faced with questions you never thought you’d have to ask about a company you put your trust in. Let's cut through the noise and give you direct, no-nonsense answers to the questions we hear most often.

Can USAA Cancel My Policy if I Hire a Public Adjuster?

Let me be crystal clear: absolutely not.

It is illegal in North Carolina, Virginia, and every other state for an insurance company to retaliate against you for hiring a public adjuster. They can't cancel your policy, hike your rates, or punish you in any way for exercising your consumer rights.

Hiring professional representation is your right. You’re simply bringing in an expert to make sure USAA honors the contract you paid for. Anyone from USAA who suggests otherwise is using an intimidation tactic, plain and simple.

The Adjuster from USAA Seemed Nice. Should I Trust Their Offer?

Never, ever accept the first offer. Don't even consider it. The adjuster's friendly demeanor isn't genuine concern—it's a calculated strategy to build rapport so you'll quickly sign off on a lowball settlement that pads their employer's profits.

Remember, the USAA adjuster works for USAA, not for you. Their primary objective is to protect USAA’s bottom line by closing your claim for the lowest possible amount. Always get a second opinion from a trusted local contractor or, better yet, a public adjuster before you sign a single thing.

How Is a Flood Damage Claim Different?

This is a critical distinction that trips up countless homeowners. Flood damage claims are an entirely different animal and are not covered by a standard homeowner's policy.

These claims fall under a federal National Flood Insurance Program (NFIP) policy, which is governed by a rigid and unforgiving set of rules with brutally strict deadlines. The adjusters for these claims, whether from FEMA or a Write Your Own (WYO) company, are notorious for making the process a bureaucratic nightmare. They often undervalue the cost of repairs and deny legitimate parts of a claim. If you have a flood claim, you absolutely need a public adjuster with specific NFIP experience to have any chance of getting a fair settlement from these difficult federal programs.

Don't let USAA dictate the value of your recovery. If you're facing a denied, delayed, or lowballed homeowner or business owner claim in North Carolina or Virginia, you need an expert in your corner. The team at For The Public Adjusters, Inc. provides no-cost claim reviews to help you understand your options and fight back. Contact us today to level the playing field. Learn more at https://forthepublicadjusters.com.