You opened the denial letter, read the policy language twice, and still felt like you got hit a second time. First the pipe burst, leak, or hidden water intrusion tears up your house. Then State Farm acts like the damage is your fault, your maintenance problem, or somehow too old to count.

That reaction is normal. So is the anger.

A state farm denied water damage claim is often not the end of the matter. It’s the start of a fight. Big carriers know plenty of homeowners will accept the denial, clean up the mess, and move on. That’s exactly why you need a strategy, not another call where you beg the adjuster to “take another look.”

Table of Contents

- Your State Farm Water Damage Claim Was Denied Now What

- The Real Reasons State Farm Is Denying Your Claim

- Your First Moves After a Claim Denial

- How to Build and Submit a Winning Appeal

- Calling in the Pros Public Adjusters vs Attorneys

- Escalating Your Fight in North Carolina and Virginia

- A Denial Is a Negotiation Not a Final Answer

Your State Farm Water Damage Claim Was Denied Now What

The usual scene goes like this. You’ve got wet floors, damaged drywall, cabinets swelling, maybe microbial growth starting, and a house that smells wrong. You expect the insurer you paid for years to step in. Instead, you get a letter that leans on words like “seepage,” “maintenance,” “wear and tear,” or “not covered.”

That letter is designed to shut the conversation down.

I’ve seen homeowners make two bad moves right after a denial. They either give up, or they call State Farm and argue emotionally without new evidence. Neither move helps. The carrier already has its position on paper. You need to attack that position with documentation, policy language, and independent findings.

One recent example shows why homeowners shouldn’t just accept the denial. In a claim dispute covered in our write-up on a State Farm homeowners claim dispute, the core issue turned on where the failed pipe sat and how the loss was documented. That kind of detail matters because carriers often deny first and force the homeowner to prove what should have been investigated correctly the first time.

Denial doesn’t mean the facts favor State Farm

A denial letter is not a judge’s order. It’s State Farm’s version of events.

Practical rule: Treat every denial as a challenge to your evidence, not a final ruling on coverage.

If the carrier misidentified the source, skipped key inspection steps, relied on the wrong exclusion, or ignored the full scope of damage, the denial can be attacked. That’s the mindset you need. Not frustration. Not panic. Pressure.

Here’s the right posture:

- Stop reacting to the letter emotionally: Read it carefully and pull out every stated reason for denial.

- Assume the investigation was incomplete until proven otherwise: Especially if no qualified plumber, engineer, or moisture documentation supports the carrier’s position.

- Prepare for a record-based fight: The homeowner who wins usually has the better file, not the louder voice.

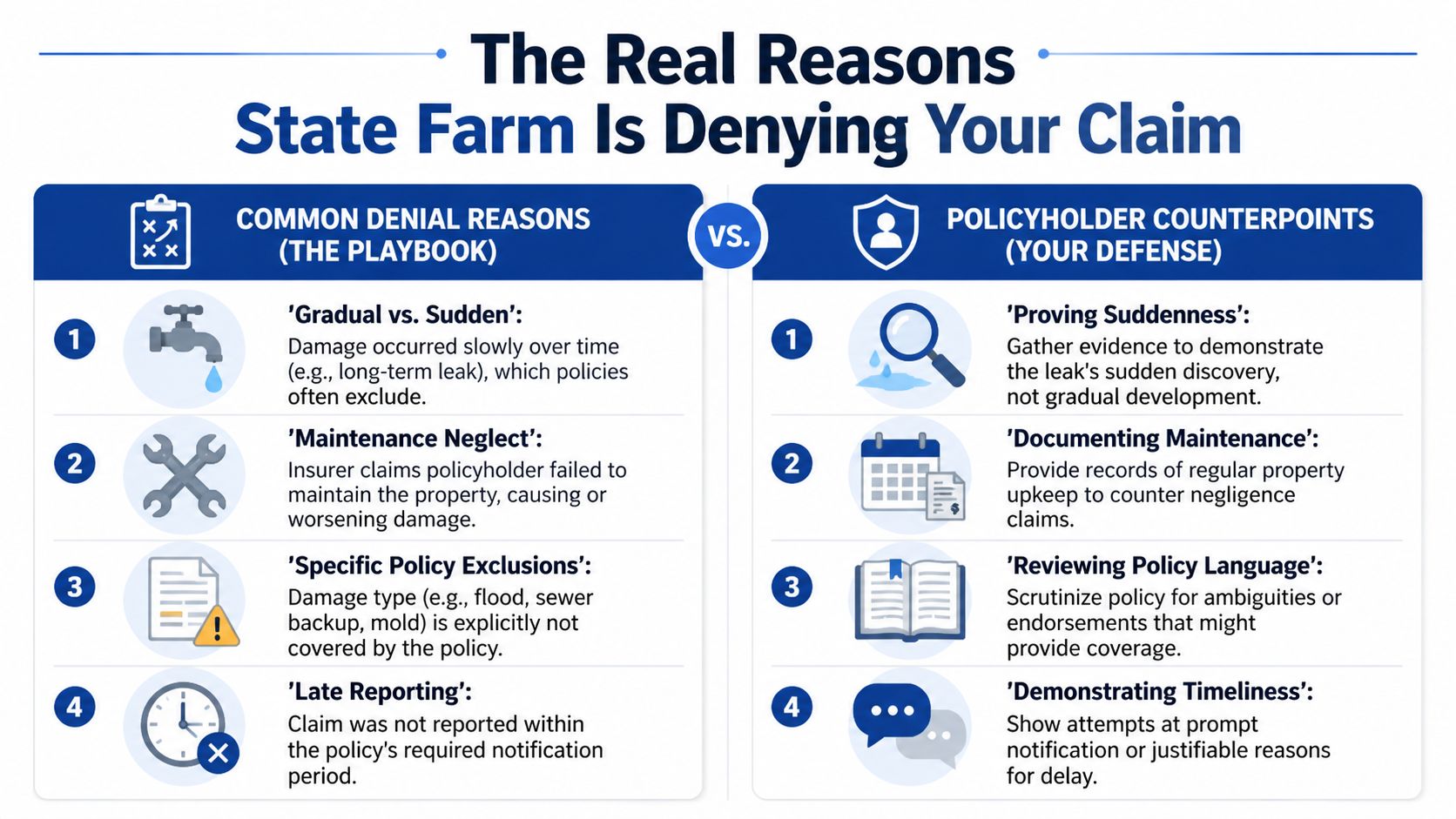

The Real Reasons State Farm Is Denying Your Claim

State Farm rarely writes, “We’re denying this because paying water losses hurts profitability.” Instead, it reaches for exclusion language that sounds technical enough to intimidate you and vague enough to cover a sloppy investigation.

That’s the playbook.

The denial language is usually broad on purpose

The most common denial themes are familiar. State Farm says the damage was caused by repeated seepage, mold or microbial growth, failure to maintain, or wear and tear. Those phrases matter because they let the company argue the loss was gradual rather than sudden, or excluded rather than covered.

That doesn’t mean the denial is right.

A failed plumbing component can show corrosion or age and still trigger a sudden escape of water. A shower line, supply line, drain line, or slab-adjacent pipe can fail abruptly even if the carrier tries to focus only on the deteriorated part. That is where many homeowners get boxed in. They start defending the old pipe instead of forcing the insurer to confront the actual water event and the resulting damage.

There is evidence this is bigger than your claim

A 2025 class-action lawsuit filed by California homeowners Ashley Hernandez and Samson Dallas Shake accuses State Farm of systematically denying thousands of water damage claims over the past decade by misapplying exclusions for water “below the surface of the ground,” according to Insurance Business reporting on the lawsuit. The suit alleges State Farm denied the plaintiffs’ claim after a failed bathroom water supply line made their home uninhabitable, and did so without inspecting the property or consulting experts like plumbers or engineers, even though their plumber said the pipe was laterally adjacent to the slab, not below it.

That allegation tracks with what many policyholders describe. The company narrows adjuster authority on water losses, pushes aggressive exclusion use, and leans on chosen experts who support denial. Public adjuster David Melzer also reported in that same coverage that approximately 75% of California water leak damage claims are denied by State Farm.

State Farm wants the debate framed around its exclusion language. You want the debate framed around causation, inspection quality, and the actual location and condition of the failed component.

There’s another reason this matters. If the carrier never hired the right professionals, never tested assumptions, or never inspected thoroughly, then the denial may rest on guesswork dressed up as policy interpretation.

What their excuses usually mean in plain English

Here’s what I tell homeowners when they show me the denial letter.

- “Repeated leakage or seepage” often means State Farm is trying to convert a sudden discovery into a long-term condition without solid proof of duration.

- “Failure to maintain” often means the company wants you to carry the blame because that’s cheaper than proving the exclusion applies.

- “Wear and tear” often gets used to deny the resulting damage by focusing on the broken part instead of the water that escaped.

- “Mold growth” is frequently used as a shortcut argument that the loss must have been old, even when water can create mold quickly.

A recent Florida appellate ruling in State Farm Florida Insurance Company v. Adele Feltes reversed a $60,000 jury award for tear-out costs based on policy exclusions for wear and tear and repeated seepage, as discussed in the background video source on State Farm’s water-loss denials. That case matters because it shows how aggressively these exclusions get litigated and how dangerous it is to assume your “obvious” water loss will be treated fairly.

Red flags that the denial may be weak

- No destructive testing: If they assumed “below slab” or hidden long-term leakage without confirming it.

- No licensed trade input: If no plumber, engineer, or qualified mitigation expert weighed in.

- No real moisture mapping: If the scope was built from a visual walk-through only.

- Shifting reasons: If the explanation changed after you pushed back.

The bottom line is simple. Many denials are not clean coverage calls. They’re pressure tactics built on incomplete facts and aggressive reading of the policy.

Your First Moves After a Claim Denial

The first two days after a denial matter more than most homeowners realize. This is when people accidentally destroy evidence, make permanent repairs too soon, or keep talking on the phone instead of locking down the record in writing.

Move like you’re preparing for trial, even if the claim resolves without one.

Protect the evidence before you protect appearances

Don’t rush to make the property look normal. Clean-looking rooms are useless if the evidence that proves your claim is gone.

Start with a hard evidence sweep:

- Photograph everything again: Get wide shots, close-ups, affected materials, baseboards, cabinets, flooring transitions, ceilings, access points, and the failed plumbing component if available.

- Take video with narration: Walk room to room and explain what happened, when you discovered it, what was wet, and what State Farm said.

- Preserve removed materials: If a plumber cuts out pipe or a contractor opens walls, save the damaged parts when possible.

- Mitigate, don’t erase: Drying, tarping, water extraction, and stopping active intrusion are smart. Cosmetic restoration before the dispute is resolved is not.

If you throw out the damaged material, patch everything, and repaint before documenting the scope, you make State Farm’s job easier.

If your water damage ties to roof failure or exterior storm entry, the same principle applies. Evidence fades fast. Homeowners dealing with roofing disputes can learn a lot from this guide on getting your roof claim approved, especially the emphasis on documentation before permanent work hides the cause.

Get the file before State Farm shapes the story

You need more than the denial letter. You need the claim file behind it.

Send a written request for:

- A certified copy of your full policy

- The adjuster’s estimate

- All photographs taken by State Farm

- Engineer, plumbing, or vendor reports

- Recorded statements, notes, and claim log entries

- The exact basis for every exclusion cited

Do this by email so there’s a timestamp. If they call you, answer if you want, but follow up by email confirming what was said. Verbal conversations are where carriers soften, dodge, and reframe. Written communication pins them down.

You should also build your own timeline. Include the date of loss discovery, who you called, when mitigation started, who inspected, when the denial arrived, and every reason they gave. If State Farm later shifts from “wear and tear” to “seepage” to “maintenance neglect,” that timeline helps expose it.

How to Build and Submit a Winning Appeal

A good appeal doesn’t rant. It dismantles the denial.

That means you match every excuse in State Farm’s letter with evidence, policy wording, expert support, and a demand for reconsideration. When policyholders take that approach, they see results. An estimated 70% of denials are overturned with rigorous appeals, and public adjusters using IICRC S500 standards, infrared thermography, psychrometric charts, and benchmark Xactimate estimates can increase payouts by 40% to 60% over an insurer’s initial low-ball offer by proving the true scope of loss, according to WDB Legal’s discussion of State Farm water claim denials.

Build the appeal around proof not outrage

Your appeal package should look professional and a little uncomfortable for State Farm to ignore. It should include a cover letter, exhibits, and a clean explanation of why the denial fails under the facts and the policy.

A basic appeal structure works like this:

- State the claim details clearly: Policy number, claim number, property address, date of loss.

- Identify the denial reasons exactly as written: Quote their language.

- Respond point by point: If they say “continuous leakage,” show why that claim lacks proof. If they say “maintenance,” attach service records or causation opinions.

- Demand written reconsideration: Ask them to reverse the denial or explain in writing why the new evidence does not change their position.

- Set a deadline: A reasonable deadline keeps the file moving.

Here’s sample language you can adapt:

I dispute State Farm’s denial of this water damage claim. The denial relies on exclusions that are unsupported by the facts, incomplete inspection findings, and an incorrect assessment of causation. Enclosed are independent findings, damage documentation, and a revised scope of loss. Please review this supplemental submission and provide a written coverage position after considering the enclosed materials.

What strong appeal evidence looks like

Most homeowners lose appeals because they send photos and opinions. You need technical support.

A serious water-damage rebuttal often includes:

- Independent plumber findings: Especially when the dispute involves a supply line, drain line, shower pan, or slab-adjacent piping.

- IICRC-based moisture documentation: Thermal imaging, moisture meter readings, mapped affected areas, and drying analysis.

- Mitigation records: Dry-out logs, equipment records, and notes showing what materials were wet and why they required removal.

- Engineer or contractor narrative: Useful when framing, subfloor, cabinetry, or concealed spaces were affected.

- A detailed estimate: Xactimate is the language insurers already know. Use it against them.

A home inventory also helps when contents were damaged. If you need a practical system for organizing affected personal property and rooms, this guide on how to simplify insurance claims gives homeowners a straightforward inventory approach that makes appeal packages cleaner and harder to pick apart.

For homeowners who want expert help assembling this kind of package, a licensed public adjuster can handle inspection, documentation, estimate preparation, and carrier communication. One example is how to appeal an insurance claim denial, which outlines what a formal property-claim challenge should contain.

Your appeal should force State Farm to answer evidence with evidence. If they can’t, their denial starts to look exactly like what it is: a weak coverage position.

Your Water Damage Claim Appeal Checklist

| Document/Evidence Type | Why It’s Crucial | Where to Get It |

|---|---|---|

| Denial letter | Identifies every reason State Farm is relying on | State Farm claim correspondence |

| Full policy and endorsements | Shows the exact wording of exclusions, exceptions, duties, and additional coverages | Request from State Farm in writing |

| Claim file materials | Reveals photos, notes, estimates, and internal basis for denial | Request from State Farm in writing |

| Photos and video of damage | Preserves visible conditions and damage spread | Homeowner, contractor, mitigation team |

| Plumbing report | Helps establish failure point and causation | Independent licensed plumber |

| Moisture mapping and mitigation records | Supports scope and hidden damage | Water mitigation company using IICRC methods |

| Repair estimate in Xactimate | Translates damage into insurer-recognized pricing and scope | Public adjuster or qualified estimator |

| Maintenance and repair records | Counters “failure to maintain” allegations | Homeowner records, service providers |

| Timeline of events | Shows prompt action and exposes inconsistent denial logic | Homeowner-prepared chronology |

| Expert affidavit or written opinion | Adds weight where causation is disputed | Engineer, specialist contractor, or other qualified expert |

Submission tips that actually help

- Package the appeal cleanly: Label exhibits. Don’t send a pile of screenshots.

- Keep the tone firm: Professional language beats anger.

- Ask specific questions: If they claim long-term leakage, ask what evidence establishes duration.

- Demand a reinspection when needed: Especially if the original inspection was visual only or missed hidden moisture.

Calling in the Pros Public Adjusters vs Attorneys

Homeowners usually wait too long to bring in help. They assume one more phone call will fix it. It usually doesn’t.

The key question isn’t whether you need help. It’s what kind.

What a public adjuster does that your carrier adjuster will not

A public adjuster works for the policyholder. That matters because State Farm’s adjuster works for State Farm. Their job is to inspect your loss, but they do it inside the carrier’s cost controls, claim culture, and preferred framing of the damage.

A public adjuster focuses on:

- Full scope documentation: Not just what’s obvious from the doorway.

- Policy application from the insured’s side: Including ambiguous language and coverage arguments the carrier won’t volunteer.

- Estimate preparation: Using the same pricing structure insurers understand, but with the actual quantity and extent of damage.

- Negotiation backed by evidence: Not casual phone chatter.

When a water loss denial turns on hidden moisture, tear-out, slab location, or whether damage was sudden versus gradual, that technical file matters as much as the policy itself.

When you need an attorney instead

An attorney becomes critical when the dispute moves beyond valuation and into legal misconduct. That can mean bad-faith exposure, lawsuit filing, statutory claims, or a carrier that refuses to engage even after strong rebuttal evidence lands on its desk.

A simple way to think about it:

| Situation | Public Adjuster | Attorney |

|---|---|---|

| Scope of damage is incomplete | Strong fit | Usually not first move |

| Denial looks factually weak | Strong fit | May be needed later |

| Carrier ignored evidence repeatedly | Useful | Often needed if stalemate persists |

| You need a lawsuit filed | Not applicable | Required |

| You need valuation and negotiation help now | Strong fit | Usually secondary at this stage |

Here’s a practical split. If State Farm denied your water claim based on a bad inspection, weak causation analysis, or low-balled scope, start with claim-building help. If the carrier doubles down after being shown it’s wrong, then legal escalation may be the next step.

A real client review matters more than marketing copy

One reason homeowners hire a public adjuster is simple. They’re exhausted and they don’t trust the insurer’s process anymore. That’s rational.

Below is a client review screenshot tied to that experience.

After you’ve seen how policyholders describe the process, it also helps to hear directly from the field about claim advocacy and what professional representation looks like in practice.

A strong public adjuster doesn’t just “help with paperwork.” They build the record that State Farm should have built before issuing the denial.

Escalating Your Fight in North Carolina and Virginia

If you’re in North Carolina or Virginia, you have advantages many homeowners never use. State Farm counts on that.

Start by understanding two separate tools. One is regulatory pressure. The other is contractual dispute pressure.

Use the insurance department the right way

A complaint to the North Carolina Department of Insurance or the Virginia Bureau of Insurance won’t replace an appeal package, and it won’t write you a check. What it can do is force a formal response, create regulatory visibility, and make it harder for the carrier to hide behind vague denials and endless delay.

Your complaint should include:

- The denial letter

- A short timeline

- A statement of what State Farm failed to do

- Key supporting documents

- A direct request for review of claim handling

In North Carolina, policyholders also have statutory language around unfair practices that can matter in how disputes are framed. The same verified legal guidance discussing appeals notes that ambiguity arguments can matter and references N.C. Gen. Stat. § 58-63-15 and appraisal under N.C. § 58-83-1 in claim disputes involving water losses. In Virginia, bad-faith exposure can implicate Va. Code § 38.2-209.

If your denial came from a burst pipe or slab leak dispute, this explanation of water damage from a burst pipe is useful because those claims often get twisted into exclusion fights that should have been straightforward.

Don’t ignore the appraisal clause

Appraisal is one of the most overlooked pressure tools in property claims. It usually applies when the fight is over the amount of loss, but it can also become relevant after coverage arguments narrow and the remaining dispute turns on scope and price.

State Farm does not like informed policyholders invoking the contract precisely.

Use appraisal carefully:

- Read the policy first: Confirm the clause language and procedure.

- Separate coverage from valuation: Appraisal won’t fix every denial, but it can break a stalemate where the actual issue is scope.

- Choose your appraiser wisely: This is not a formality. A weak appraiser wastes the opportunity.

- Keep the record clean: Your pre-appraisal documentation still matters.

Filing a complaint creates pressure from outside the claim. Invoking appraisal creates pressure from inside the policy.

Those are different tools. Use both when the facts support it.

A Denial Is a Negotiation Not a Final Answer

A State Farm denial letter feels final because it’s supposed to. That’s the tactic. The carrier wants you discouraged, rushed, and isolated. Don’t give them that advantage.

The better approach is disciplined. Preserve the evidence. Get the file. Build the rebuttal around causation, scope, and policy language. Escalate when necessary. Bring in professionals when the facts or the carrier’s behavior call for it.

Most denied water claims don’t turn on one dramatic moment. They turn on whether the homeowner can prove what State Farm ignored, misstated, or minimized. That’s why the fight is winnable.

If you’re overwhelmed, that’s normal. If you’re ready to push back, that’s the right instinct.

If State Farm denied your water damage claim on your home or business property in North Carolina or Virginia, For The Public Adjusters, Inc. offers no-cost claim reviews for policyholders who need help disputing denials, documenting loss, and negotiating for the full amount owed under the policy.