Should you consider a Public Claims Adjuster Near Me? When your home or business gets hit with serious damage, you naturally turn to your insurance company. You’ve paid your premiums on time, year after year, and you expect them to hold up their end of the deal.

But for so many property owners, that’s when the real nightmare begins. The frustrating truth is that your insurance provider is not your ally. That reality sinks in after weeks of unreturned phone calls, confusing double-talk, and a settlement offer from carriers like State Farm or Allstate that feels like an insult.

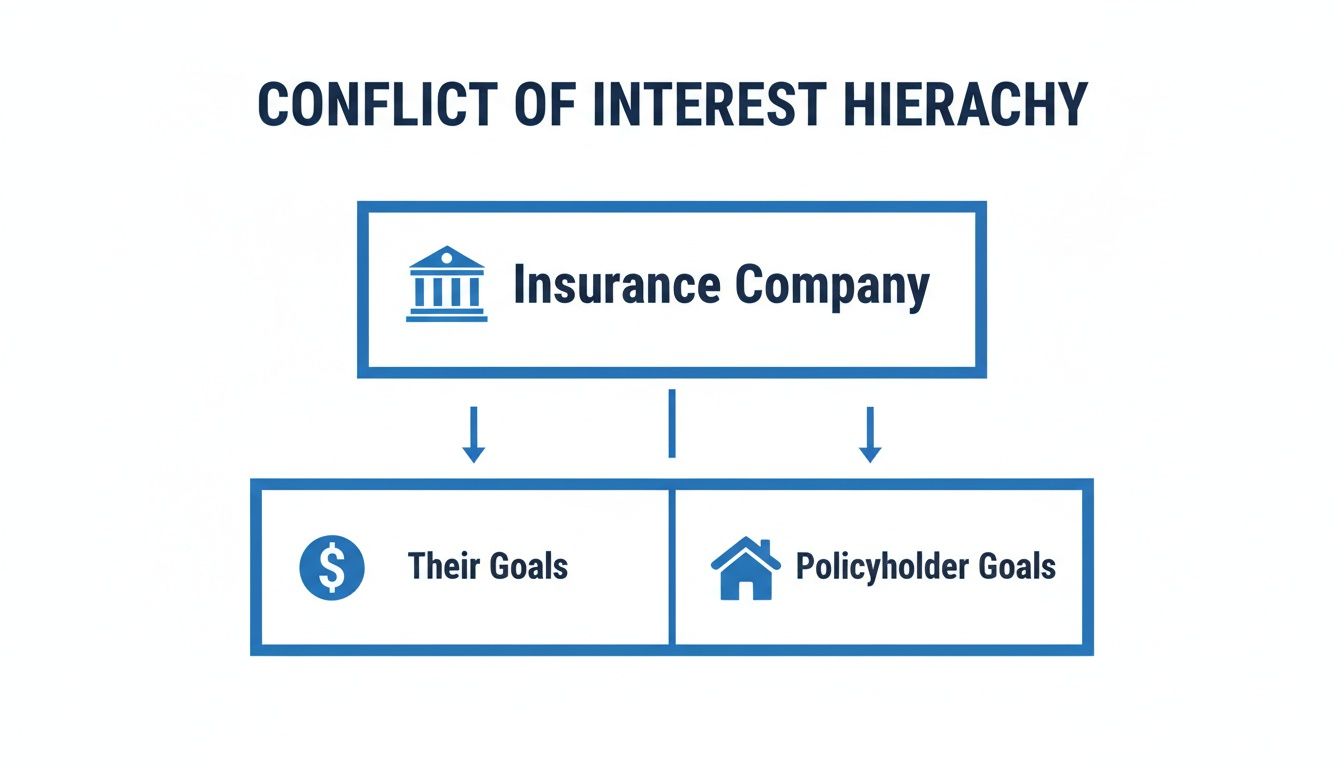

Your Insurance Company Has a Conflict of Interest

Let’s be blunt: the insurance business model is simple. They make money by collecting more in premiums than they pay out in claims. This isn’t a secret; it’s a business model that creates a massive, built-in conflict of interest right from the start.

The adjuster they send out—whether they work for State Farm, Allstate, or any other carrier—is on their payroll. Their job, their loyalty, and their performance reviews are all tied to protecting the company’s bottom line. It’s not about making you whole; it’s about minimizing the payout through delays and low-ball tactics.

This conflict of interest isn’t just theoretical. It plays out in real ways that cost homeowners and business owners dearly:

- Intentional Delays: They know that dragging out the process grinds you down. The longer you wait, the more desperate you get, and the more likely you are to accept a low-ball offer just to make it all stop.

- Low-Ball Offers: The first offer is almost always a fraction of what you’re actually owed. They’re betting you don’t know the true cost of materials and labor and will just take the money and run.

- Confusing Policy Language: Insurance policies are dense, complicated legal contracts. Carriers use that confusing wording and hidden clauses as leverage to underpay or flat-out deny your claim. To even begin to fight back, you have to know what you’re up against, which is why learning how to read your insurance policy is such a crucial first step.

An Adjuster on Your Side

The insurance company’s adjuster is trained to find ways to save their employer money. They might overlook hidden water damage, use outdated pricing for roofing materials, or “misinterpret” a section of your policy in their favor. It’s critical to get informed, and a solid guide on understanding your storm damage insurance coverage can really open your eyes to how their interests and yours are not the same.

When you’re going up against a multi-billion-dollar corporation, you need a pro in your corner who only answers to you. Searching for a “public claims adjuster near me” is the single most important thing you can do to level the playing field. A public adjuster works for you and only you, the policyholder. Our entire job is to document every last detail of your claim and force the insurance company to pay what you are rightfully owed.

What a Public Adjuster Does for You

When your home or business is hit by a catastrophic loss, you’re not just dealing with the damage—you’re thrown into a high-stakes financial fight you never signed up for. Going up against your insurance company alone is like trying to argue a complex legal case without a lawyer.

This is where a public adjuster comes in. We are your licensed, professional advocate in this fight. Our job is to represent your interests, and your interests only.

Your Dedicated Claims Expert

Think about the adjuster your insurance company sends out. They’re on the company’s payroll, and their main goal is to protect their employer’s bottom line. A public adjuster works for you. Our one and only mission is to get you the maximum and fair settlement you’re entitled to under the policy you’ve been paying for.

We step in and take the entire claims process off your shoulders. It’s an incredibly time-consuming and complicated job, but we handle every last detail to build an ironclad case for you.

This means we manage:

- A Forensic Damage Assessment: We conduct our own deep-dive inspection of your property. We find all the damage, especially the hidden issues the insurance company’s adjuster conveniently misses or flat-out ignores.

- Deep Policy Analysis: We tear apart the dense, confusing language of your insurance policy to find every single piece of coverage that can be used to pay for your recovery.

- Meticulous Claim Documentation: We build your claim from the ground up with detailed scopes of loss, precise measurements, photos, and up-to-date, market-rate estimates for every repair. We leave no room for the insurer to argue.

- Aggressive Negotiation: We become the single point of contact with your insurance company. We handle all the calls, emails, and meetings, using facts and evidence to shut down their low-ball offers and stall tactics.

It’s crucial to understand the built-in conflict of interest you’re up against from day one.

This diagram lays it out clearly: your goal is to be made whole, while your insurer’s goal is to protect its profits. Those two objectives are fundamentally at odds, and a public adjuster is the expert who levels that playing field for you.

Who Is Really Working for You? Adjuster Types Compared

It’s easy to get confused by the different types of “adjusters” involved in a claim. Let’s break it down so you know exactly who is on your side and who isn’t.

| Adjuster Type | Who They Work For | Primary Goal |

|---|---|---|

| Company Adjuster | Your Insurance Company | Minimize the payout to protect the company’s profits. |

| Independent Adjuster | The Insurance Company (as a contractor) | Minimize the payout, just like a staff adjuster. Paid by the insurer. |

| Public Adjuster | You, the Policyholder | Maximize your settlement and ensure you get a fair and full recovery. |

As you can see, only one person in this entire process has a legal and ethical duty to fight for your best interests: the public adjuster.

The claims adjusting industry is a massive business, projected to hit $10.8 billion in 2025. That growth isn’t just happening out of thin air; it’s being driven by the sheer complexity of modern insurance policies and claims.

For property owners in North Carolina and Virginia, this makes having a qualified professional on your side more critical than ever. You can learn more about the key benefits of hiring a public insurance adjuster on our blog.

How We Turn Unfair Claim Denials and Low Offers Around

Getting a denial letter or a ridiculously low settlement offer from your insurance company can feel like hitting a brick wall. Honestly, it’s a gut punch. But for us, that’s not the end of the road—it’s where our work begins. We have a battle-tested process for taking apart the weak arguments and corner-cutting inspections that carriers like State Farm and Allstate use to protect their bottom line.

The fight starts with our comprehensive, no-cost review of your claim file and the insurer’s decision letter. We meticulously go through every single line, hunting for the mistakes, omissions, and flat-out policy misinterpretations that are almost always hiding in plain sight. This initial deep dive becomes the blueprint for our entire strategy.

From there, we launch our own independent investigation. This isn’t the quick 15-minute walkthrough the company adjuster did. This is a forensic analysis.

Building an Undeniable Case for Your Recovery

Our licensed public adjusters get on-site and conduct a deep, forensic inspection of your property. We don’t just glance at the obvious damage. We bring out the heavy-duty tools—specialized moisture meters and thermal imaging cameras—to uncover the hidden water damage creeping behind your walls or the subtle smoke contamination in the attic that their adjuster somehow “missed.”

We then build your case with a mountain of undeniable proof:

- A Detailed Scope of Loss: We create an exhaustive, line-item estimate detailing the exact materials and labor costs needed to bring your property back to its pre-loss condition, all based on current market rates, not outdated numbers.

- Policy Provision Citing: We dig into your policy and pinpoint the specific language that contractually obligates your insurer to cover the very damages they denied. This leaves them zero wiggle room.

- Meticulous Documentation: We compile a bulletproof file loaded with high-resolution photos, expert reports, and every piece of paperwork required to justify every single dollar of your claim.

This methodical approach completely flips the script. You’re no longer in a position of asking them for a fair offer. Instead, we force them to defend their low-ball number against a wall of hard evidence they can’t ignore.

Your insurance company is banking on you not knowing the rules of the game. Our job is to show up as the experts who not only know every rule but also know precisely how to enforce them. We make sure your rights as a policyholder are fully protected.

Case Study: Turning a Low-Ball Offer Around

Let’s look at a real-world example. We recently worked with a homeowner in Raleigh whose finished basement flooded after a pipe burst. Their insurance company came back with a pathetic offer of $12,000, insisting that only the carpet and a few baseboards needed replacing. They completely ignored the moisture that had soaked into the drywall, the high risk of mold growth, and the cost of bringing in specialized drying equipment.

Feeling completely defeated, the homeowner searched for a “public claims adjuster near me” and gave us a call. We were on-site right away. Our inspection, using thermal cameras, revealed extensive water saturation hidden behind the walls—damage the company adjuster never looked for. We documented everything, created a brand-new scope of loss that included proper mold remediation and full reconstruction, and cited the specific policy language covering these “ensuing losses.”

After some very aggressive negotiation, we forced the insurer to reverse its decision. We secured a final settlement of $78,000 for our client. That’s more than six times their original offer. This is what we do. We fight back and we win for property owners. To learn more about what to do when your insurer refuses to play fair, check out our guide on how to handle an insurance claim dispute.

Why Experience and Licensing Are Your Biggest Weapons

Going up against a multi-billion dollar insurance company is no small feat. The adjuster they send to your home isn’t there to help you; they’re a company employee trained to find every possible reason to pay you less. Their job is to protect their employer’s bottom line, day in and day out.

To have any chance of winning, you need a seasoned pro in your corner who knows their playbook inside and out.

The Non-Negotiable: State Licensing

First things first: never, ever hire an adjuster who isn’t officially licensed by the state. In North Carolina and Virginia, a state-licensed public adjuster is the only person legally authorized to represent you in a property claim.

This license is your assurance that the adjuster has passed rigorous state exams, met strict ethical standards, and is accountable to a governing body. It’s the baseline that separates the real professionals from the storm-chasing opportunists.

Credentials That Force the Insurer’s Hand

Beyond the license, a truly elite adjuster has deep technical knowledge proven by industry certifications. When you’re dealing with something as complex as fire, smoke, or water damage, having an adjuster with credentials from the IICRC (Institute of Inspection, Cleaning and Restoration Certification) is a massive advantage.

An IICRC-certified expert doesn’t just guess what needs to be fixed. They understand the science behind the damage.

- They can pinpoint hidden moisture that will lead to mold down the road.

- They know the correct, industry-standard protocols for removing toxic smoke and soot.

- They understand exactly how to dry a structure to prevent long-term warping and rot.

This allows us to build a scope of loss that isn’t just an estimate—it’s a scientifically-backed demand. It’s hard evidence that shuts down an insurance company’s attempt to cheap out on your repairs.

Why a Long-Term Career in This Fight Matters

The insurance adjusting world has a lot of turnover. People burn out or move on. That’s why finding someone with a long, proven track record is so critical.

The U.S. Bureau of Labor Statistics projects there will be around 21,600 job openings for claims adjusters every year, mostly to replace people leaving the field. You can read more about these employment trends and what they mean. The takeaway for you? You don’t want an adjuster who is just passing through. You need a career professional who has seen it all.

When you hire For The Public Adjusters, Inc., you’re not getting a rookie. You’re getting a team of career experts who have dedicated their professional lives to mastering one thing: beating insurance companies at their own game. We’ve spent years battling carriers like Allstate and State Farm, learning their tactics, and building the strategies to defeat them. That deep well of experience is your single greatest weapon.

Navigating Claims in a World of Rising Costs and AI

Let’s be honest—the insurance claim game has changed, and not in your favor. Big insurance carriers are leaning heavily on artificial intelligence and quick, photo-only inspections to figure out what they owe you. The result? Incomplete assessments and insultingly low settlement offers that don’t come close to the real cost of putting your property back together.

These computer-generated estimates are built to miss things. They can’t smell the smoke damage hidden in your attic or detect the moisture festering behind your walls. When you stack these flawed methods against today’s soaring material prices and supply chain headaches, the first number the insurance company throws at you is almost always a joke.

Countering the Algorithm with On-Site Expertise

We fight this new reality by sticking to what actually works: thorough, boots-on-the-ground inspections. We don’t trust an algorithm to tell us the truth; we trust our own expert eyes. Our licensed adjusters get on-site and physically inspect every single inch of your property to document the full, unfiltered scope of the damage.

From there, we build a rock-solid estimate based on today’s market rates for labor and materials. This ensures your settlement reflects what it will actually cost to rebuild now, not what things cost a year ago. Understanding the real cost of residential construction needs is the only way to effectively negotiate your claim in this market.

Your insurer’s algorithm is designed to save them money. Our detailed, human-led investigation is designed to get you paid what you are rightfully owed. We know how to challenge and dismantle a computer-generated decision with undeniable physical evidence.

The insurance world is being rocked by technology and climate-driven disasters. The market for AI in claims processing exploded to $514 million in 2024 and is on track to hit $2.7 billion by 2034. This rush to automate, paired with new tariffs expected to jack up U.S. construction costs by over $3 billion, puts your claim payout directly in the crosshairs. For property owners in North Carolina and Virginia, it’s never been more critical to have a public adjuster who can fight back against automated low-ball offers with real-world proof.

When you’re searching for a “public claims adjuster near me,” you need a firm that knows how to win in this tough new environment. We combine old-school, detailed inspections with a modern understanding of exactly how to beat a computer-based denial.

A Real Review from a Homeowner We Helped

We can talk all day about our process and how we fight for policyholders, but nothing hits home like hearing from the actual people we’ve helped.

These aren’t just case files; they’re our neighbors, right here in the community, who were getting ignored and low-balled by their own insurance companies.

When you’re searching for a “public claims adjuster near me,” you need to see proof. You need to hear from people who were in your shoes—frustrated, overwhelmed, and unsure where to turn. Their stories show the real-world impact of having a genuine advocate in your corner.

Take a look at this review from James W. This client was facing a tough battle before they picked up the phone and called us.

This story is a classic example of a common insurance company tactic. Their adjuster came out, missed a huge amount of the damage, and wrote up a ridiculously low offer. It’s a strategy designed to make you just give up and take the money.

We stepped in, documented the full extent of the damage, and forced the insurance company to pay a settlement that was more than double their first offer.

That’s the difference an expert makes. It’s not just about getting a check—it’s about getting the right check. The one that actually lets you rebuild your life the right way.

Common Questions We Hear About Hiring a Public Adjuster

When you’re trying to figure out your next move after a property disaster, a few key questions always come up. If you’ve been searching online for a “public claims adjuster near me,” you deserve straight answers, not corporate-speak.

Let’s cut through the noise. Here are the most common concerns we hear from homeowners and business owners who are stuck in a fight with their insurance company.

So, How Much Does a Public Adjuster Cost?

This is almost always the first question, and for good reason. The answer is simple: we work on a contingency fee basis. That means you don’t pay us a single dime out of pocket. Ever.

Our fee is just a small, pre-agreed percentage of the final settlement we win for you. This setup puts us on the exact same team—if we don’t get you more money from the insurance company, you owe us nothing. It completely removes the financial risk from your plate, so you can get the expert help you need without worrying about another bill.

Is It Too Late to Hire You if My Claim Was Already Denied?

Absolutely not. In fact, that’s one of the main reasons people call us. A denial letter from your insurance company isn’t the end of the road; it’s just their first move.

We specialize in taking denied claims, ripping them open, and finding what the company adjuster conveniently missed. Our team launches a brand-new, independent investigation to build a powerful case that forces the insurer to re-evaluate their flimsy decision. We are experts at turning their hard “no” into the full payment you were owed all along.

Will My Insurance Company Get Mad and Punish Me for Hiring a Public Adjuster?

No. It is 100% illegal for an insurance company to cancel your policy, jack up your rates, or punish you in any way for hiring professional representation. Your policy is a legal contract, and you have every right to get help enforcing it.

Think of it this way: your insurance company has its own army of adjusters, lawyers, and experts all working to protect their bottom line. Hiring a public adjuster just levels the playing field. It sends a clear signal that you’re serious about getting paid fairly and won’t be pushed around.

Don’t let your insurance company have the final say. If you’re dealing with a denied, delayed, or low-balled claim, it’s time to fight back. Contact For The Public Adjusters, Inc. for a free, no-strings-attached claim review and let us show you what your claim is really worth. Request your free claim review online today.