The floodwater is gone, but the fight is just starting. You opened the letter expecting help and got a denial, a thin payment, or a scope of damage that barely matches what happened inside your home or building. That shock is real, and if your flood coverage is through FEMA's National Flood Insurance Program or a Write Your Own carrier, your frustration is justified.

NFIP flood claims are rigid, technical, and unforgiving. The adjuster may sound polite. The letter may look official. None of that means the number is right. If your flood insurance claim was denied, delayed, or lowballed, you need a battle plan, not generic advice. If you need a basic starting point, review this guide on claiming insurance for flood damage first, then come back ready to challenge the result.

Table of Contents

- Your Flood Insurance Claim Was Denied or Lowballed Now What

- Understanding the NFIP System and Why It Is Stacked Against You

- The 60-Day Proof of Loss Deadline The NFIP Hopes You Miss

- Building an Unbeatable Damage and Documentation Portfolio

- Decoding NFIP Excuses for Denials and Lowball Offers

- NC and VA Flood Claim FAQs

- Why You Need a Public Adjuster to Fight an NFIP Claim

- Get the Flood Claim Help You Deserve

Your Flood Insurance Claim Was Denied or Lowballed Now What

A lot of homeowners hit the same wall. The carrier sends an estimate that leaves out major materials, values contents like they were garage-sale leftovers, or rejects part of the loss with vague wording that sounds final. You read it three times and still don't know how they reached that number.

That doesn't mean the claim is over. It means the paperwork phase has turned adversarial.

What a lowball usually looks like

Sometimes the problem isn't a full denial. It's a payment that covers cleanup but not rebuild. Or it approves obvious flood damage while sidestepping hidden damage, damaged finishes, damaged built-ins, or personal property that should have been evaluated more carefully.

Common red flags include:

- A thin scope of repairs: The estimate addresses visible damage but ignores what had to be removed, detached, cleaned, or replaced.

- Depreciation hitting hard: The payment looks decent until you realize contents and some categories are being valued far below replacement cost.

- Confusing exclusions language: The letter sounds absolute, but the actual dispute may be about valuation, causation, or documentation.

- Pressure to move on: The insurer acts like the first number is reasonable because they already inspected the property.

You don't judge a flood insurance claim by how fast the carrier responds. You judge it by whether the scope and valuation match the real loss.

Your job changes after the first bad decision

At this point, stop acting like a reporter and start acting like a case builder. Every communication, every estimate, every photograph, every receipt, and every damaged-item list now matters. You're no longer just notifying the insurer. You're challenging its version of the loss.

Do three things immediately:

- Get the denial or payment letter organized. Print it, save it, highlight every reason given.

- Preserve the property record. Keep photos, videos, invoices, moisture logs, cleanup bills, and contractor observations.

- Stop assuming the insurer's adjuster caught everything. They inspected for the carrier. You need your own valuation of the damage.

A denied or underpaid flood insurance claim can be disputed. But you need discipline, speed, and better documentation than the insurer expects you to produce.

Understanding the NFIP System and Why It Is Stacked Against You

Most policyholders make the same mistake at the start. They assume a flood claim works like a standard homeowners claim. It doesn't.

Flood coverage under the National Flood Insurance Program runs on federal rules. Even when a private insurer services the policy as a Write Your Own company, that doesn't turn the claim into an ordinary private insurance dispute. The rules stay rigid.

Why this system feels so cold

The person assigned to inspect your property may seem helpful. That doesn't change who they answer to. They are not your advocate, and they are not there to build the strongest version of your claim for you.

The system is especially hard on policyholders after major storm years. FEMA's Floodsmart program states that every U.S. state and territory has had flood insurance claims since 1980, and that 2005 was the largest year for flood-related claims, driven in part by Hurricanes Katrina and Rita, according to FEMA's historical NFIP claims information and trends. When catastrophic seasons hit, claim volume surges and pressure on the system rises with it.

That matters because overloaded systems don't become more generous. They become more procedural.

Where homeowners get trapped

The NFIP claim process punishes assumptions. Policyholders often assume:

| Assumption | Reality |

|---|---|

| The adjuster will explain everything I need | You still carry the burden of getting critical claim paperwork right |

| If the damage is obvious, payment will follow | Technical noncompliance can kill an otherwise valid claim |

| A private insurer will handle this like a normal property loss | NFIP flood claims follow federal requirements and narrower coverage rules |

Practical rule: Treat every NFIP communication like it came from a bureaucracy that expects exact compliance, because that's what you're dealing with.

The conflict you need to see clearly

The carrier wants a controlled file. You need a fully documented one. Those aren't the same thing.

An NFIP flood insurance claim isn't just about proving water entered the property. It's about proving the full covered amount, in the right form, under strict rules, on time. If you don't take control of the evidence and the deadlines, the system will take control of the outcome.

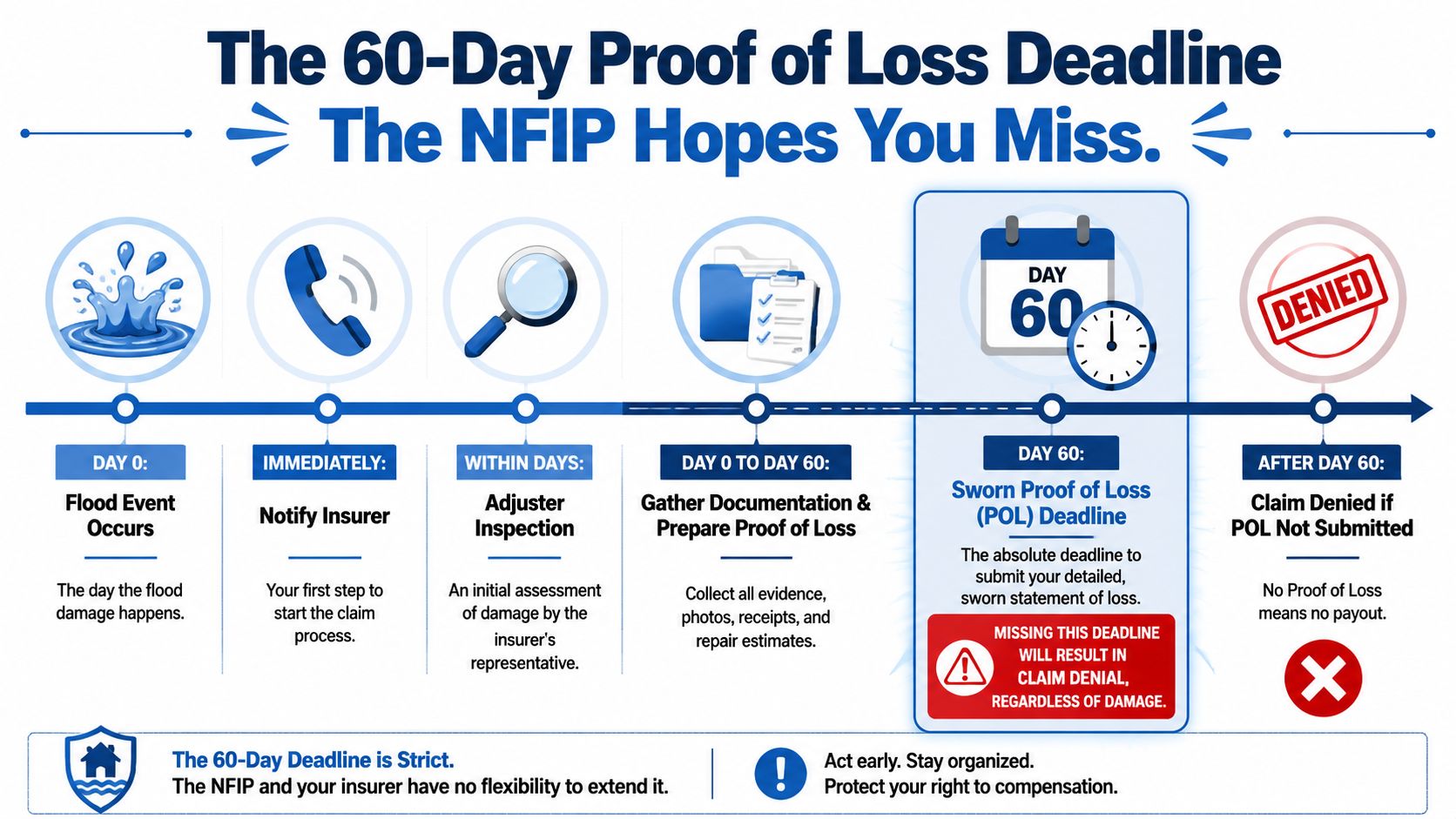

The 60-Day Proof of Loss Deadline The NFIP Hopes You Miss

You get the house gutted, the photos taken, the mold crew scheduled, and then the true hit lands. The carrier says your file is missing the one document that keeps your rights alive. That is how flood claims get buried in the NFIP system.

The Proof of Loss is a sworn statement. It is not optional paperwork, and it is not something you should assume the adjuster will handle for you. If it is late, incomplete, or wrong, you hand the carrier a clean procedural excuse to deny or underpay the claim.

What the Proof of Loss really is

This document is your sworn demand for payment under the policy. You are stating what was damaged, what it will cost, and what you expect the carrier to pay under the flood policy. Once you understand that, you stop treating it like routine claim mail and start treating it like testimony.

That is the right mindset.

If you want to see what belongs in it, review this breakdown of the sworn statement of proof of loss. Then build your claim file around supporting every line in that statement.

Homeowners get crushed here because the deadline starts running while real life is on fire. You are dealing with tear-out, temporary housing, contractor no-shows, contaminated contents, and a carrier that wants exact numbers fast. The system knows that. It still expects a sworn claim package on time.

Where the trap usually snaps shut

The first mistake is assuming notice of loss is enough. It is not.

The second mistake is trusting the adjuster's estimate as if it replaces your Proof of Loss. It does not. The adjuster works the file for the carrier. Your job is to protect your claim, not to wait for the carrier's version of your damages.

The third mistake is relying on casual reassurances. A phone call does not protect you. A vague promise does not protect you. If anyone says a waiver applies, or says more time has been granted, get that in writing and keep it in the file.

This video gives a useful visual explanation of the issue:

Your battle plan for beating the deadline

Do not wait for the carrier to organize this claim for you. Take control immediately.

Start a day-count the moment the flood loss occurs. Put the Proof of Loss deadline on your phone, your calendar, and your kitchen wall. Then work backward.

Next, gather the numbers that support the sworn amount you will claim. That means repair estimates, room-by-room damage notes, measurements, photos, videos, contents lists, invoices, and any drying or mitigation records.

Then compare your evidence to the adjuster's scope. If their estimate misses insulation, cabinets, doors, trim, built-ins, electrical components, appliances, or contaminated contents, fix that gap before the deadline passes.

Finally, submit a complete sworn Proof of Loss with documentation that supports the amount claimed, and keep proof of delivery. If the number must be supplemented later because more damage is uncovered, you are still in a stronger position when the initial filing was timely and well supported.

The valuation fight hiding inside this form

The deadline is only part of the problem. The amount you swear to matters just as much.

A rushed contents claim usually gets hit with depreciation and weak pricing support. A thin building claim gives the carrier room to say the missing items were never proven. That is how homeowners lose money twice. First on timing, then on valuation.

Here is the plain truth. The NFIP system rewards precision and punishes delay. If your Proof of Loss is sloppy, the claim survives in a damaged state. If it is missing or late, the carrier has an opening to shut the door.

Treat the 60-day Proof of Loss deadline like a legal deadline, because that is exactly what it is.

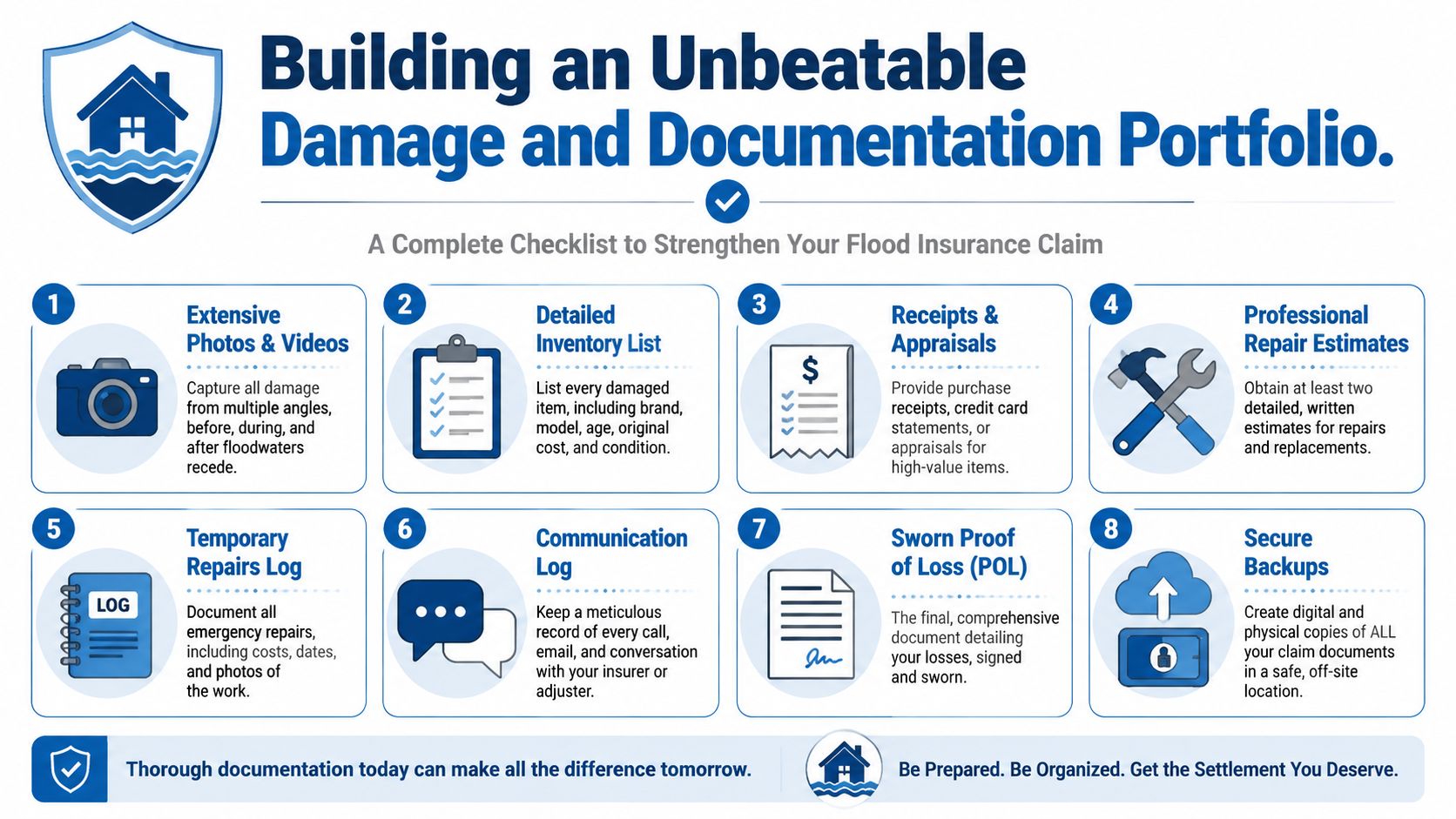

Building an Unbeatable Damage and Documentation Portfolio

The strongest flood insurance claim file looks less like a cleanup folder and more like trial prep. That's the standard you should use.

NFIP payout history shows how much flood losses can swing. The average flood claim payout was $44,401 in 2021, while it was $91,735 in 2017, according to Policygenius' compiled NFIP flood insurance statistics. That kind of volatility is exactly why weak documentation costs people money. The carrier is not going to guess high on your behalf.

Build the file before the memory fades

Start with the evidence that disappears first. Water lines fade. Debris gets hauled away. Wet materials get cut out. Once that happens, your proof gets weaker unless you captured it.

Your documentation portfolio should include:

- Wide and close photos: Shoot every room, exterior entry point, water line, flooring transition, baseboard, cabinet base, appliance contact point, and detached material.

- Video walkthroughs: Narrate what you're seeing. Open cabinets. Show swelling, staining, buckling, warping, and debris line marks.

- Itemized contents lists: Identify damaged personal property by room. Add brand, model, age, purchase details if you have them, and condition before the flood.

- Cleanup and mitigation records: Save invoices, work authorizations, drying logs, disposal records, and photos taken before removal.

- Repair estimates from independent contractors: Don't rely only on the insurer's scope.

The documents that win disputes

A lot of people collect paper. Very few build a persuasive file. The difference is structure.

Use this order:

Chronology

Create a dated timeline from the flood event through inspection, cleanup, communications, and repairs.Room-by-room evidence

Group photos, videos, notes, and estimates by area of damage instead of dumping everything into one folder.Contents support

Match damaged-item entries with receipts, credit card statements, owner photos, manuals, or appraisals where possible.Communication log

Track every call and email with the adjuster or carrier. Note date, time, person, and what was said.

If an item gets thrown away before it's documented, the carrier may treat it like it never mattered.

Don't let the insurer define the scope alone

Independent contractor estimates matter because they expose omissions. A carrier estimate may focus on what is immediately visible. A good contractor often identifies what has to be detached, reset, replaced, or rebuilt to restore the property properly.

That doesn't mean every outside estimate will control the claim. It does mean you need competing documentation if you expect to challenge a low number.

Back up everything digitally and physically. Flood claims get harder, not easier, when records go missing.

Decoding NFIP Excuses for Denials and Lowball Offers

Most denial and underpayment letters use formal language to make a judgment call sound mechanical. It isn't always mechanical. A lot of it comes down to scope, interpretation, and what the carrier thinks it can defend.

What the usual excuses really mean

Here are some common insurer positions, translated into plain English:

| Carrier language | What it often means | How to answer it |

|---|---|---|

| Damage was pre-existing | They think they can separate current flood damage from older wear or condition issues | Use before-loss photos, maintenance records, contractor observations, and flood-line evidence |

| Payment issued at ACV | They are applying depreciation to categories that don't get replacement cost treatment | Demand a clear item-by-item breakdown of depreciation and compare it to policy terms |

| Damage not caused by flood | They are disputing causation, not necessarily disputing that damage exists | Tie every damaged area to flood entry, water level, timing, and material response |

| Item not covered in basement | They are relying on location-based coverage limits | Identify the exact item, exact location, and exact policy wording being used |

ACV versus what you thought you bought

One of the ugliest surprises in a flood insurance claim is the gap between what it costs to replace something and what the NFIP pays on it. If contents are paid on an Actual Cash Value basis, depreciation can gut the number.

That doesn't mean you accept the carrier's depreciation table without question. You challenge age assumptions, condition assumptions, and omitted items. A vague depreciation figure isn't enough. The insurer should be able to show how it valued the item.

Causation fights are often evidence fights

When a carrier says damage is from settlement, prior condition, or something other than flood, the dispute usually turns on documentation. If you have flood-line photos, pre-loss condition evidence, demolition photos, drying records, and contractor statements tied to observed damage, their theory gets weaker.

Use language like this in a dispute letter:

"The inspection and estimate omitted flood-related damage that was physically present after the event, documented in photos, and confirmed during removal of affected materials."

That's stronger than writing, "I disagree."

Basement disputes need precision

Basement issues create confusion fast. Don't argue in general terms. Identify the item, the area, and the reason the carrier gave for excluding or limiting it. Then compare that to your documentation and the policy language they are relying on.

This is not the place for emotion. It's the place for exactness.

NC and VA Flood Claim FAQs

North Carolina and Virginia policyholders deal with a mix of coastal storm surge, inland flooding, intense rainfall, drainage backup conditions, and water movement that catches people off guard. That creates coverage confusion fast.

My property isn't in a high-risk flood zone. Can I still have a flood claim?

Yes, if you had flood coverage in place.

A common mistake is assuming flood claims only happen in mapped high-risk areas. FEMA training material cited by HUD says about 40% of NFIP claims come from outside Special Flood Hazard Areas, according to the HUD flood insurance and recovery training slides. For NC and VA owners, that matters because inland and localized flooding can damage homes and commercial buildings far from the coast.

If your property flooded and you carried an NFIP policy, don't let anyone dismiss the claim just because the address wasn't in the zone people talk about on the news.

What's the difference between storm water damage and flood damage?

For claim purposes, this question matters because standard homeowners insurance and NFIP flood coverage are not the same thing. A homeowner may say "storm damage" and mean wind-driven rain, roof damage, surface water intrusion, or rising floodwater. The policy language separates those causes.

If rising water affected the property from outside and on the ground, you're often in flood-claim territory. If the carrier is mixing categories or pushing the loss into the wrong bucket, get the policy language and the denial language side by side.

What if my basement claim is only partly paid?

Don't assume the insurer got it right just because they paid something. Basement-related flood disputes often come down to exactly what was damaged, where it was located, and how the item is classified under the policy.

Your response should include:

- A precise inventory: List the affected basement items individually.

- Photos tied to location: Show where each item was installed or stored.

- A written challenge to omissions: Ask the carrier to identify the policy basis for each unpaid item.

Can federal disaster help replace a bad insurance outcome?

Don't count on that. Insurance and public assistance are not interchangeable. If insurance was required and not maintained, disaster-related assistance can be restricted under the HUD guidance discussed in the background material. Handle the insurance claim seriously from the start.

Why You Need a Public Adjuster to Fight an NFIP Claim

You get the letter. Part of the damage is missing, the numbers are too low, and the insurer acts like the file is basically closed unless you can prove otherwise on their terms. That is the NFIP claim system in real life. It wears people down, especially when the flood insurer and the WYO carrier already know the rules and you are learning them under pressure.

A public adjuster changes that. You stop reacting and start building a case.

A good one works for you, not the carrier, and treats the claim like a dispute that has to be documented, priced, and argued correctly. If you want a plain-language overview, this guide on what a public adjuster does during a property claim lays out the role.

What a public adjuster actually does in a flood dispute

The right public adjuster does far more than compare your estimate to the carrier's estimate. They review the policy, the adjuster's write-up, the denial or underpayment language, the photos, and the missing items. Then they organize the file so the insurer has to answer a stronger claim presentation instead of brushing off a frustrated complaint.

That work usually includes:

- Reviewing the policy and claim correspondence: finding scope gaps, pricing errors, and weak carrier positions

- Inspecting the property independently: documenting flood damage the carrier minimized, missed, or classified the wrong way

- Preparing a damage package that can hold up under scrutiny: estimates, room-by-room details, inventories, photos, and support for disputed items

- Handling carrier communication: keeping the file on track and forcing clear responses instead of vague delay tactics

Why this matters in real life

NFIP claims are technical on purpose. The system rewards precision and punishes incomplete paperwork. Homeowners usually come into the fight angry, tired, and short on time. The carrier comes in with procedures, forms, internal reviewers, and a playbook.

That gap matters.

A public adjuster closes it by turning your side of the story into evidence, numbers, and policy-based arguments. That is how underpaid claims get taken seriously.

For policyholders in North Carolina and Virginia, For The Public Adjusters, Inc. is one example of a licensed public adjusting firm that represents homeowners and businesses in property damage claim documentation and negotiation.

The flood insurer already has trained professionals on its side. Hiring your own expert is basic claim defense.

What to look for before hiring help

Be picky. Flood claims are not the place for a generalist who "also handles water losses."

Ask direct questions:

- Have you handled NFIP and WYO flood claims before?

- Will you help build and support the Proof of Loss and the backup for it?

- How do you prove omitted building damage and disputed contents items?

- Who deals with the carrier once I sign, and how often will I get updates?

If the answers are fuzzy, walk away. In an NFIP fight, confusion costs money.

Get the Flood Claim Help You Deserve

You already know the feeling. The house flooded, the cleanup started, and then the claim process turned into a second disaster. The insurer asks for more paperwork, questions obvious damage, or sends a payment that does not come close to what it will take to repair the property. That is how NFIP fights usually start.

Treat this stage like a dispute that has to be built and pressed, not a customer service problem that will fix itself.

For The Public Adjusters, Inc. represents policyholders in North Carolina and Virginia on property damage claims. Their work includes inspection, documentation, estimating, claim review, and negotiation support for homeowners, dwelling owners, and business property claims.

Keep your next steps simple and disciplined:

- Stop reacting and start building your file. Gather the denial letter, estimate, photos, videos, contractor input, prior carrier emails, and every document tied to the loss.

- Get the claim reviewed by someone who works for you. A public adjuster can spot missing scope, weak pricing, policy misapplication, and deadline problems fast.

- Force the dispute onto paper. Verbal conversations get forgotten. Written positions, written support, and written rebuttals move a flood claim.

- Do not let the clock beat you. If the Proof of Loss issue is still alive, act immediately. Delay helps the carrier, not you.

- Prepare for pushback. NFIP and WYO flood claims often turn adversarial once you challenge the first number.

This is the part where homeowners lose momentum. They are exhausted, busy with repairs, and tired of arguing. The carrier counts on that. Do not give them that win.

If your flood claim is stuck, underpaid, delayed, or denied, call 919-400-6440 to speak with a licensed Public Insurance Adjuster, or Contact Us with your questions. A no-cost review of the damage, paperwork, and insurer position can tell you whether you have a real fight worth pressing.

WE Work For YOU. NOT Your Insurance Company.