The fire is out, but the fight is just starting. A Fire Damage Claim Adjuster in NC works for YOU!

You’re dealing with smoke, soot, contractors, temporary housing, missing belongings, and a carrier that suddenly wants everything documented down to the last burned lamp and stained shirt. Then the insurance company sends an adjuster and acts like help has arrived.

Sometimes that first call becomes the one you regret. Not because you reported the loss. Because you assumed the person on the other end was there to protect you.

The Aftermath of Fire and the First Call You’ll Regret

The day after a fire feels unreal. You walk through a house that still smells like smoke, and you’re trying to make decisions while your brain is still catching up.

Then the carrier moves fast. They assign an adjuster, ask for a recorded statement, and start talking about “the process” like it’s routine. For them, it is. For you, it’s your home or business.

The first mistake is trusting the setup

Most policyholders think the insurance adjuster is a neutral expert. That’s the trap.

The insurer’s adjuster works for the insurer. Their employer pays them. Their file notes, scope, estimate, and recommendations flow back to the company that owes you money.

That conflict matters most in fire claims because fire losses are messy. Visible burn damage is only part of the claim. Smoke gets into insulation, framing, HVAC systems, contents, attic spaces, and areas the average walk-through never captures.

Practical rule: If the insurance company controls the first inspection, the first estimate, and the first narrative of your loss, they control the claim unless you push back.

Why taking a passive approach is dangerous

North Carolina homeowners already face serious residential fire risk. In 2023, the state reported 6.1 deaths and 24.6 injuries per 1,000 residential structure fires, both above the national averages, and nationally about one in 430 insured homes files a property damage claim related to fire and lightning, according to the U.S. Fire Administration’s North Carolina fire statistics.

That doesn’t just tell you fires happen. It tells you fire claims happen often enough that carriers have a system for handling them, and that system is built around controlling cost.

What this looks like in real life

A homeowner sees blackened drywall in one room and assumes that’s the loss. The company adjuster writes for demolition, paint, some cleaning, maybe a few contents.

Months later, the smell is still there. The HVAC keeps circulating residue. Cabinets, porous materials, and hidden cavities still carry contamination. By then, the insurer is already treating the first estimate as the baseline.

That’s how underpayment starts. Not with some dramatic denial letter. With an incomplete first inspection.

If you’ve also had water used to put out the fire, secondary damage becomes another fight. Moisture behind walls and under flooring can become a separate problem fast. That’s why homeowners dealing with damp post-loss conditions should also understand practical prevention steps like how to prevent mold in your basement while the larger claim dispute is unfolding.

What you should do instead

Don’t hand over control because the insurer sounds organized.

Do this early:

- Slow the conversation down: Don’t guess at damage totals, repair methods, or contents values on the first call.

- Photograph everything: Wide shots, close-ups, contents, HVAC vents, cabinets, attic access points, insulation, and every room.

- Keep your own paper trail: Every email, estimate, hotel bill, emergency service invoice, and temporary repair receipt matters.

- Treat the claim like a negotiation: Because that’s exactly what it is.

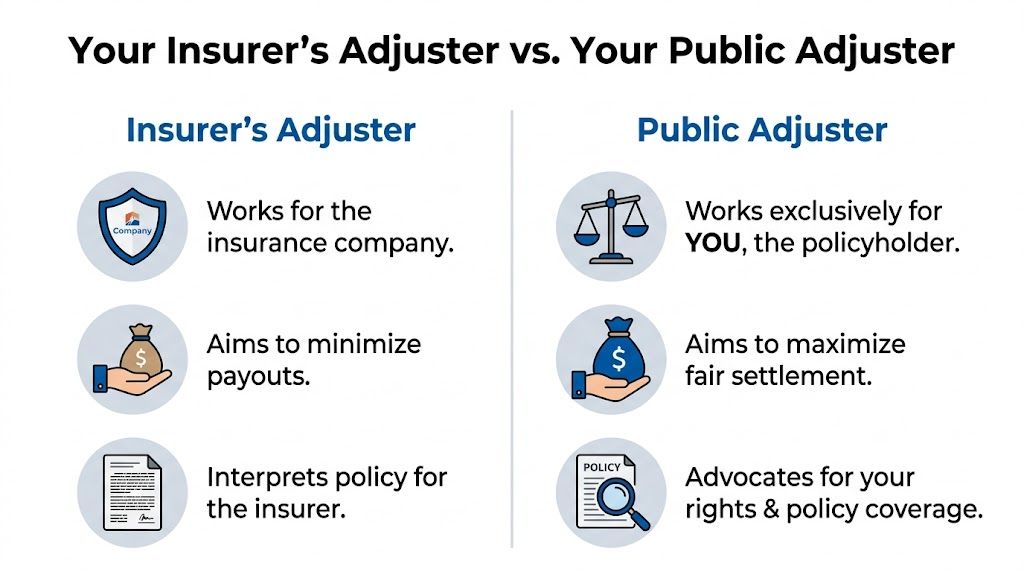

Your Insurer’s Adjuster vs Your Public Adjuster

People get confused by the title “adjuster.” They assume both adjusters do roughly the same job.

They don’t.

One works for the company paying the claim. The other works for the policyholder trying to get fully paid. That difference controls everything.

Who each adjuster actually serves

If the carrier has already assigned someone to your fire loss, that person is there to inspect, evaluate, and report for the insurer.

A public adjuster is your expert. They inspect for you, document for you, interpret the policy for your side, and negotiate against the carrier’s position.

If you want a basic overview of the role, this breakdown of what does a public adjuster do is useful. The short version is simple. The public adjuster represents the insured, not the carrier.

Public Adjuster vs. Insurance Company Adjuster Who is on Your Side

| Attribute | Public Adjuster (Your Advocate) | Insurance Company Adjuster (Their Employee) |

|---|---|---|

| Who hires them | You, the policyholder | The insurance company |

| Who they answer to | You | Their employer |

| Primary objective | Maximize the fair settlement supported by the policy and evidence | Control claim cost for the insurer |

| Policy interpretation | Looks for available benefits, extensions, and overlooked coverage | Interprets policy from the carrier’s claim position |

| Damage inspection style | Detailed, room-by-room, scope-driven | Often narrower and budget-driven |

| Negotiation role | Pushes for full valuation | Defends the company estimate |

| Best for | Disputed, delayed, denied, or low-balled property claims | Processing claims for the insurer |

The conflict isn’t subtle

A lot of homeowners want to believe the company adjuster is at least partly on their side. That belief costs people money.

The insurer doesn’t send an adjuster because they want your claim as high as possible. They send an adjuster because they need a number they can defend internally. If that number comes in low, you’re the one left trying to close the gap.

The insurance company has its expert from day one. You should have yours.

Fire claims make the gap even worse

Fire losses aren’t simple drywall and paint claims. They involve structure, smoke migration, contents valuation, code issues, cleanup scope, and sometimes business interruption or additional living expenses.

That means the person controlling the scope has enormous influence.

Here’s how that usually plays out:

- On smoke damage: The insurer’s adjuster may focus on visible residue. Your adjuster looks at hidden spread, odor retention, and whether materials can be restored.

- On rebuilding costs: The insurer may price to a stripped-down scope. Your adjuster prices what it takes to repair properly and comply with the policy.

- On contents: The insurer may accept broad categories. Your adjuster pushes for itemized, supportable replacement values.

- On communication: The insurer creates deadlines for you. Your adjuster creates deadlines for them.

My advice

If your loss is more than minor, stop treating the company adjuster like a shared resource. They aren’t.

Treat them like the insurer’s field representative, because that’s what they are. Then decide whether you want to face a professional claim operation alone or level the field with your own expert.

How a Public Adjuster Dismantles a Low-Ball Fire Claim

You open the insurer’s estimate and your stomach drops. Rooms are missing. Smoke damage is priced like a basic cleaning job. Contents are grouped into broad categories that slash value before substantive negotiation begins.

That is the moment many homeowners realize they are not in a customer service process. They are in a claim fight.

A public adjuster wins that fight by rebuilding the file the insurance company should have built in the first place, then forcing the carrier to respond to facts, policy language, and itemized costs instead of shortcuts.

The first move is a new inspection

Do not waste your best energy arguing over a weak estimate that was built on a weak inspection.

A public adjuster starts by inspecting the loss again, room by room and system by system. The goal is simple. Find every missed item, every under-scoped repair, and every place the carrier treated contamination like a cosmetic issue. Fire claims are full of these pressure points because smoke travels, soot settles in hidden areas, and odor stays trapped in porous materials long after the visible damage is cleaned.

A serious inspection looks beyond burned surfaces. It tracks what happened inside the HVAC system, behind finished walls, inside insulation, around electrical components, and across contents that may look salvageable but are not fit to remain in the home.

The claim gets rebuilt from scratch

A public adjuster is not there to complain. A public adjuster is there to assemble a stronger claim file than the carrier’s.

That file usually includes:

- A line-by-line structural estimate: demolition, cleaning, sealing, replacement, code-related work, and repairs the carrier skipped or underpriced

- A contents schedule: item descriptions, quantity, age if relevant, condition, and support for replacement cost

- Technical support where the claim needs it: contractor input, hygienist findings, engineering opinions, or specialty evaluations

- Policy-based arguments: coverage language tied to each disputed item, not vague appeals to fairness

- Expense tracking: temporary housing, emergency mitigation, debris removal, permits, and other covered costs that often get shaved down

This is how low offers get exposed. The insurer has to answer specifics.

Hidden damage is where underpayments break apart

Insurance company estimates often look clean because they avoid the expensive parts of the loss. That is not an accident. If the carrier labels a contaminated material as cleanable instead of replaceable, the number drops fast. If the carrier ignores ductwork, cavity contamination, or damaged electrical components, the number drops again.

That is why experienced public adjusters push hard on hidden damage.

| Area | What carriers often miss | Why it matters |

|---|---|---|

| HVAC system | Smoke and soot inside ducts, returns, and mechanical components | Residue can keep circulating through the property |

| Insulation | Embedded odor and contamination in porous materials | Surface treatment does not remove trapped smoke |

| Wall cavities | Residue behind drywall and trim assemblies | Incomplete remediation leads to recurring odor and rework |

| Electrical components | Heat exposure, soot, and corrosion risk | Safety problems can remain after cosmetic repairs |

If the estimate does not explain these areas clearly, the carrier has left itself room to underpay you.

Good adjusters control the paper trail

Insurance companies do not just win with low numbers. They win with documentation gaps, vague notes, and a file that makes their position look reasonable.

A public adjuster closes those gaps and creates pressure in writing. Every omitted room, missing line item, unsupported depreciation decision, and below-market price gets challenged with a documented response. Every disagreement gets tied back to the policy. Every delay gets tracked.

That paper trail matters because disputed claims drag out. If you want a sense of how carriers stretch these files, review this breakdown of how long an insurance claim can take. Delay is not just frustrating. Delay gives the insurer more chances to wear down an exhausted homeowner.

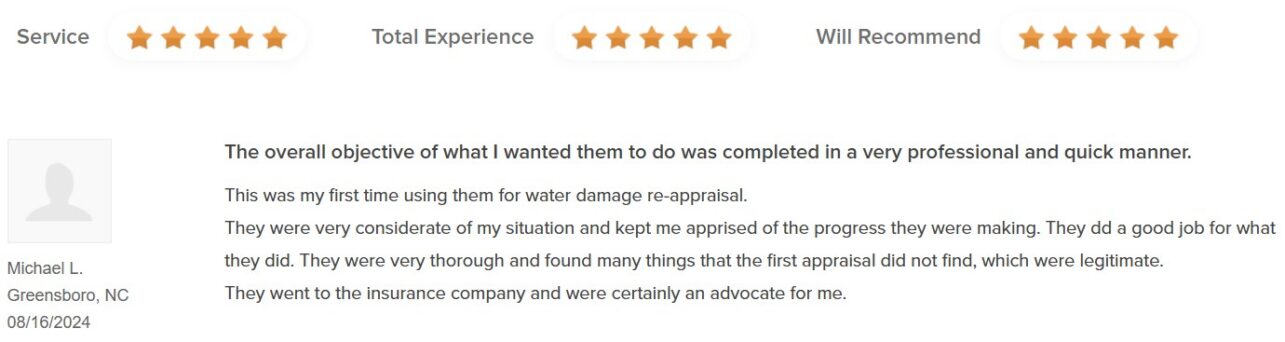

Reviews matter only if they show real claim work

Look at reviews with a hard eye. Praise about friendliness is fine, but it does not tell you whether the adjuster can take apart a weak fire estimate.

A customer review on Customer Lobby for For The Public Adjusters, Inc. describes the firm as very professional, considerate, thorough, and an advocate in dealing with the insurance company during a difficult property claim. That is the kind of feedback worth paying attention to. Fire claims punish shallow work and reward detailed claim preparation.

Later in the process, seeing how this dispute plays out can help you understand what’s happening on the carrier side:

The pressure points that force movement

Once the evidence is organized, the insurer loses the easy excuses.

The strongest public adjusters do four things well:

-

They replace the carrier’s version of the loss

A limited scope gets answered with a fuller, documented scope tied to real repair needs. -

They force line-by-line accountability

Broad denials are easy. Responding to a detailed estimate is harder. -

They anchor every dispute to coverage

Policy language moves claims. Complaints alone do not. -

They document the cost of delay and underpayment

Housing costs, emergency work, storage, debris handling, and code issues add up fast. If they are not documented and pressed, they get ignored or reduced.

Make the insurance company explain every omission in writing. That changes the balance of power fast.

Low-ball fire claims do not fall apart because the homeowner gets angry. They fall apart because someone with experience builds a stronger file, attacks the weak assumptions, and refuses to let the carrier control the story.

Navigating the Disputed Claim Timeline Step-by-Step

A disputed fire claim has its own rhythm. Once you reject a weak estimate or challenge an underpayment, the file changes from routine processing to controlled conflict.

You need a timeline. Not the carrier’s version. Yours.

Phase one re-inspection and evidence

The most important window often opens during the insurer investigation and inspection phase, typically weeks 2-6 post-claim, when documentation quality directly shapes the outcome. Benchmark data also shows homeowners who request second appraisals and formal appeals increase payouts by approximately 20%, according to this breakdown of the fire damage insurance claim process and dispute timeline.

That means early dispute work matters. A lot.

The first phase is not about sending angry emails. It’s about assembling a file the carrier has to take seriously.

What gets gathered first

- Property inspection records: Photos, videos, contractor observations, specialty reports.

- Contents support: Inventory lists, model information when available, proof of ownership where possible.

- All extra expenses: Hotel stays, rentals, meals if covered, emergency mitigation, board-up, debris, permits.

- Carrier file gaps: Missing rooms, skipped systems, omitted code items, unsupported depreciation, and pricing issues.

Phase two the demand package

Once the evidence is organized, your side submits a new estimate and supporting documents.

This package should be tight. It should tell a coherent story and support the number. It should also expose where the insurer’s estimate falls short.

A solid demand package usually does three things:

| Demand element | Why it matters |

|---|---|

| Detailed scope | Forces the carrier to address specifics instead of hiding behind generalities |

| Policy references | Anchors the dispute in contract rights, not emotion |

| Supporting invoices and expert input | Makes the claim harder to dismiss as opinion |

Phase three negotiation under pressure

Now the negotiation starts for real.

Many policyholders get worn down at this stage. The carrier may ask for more paperwork, re-open settled points, or act like your revised estimate is somehow unreasonable because it’s higher.

That doesn’t mean you’re losing. It usually means they’ve realized the original number won’t survive scrutiny.

A disputed claim moves faster when your documentation is cleaner than the insurer’s excuses.

If you want a broader sense of timing issues, delays, and what can slow or move a claim, this article on how long insurance claim take adds useful context.

Phase four appraisal if needed

If negotiations stall, the policy may allow Appraisal. That’s a contract tool many homeowners never use because nobody explains it clearly.

Appraisal is generally about the amount of loss, not broad legal coverage questions. Each side selects an appraiser, and those appraisers work with an umpire if needed.

It’s not the right move in every file. But in the right dispute, it can break a deadlock that the carrier was happy to drag out.

When appraisal may make sense

- The insurer admits some coverage but disputes value

- The fight centers on repair scope or pricing

- You already have a strong, documented estimate

- The carrier keeps delaying without resolving numbers

Phase five supplements and unresolved damage

A fire claim can keep evolving. Odor issues, concealed contamination, code problems, or additional tear-out needs may appear later.

That’s why a disputed claim isn’t always one estimate and one settlement check. It can involve supplements, revised scopes, and continued negotiation after the first payment.

The policyholder who treats the file like it ended too soon usually loses money. The one who keeps documenting and pushing usually has more advantage.

Unmasking Insurer Delay and Deny Tactics in NC & VA

You call the carrier after a fire, expect help, and get a process designed to control the claim before you understand what was lost.

That is the part many homeowners miss. A fire claim is not a customer service exercise. It is an adversarial negotiation. The insurer’s job is to protect the company’s money. Your job is to protect your property, your health, and the full value of the claim.

The common playbook

In North Carolina and Virginia, the tactics are usually predictable. They just arrive dressed up as routine claim handling.

Endless information requests

The carrier asks for photos, then receipts, then contractor bids, then a recorded statement, then more documents they could have requested at the start. Some of this is reasonable. A lot of it is delay with a paper trail.

Counter-move: answer legitimate requests promptly, keep every response in writing, and ask the adjuster to list every remaining item needed to make a coverage and payment decision.

Blaming non-covered conditions

A fire loss suddenly becomes a debate over wear and tear, old staining, deferred maintenance, or prior defects. That shift is intentional. If the carrier can mix pre-existing issues into the file, it gets easier to shrink the scope and harder for you to prove what the fire caused.

Counter-move: pin the claim to causation. Use photos, expert inspections, contractor notes, and room-by-room documentation that separates old issues from fire, smoke, soot, and suppression damage.

Low-ball estimating

This is one of the oldest tricks in the book. The estimate leaves out demolition, odor treatment, code upgrades, specialty cleaning, detached structures, contents handling, or proper finish matching. The total looks official, so homeowners assume it must be close.

It usually is not.

Counter-move: answer line item by line item. Replace the carrier estimate with one built on the actual damage, not the insurer’s preferred version of it.

If that pattern sounds familiar, review these reasons insurance companies deny fire claims and compare them against what is happening in your file.

The smoke damage fight most carriers want to avoid

Smoke claims are expensive when handled correctly. That is exactly why insurers push so hard to keep them small.

The usual move is simple. Call it light cleaning. Ignore odor migration. Skip testing. Pretend residue stayed in one room. Overlook what moved through the HVAC system. Treat porous materials like they can always be saved. That approach protects the carrier, not the property.

Smoke is not just dirt on a wall. It can affect insulation, cabinetry, soft goods, electronics, framing cavities, ductwork, and indoor air quality. If the insurer decides the house only needs wiping and paint, challenge that conclusion immediately and ask what inspection, testing, or technical basis supports it.

What carriers often ignore in smoke disputes

- Air quality concerns: If no one evaluates particulates or combustion byproducts, the carrier can frame the problem as cosmetic.

- Porous materials: Smoke and odor absorb into materials that cannot always be cleaned back to a pre-loss condition.

- HVAC contamination: A system that circulated smoke can keep spreading residue and odor after the fire is out.

- Health-based remediation needs: Carriers often resist these costs even when the fire loss created the condition.

One question cuts through a lot of nonsense: What testing or inspection did you rely on before deciding cleaning was enough?

Partial payment can be a denial strategy

Many bad fire claims never receive a clean, formal denial letter. The insurer pays part of the loss, drags out the rest, disputes obvious scope, and waits to see if the policyholder gives up.

That is still a denial tactic.

A small check can do real damage if it locks the conversation around the wrong number. Once the carrier sets an artificially low baseline, every later discussion starts from a weaker position unless someone challenges it with evidence and pressure.

Treat delay, silence, repeated reinspection, and unexplained underpayment as warning signs. In a fire claim, you are either strengthening your position or weakening it.

How to Choose a Public Adjuster in North Carolina and Virginia

The wrong public adjuster can cost you almost as much as the wrong insurance adjuster.

After a fire, plenty of homeowners are tired, displaced, and desperate for someone to take over. That is exactly when bad adjusters, sloppy contracts, and weak claim handling do the most damage. You are not hiring a friendly helper. You are hiring a representative for a financial dispute against a company that already has a strategy, a playbook, and a number it wants you to accept.

Start with one rule. Verify everything yourself.

What to check before you sign anything

A license matters, but it is only the starting point. You need someone who can build, value, and fight a fire claim under pressure.

Use this checklist.

- Confirm the state license: Check North Carolina or Virginia records yourself. Do not rely on a business card, a website, or a verbal claim.

- Ask how many fire claims they personally handle: Fire losses involve smoke spread, demolition scope, cleaning limits, code upgrades, contents valuation, and hidden damage. General property experience is not enough.

- Read the fee agreement line by line: A contingency fee should be clear, written plainly, and easy to understand. If the contract is confusing, one-sided, or packed with vague language, walk away.

- Find out who will run your file: Some firms send a strong salesperson, then hand the claim to someone you never met. Ask who inspects, who writes the estimate, who inventories contents, and who negotiates with the carrier.

- Ask how they document the loss: You want a method. Photos, room-by-room scope, contents support, contractor input, policy review, and supplemental handling should all be part of the answer.

- Check local experience in NC and VA: Carrier behavior, pricing disputes, code enforcement, and claim friction vary by market. Local claim history matters.

Questions that expose weak adjusters fast

Skip the soft questions. Ask the ones that force a real answer.

| Ask this | Why it matters |

|---|---|

| How do you prove smoke damage that the carrier calls cosmetic? | You need evidence strategy, not opinions |

| Who prepares the building estimate and contents valuation? | Weak files often come from outsourced or generic estimating |

| How do you handle supplemental damage found after teardown or cleaning attempts? | Fire claims often grow once the work begins |

| What do you do when the insurer delays inspections, changes adjusters, or ignores documentation? | Delay is a common pressure tactic, and your adjuster needs a response plan |

| How often will I hear from you, and who calls me back? | Poor communication usually signals poor file management |

A good adjuster answers directly. A bad one talks in circles, sells reassurance, and avoids specifics.

Watch how they talk about the insurance company

This part matters more than homeowners realize.

If an adjuster talks like the claim process is just paperwork and polite follow-up, keep looking. Fire claims are disputed on scope, price, cause, cleaning, replacement, code, depreciation, contents, and business interruption. The carrier may act cooperative while cutting value at every stage. Your adjuster should understand that from day one and explain how they handle it.

You want someone who treats the file like a case that has to be proven. Because that is what it is.

A factual example to compare against

For The Public Adjusters, Inc. is a state-licensed public adjusting firm serving North Carolina and Virginia that handles property claim assessment, documentation, and negotiation for homeowners and businesses, including fire and smoke losses.

Use that as a comparison point, not a shortcut. Put every firm through the same test.

Red flags that should end the conversation

- They promise a specific payout before reviewing the file

- They pressure you to sign on the first call or first visit

- They cannot explain their inspection and estimating process

- They speak vaguely about smoke, odor, and hidden contamination

- They avoid policy language or dismiss coverage questions

- They make themselves hard to reach before you even hire them

Hire the adjuster who can prove value, document damage, and push back when the carrier starts trimming the claim. Personality matters far less than discipline.

Your Fire Damage Claim Questions Answered

Will hiring a public adjuster slow down my claim

Usually, no. The low-ball estimate and the insurer’s resistance are what slow the claim down.

A public adjuster may add work at the front end because the file gets documented properly. That’s a good delay, if you even want to call it that. Slowing down long enough to avoid a bad settlement is smarter than rushing into one.

Fast and underpaid is not a win.

How does a public adjuster get paid

Most legitimate public adjusters work on a contingency fee. That means they’re paid from the claim recovery according to the contract, not through a big upfront bill.

Ask for the fee in writing. Read the agreement. If someone wants substantial money before they’ve done the job, be careful.

Is it too late if I already got a check

Not always.

A first payment is often just that. A first payment. Fire claims can involve supplemental damage, omitted scope, hidden smoke contamination, code issues, or contents that weren’t valued correctly the first time.

What matters is the wording around the payment and whether you signed anything that released the insurer from further obligation. Get that reviewed before assuming the claim is over.

What if the insurer says the damage is only cosmetic

That’s common in smoke-heavy files.

The answer isn’t to argue in circles. The answer is to inspect deeper, document more, and test when needed. Fire damage often extends beyond what’s obvious on painted surfaces.

Can a public adjuster help if my claim was denied

Often, yes.

A denial is not always the final word. Sometimes the carrier denied because the claim was poorly documented, the cause was disputed, or the scope submitted didn’t match the actual loss. A public adjuster can review the denial position, inspect independently, and build a stronger response.

Do I need one for a business property fire claim too

Yes, if the loss is meaningful or the carrier is fighting scope, contents, cleanup, or income-related issues.

Commercial fire claims usually involve more moving parts than residential claims. More categories. More documents. More room for the carrier to underpay.

Don’t Fight Your Insurance Company Alone

A fire damage claim isn’t a customer service event. It’s a negotiation with a company that has money on the line and professionals trained to protect it.

If your insurer has low-balled, delayed, narrowed the scope, or started acting like your fire loss is your burden to prove from scratch, get help. A fire damage claim adjuster can change the influence, the documentation, and the outcome.

You don’t get points for handling a bad claim alone. You get paid by handling it correctly.

If you’re dealing with a disputed fire loss, contact For The Public Adjusters, Inc. for a no-cost, no-obligation review of your claim. A licensed public adjuster can review the estimate, inspect for missed damage, explain your coverage issues, and help you decide how to push back against a low offer, delay, or denial.