INDEPENDENT WEBSITE, TOP RATED LOCAL, RECOMMENDS FOR THE PUBLIC ADJUSTERS AS “BEST PUBLIC ADJUSTER NEAR ME!”

For The Public adjusters, Inc. of NC receives highest Public Adjuster Ratings for Public Adjuster Reviews from Top Rated Local.

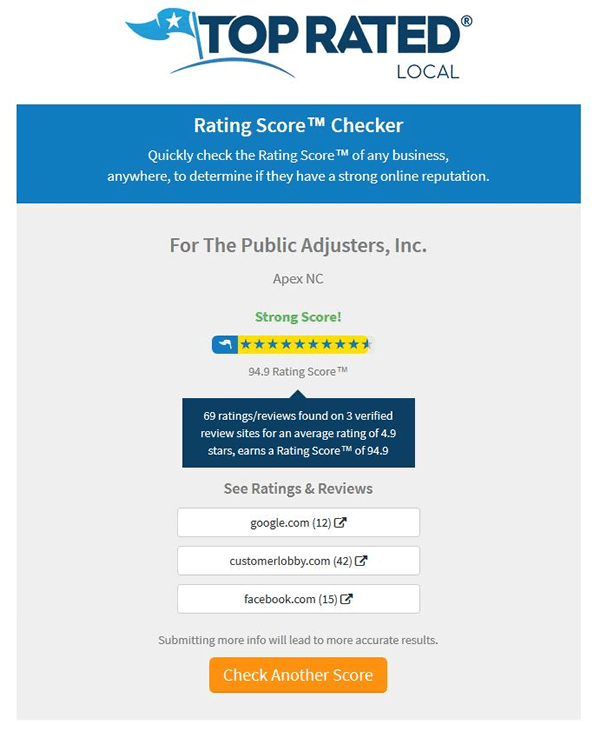

A search conducted through Top Rated Local’s Score Checker shows For The Public adjusters, Inc. of NC has an overall average Review Rating of 4.9%. This average is very high considering the average is from a whopping 69 online reviews (at the time of the review conducted in Jan 2018).

The Score Checker produces an overall score for the business based on how many online reviews it has (in this case public adjuster reviews) and the average of those reviews.

Top Rated Local gives For The Public Adjusters, Inc. an overall Online Reputation Score of 94.9%

When disaster strikes your home or business in North Carolina or Virginia, you expect the insurance company you’ve paid for years to be your ally. The harsh reality, however, is often a frustrating battle against delays, denials, and shockingly low settlement offers. Large carriers like State Farm and Allstate employ their own adjusters, whose primary loyalty is to the company’s bottom line, not to your complete and fair recovery. This fundamental conflict of interest puts you at a severe disadvantage, especially when you are navigating the stress of property damage from fire, water, wind, or a major storm.

This guide is built for policyholders who are tired of being stonewalled and are ready to fight back. We will cut through the noise and provide a comprehensive roundup of the 7 best resources and platforms to find the best public adjuster near me. A public adjuster is a state-licensed professional who works exclusively for you, the policyholder. Their job is to meticulously document your loss, build an ironclad claim, and negotiate aggressively on your behalf to secure the maximum settlement you are entitled to under your policy.

Think of them as your personal advocate in the fight against a difficult insurance carrier. In this detailed listicle, we will explore each resource, complete with direct links and practical advice on how to use them effectively. We will show you precisely where to look and what to look for, so you can find a qualified expert who can level the playing field and ensure you get the funds needed to rebuild properly.

1. For The Public Adjusters, Inc. – Top Rated Public Adjuster Near Me

When your property suffers significant damage from a fire, hurricane, or major water loss, the last thing you need is a battle with your insurance carrier. Carriers like State Farm or Allstate often protect their bottom line by delaying, denying, or underpaying legitimate claims, leaving you under-resourced and overwhelmed. This is precisely the scenario where

For The Public Adjusters, Inc. (FTPA) establishes itself as an essential ally for homeowners and business owners across North Carolina and Virginia,

Top Rated Local says, “…making it our top choice for the best public adjuster near me.”

FTPA operates on a simple yet powerful premise: they work exclusively for you, the policyholder, never for the insurance company. This commitment eliminates the inherent conflict of interest that exists when the carrier’s adjuster, whose loyalty is to their employer, is the one determining the value of your loss. Their state-licensed adjusters step in to level the playing field, providing the expert representation needed to document, estimate, and negotiate your claim for its full and fair value.

Key Strengths and Certified Expertise

What truly distinguishes FTPA is its combination of certified expertise and a comprehensive, policyholder-centric service model. They bring a level of technical proficiency that most policyholders simply don’t have, which is critical when challenging an insurer’s lowball offer.

- IICRC-Certified Adjusters: For fire, smoke, and water damage claims, their adjusters hold certifications from the Institute of Inspection, Cleaning and Restoration Certification (IICRC). This means they understand the industry-standard protocols for remediation and restoration, enabling them to build meticulously detailed and defensible repair estimates that insurance companies cannot easily dismiss.

- NFIP/FEMA Flood Claim Specialists: Navigating a flood claim through the National Flood Insurance Program (NFIP) is notoriously complex and frustrating. These claims are handled not by your homeowner’s insurance carrier, but by FEMA-backed entities like the NFIP or a Write-Your-Own (WYO) company, which are known for being incredibly difficult. FTPA possesses specialized expertise in this area, helping policyholders in North Carolina and Virginia manage the stringent documentation requirements and fight back against the difficult adjusters from NFIP or WYO carriers.

- Proven Track Record: Client testimonials and case studies repeatedly highlight FTPA’s ability to achieve significant financial victories. For example, a business owner in Raleigh saw their initial fire damage offer of $150,000 from their insurer increase to over $500,000 after FTPA took over the claim, meticulously documenting business interruption and hidden structural damage the company adjuster ignored.

The FTPA Process: An End-to-End Advocacy Model

Engaging with FTPA means you are not just hiring an estimator; you are gaining a dedicated partner for the entire claims process. Their service is designed to take the burden off your shoulders from start to finish.

- Free Claim Review & Consultation: They begin with a no-cost, no-obligation review of your insurance policy and the damage to your property. This initial step helps determine the viability of your claim and provides you with a clear understanding of your options.

- Detailed Damage Assessment: FTPA conducts its own exhaustive inspection, using advanced tools and methodologies to uncover all damage, including hidden issues that a carrier’s adjuster might overlook.

- Comprehensive Documentation: They prepare a professional claim package, which includes a detailed scope of work, precise cost estimates using industry-standard software, a complete contents inventory for personal or business property, and evidence to support business interruption losses.

- Direct Carrier Negotiation: Armed with indisputable evidence, their team communicates and negotiates directly with the insurance company on your behalf. They manage all correspondence, attend all meetings, and strategically counter any attempts to underpay or deny the claim.

Key Insight: The power of a public adjuster like FTPA lies in their ability to speak the same language as the insurance company. By presenting a claim with the same level of detail and professionalism the carrier expects, they force the insurer to adjust the claim based on facts and policy language, not on minimizing their payout.

Why It Stands Out

For The Public Adjusters, Inc. is more than just a claims service; it is a dedicated advocacy firm for property owners in a vulnerable position. Their contingency fee model, where they are only paid a percentage of the settlement they recover for you, perfectly aligns their goals with yours: to maximize your financial recovery. This “no recovery, no fee” structure removes financial risk and ensures they are motivated to fight for every dollar you are owed. If you are struggling with a complex or disputed property claim in North Carolina or Virginia, their expertise offers a clear path toward a fair and just settlement.

If you are new to this process, you can get a better understanding of their role by exploring what a public adjuster is and how they can help you.

Website: https://forthepublicadjusters.com

2. NAPIA — National Association of Public Insurance Adjusters Directory

When your search for the “best public adjuster near me” begins, starting with a trusted professional organization is a powerful first step. The National Association of Public Insurance Adjusters (NAPIA) is the premier trade association for public adjusting professionals in the United States. Its website offers a robust, free-to-use directory that serves as a high-trust vetting tool for policyholders facing difficult claims with carriers like State Farm or Allstate, who are often more focused on their profits than your recovery.

The primary advantage of using the NAPIA directory is the inherent layer of trust. Every adjuster and firm listed must adhere to a strict Code of Professional Conduct and meet ongoing continuing education requirements. This commitment to ethics is a crucial differentiator, ensuring you are connecting with professionals dedicated to advocating fiercely and fairly on your behalf, especially when an insurance company is delaying, denying, or underpaying your claim.

How to Effectively Use the NAPIA Directory

The “Find a Public Adjuster” tool is straightforward. You can search by state, city, or even by a specific firm’s name. This functionality is invaluable for homeowners in North Carolina or Virginia who need immediate, local expertise to fight back after a hurricane, fire, or major storm.

Here are a few practical tips for leveraging the platform:

- Filter Locally: Start by searching for your state (e.g., North Carolina) and then narrow it down to your city or a nearby major metro area.

- Create a Shortlist: Identify 3-5 member firms from the search results. Visit their individual websites to learn more about their specific experience with claims like yours (e.g., water damage, fire, or complex commercial claims).

- Verify Credentials: Use the directory as a starting point, but always cross-reference their license with your state’s Department of Insurance.

Why It Stands Out

What makes NAPIA unique is its focus on professional standards over commercial interests. It’s not a lead-generation service or a “pay-to-play” directory where adjusters can buy a top spot. Instead, it’s a merit-based listing of members who have chosen to be part of a self-regulating body that prioritizes the policyholder. This is a significant advantage when you’re battling a carrier that is using every tactic to minimize your payout. While the directory only lists NAPIA members, this “con” is also its greatest strength: it provides a pre-vetted list of dedicated advocates. For more insights on the value a professional adjuster brings to the table, you can explore the benefits of hiring a public adjuster.

| Feature Comparison | NAPIA Directory | General Web Search |

|---|---|---|

| Vetting Process | Members must adhere to a Code of Ethics & CE requirements. | No inherent vetting; results based on SEO and advertising. |

| Trust Factor | High. Association-backed and professionally monitored. | Low to moderate. Requires extensive independent verification. |

| Cost to Use | Free for consumers. | Free for consumers. |

| Focus | Connecting policyholders with qualified, ethical professionals. | Can be dominated by paid ads and lead-generation sites. |

3. United Policyholders (UP) — Professional Help Directory

When you are feeling overwhelmed by an insurance company’s tactics, United Policyholders (UP) provides a beacon of hope. As a non-profit organization, their mission is to be a trustworthy and knowledgeable resource for consumers, not a profit center for insurers. Their website offers a comprehensive Professional Help Directory designed to connect policyholders with vetted professionals, including the best public adjuster near me who can fight back against a carrier’s unfair settlement offer.

The core value of using the UP directory is its consumer-first approach. It’s more than just a list of names; it’s an educational hub. UP equips you with hiring checklists, sample questions to ask adjusters, and a rich library of resources. This is essential when you’re preparing to challenge a lowball offer from a massive insurer focused more on its shareholders than on your full recovery from a fire or hurricane.

How to Effectively Use the UP Directory

The UP directory is a powerful tool for education and connection. Instead of just finding a name, you can learn what to look for in a high-quality public adjuster before you even make the first call. This preparation is your first line of defense against a difficult claims process.

Here are a few practical tips for leveraging the platform:

- Educate First: Before searching the directory, explore UP’s “Hiring Help” section. Read their guides and download the checklist of questions to ask a potential public adjuster.

- Search and Compare: Use the directory to search for adjusters in your state, like Virginia or North Carolina. Create a shortlist and use UP’s resources to conduct structured interviews with each candidate.

- Ask for a Contract Review: Ask potential adjusters about their contracts and fee structures. Use UP’s guidance to spot any red flags before you sign.

Why It Stands Out

What makes United Policyholders exceptional is its unwavering commitment to policyholder advocacy. It is not a lead-generation farm; it’s a non-profit educational resource. This distinction is critical. The platform provides the tools to vet and compare professionals yourself, empowering you to make an informed decision rather than just picking a name from a list. While UP does not explicitly endorse the professionals listed, it provides the framework you need to conduct your own due diligence, including links to state regulators to verify licensing. This “do it yourself” vetting approach, supported by expert guidance, is invaluable for homeowners trying to navigate a complex claim.

| Feature Comparison | UP Directory | General Web Search |

|---|---|---|

| Vetting Process | Provides tools and education for users to vet professionals. | No inherent vetting; results based on SEO and advertising. |

| Trust Factor | High. Non-profit, consumer-advocacy focus. | Low to moderate. Requires extensive independent verification. |

| Cost to Use | Free for consumers. | Free for consumers. |

| Focus | Empowering policyholders with education and resources to hire help. | Can be dominated by paid ads and lead-generation sites. |

4. Better Business Bureau (BBB) — Local Category Pages for Public Adjusters

After identifying potential public adjusters, your next step should be a thorough reputational check. The Better Business Bureau (BBB) serves as a valuable resource for this crucial vetting stage. While not a primary discovery tool, it provides critical insights into a firm’s history of customer interactions, especially how they handle disputes. This is particularly important when you’re already fighting a difficult carrier like State Farm or Allstate, who often use delay tactics; the last thing you need is an unresponsive advocate.

The main advantage of using the BBB is its focus on transparency through customer complaints and reviews. You can see not just a firm’s rating but also the nature of any complaints filed against them and, crucially, how the business responded. This information can reveal red flags, such as poor communication or unresolved fee disputes, helping you avoid firms that might cause more stress during an already difficult claims process.

How to Effectively Use the BBB

The BBB website is most effective when used as a cross-verification tool for a shortlist of candidates. You can search directly for “Public Adjuster” in your city or search for a specific firm’s name.

Here are a few practical tips for leveraging the platform:

- Review Complaint Details: Don’t just look at the rating. Read the full text of any complaints to understand the context. Pay close attention to how the public adjuster responded; a professional and timely response is a good sign.

- Check Business History: Note how long the firm has been in business. A long-standing, accredited business often indicates stability and experience, which is vital for complex claims in North Carolina or Virginia.

- Filter Your Search: Use the filters to narrow results by accreditation status, letter grade rating, or location to refine your search for the best public adjuster near me.

Why It Stands Out

What makes the BBB a unique resource is its role as a public watchdog. It is one of the few platforms where you can see detailed, unmoderated disputes between consumers and businesses. While a lack of complaints is ideal, seeing how a firm professionally resolves a disagreement can be just as telling. It offers a layer of due diligence that general review sites lack. The primary downside is that not all excellent public adjusters seek BBB accreditation, and review volume can be low for this specialized profession, so a rating may be based on very limited data.

| Feature Comparison | BBB | General Web Search |

|---|---|---|

| Vetting Process | Based on accreditation standards, complaint history, and customer reviews. | No inherent vetting; results based on SEO and advertising. |

| Trust Factor | Moderate to High. Focuses on transparency and dispute resolution. | Low. Requires significant independent verification. |

| Cost to Use | Free for consumers. | Free for consumers. |

| Focus | Assessing business reputation and customer service history. | Dominated by marketing, ads, and lead generation. |

5. NAIC / State Regulator License Lookup

Before you hire any public adjuster to fight back against a lowball offer from your insurance company, your final and most critical step is to verify their credentials. The National Association of Insurance Commissioners (NAIC) provides a vital resource that links you directly to your state’s official insurance department. This is not a directory for finding an adjuster, but rather the ultimate authority for confirming that the professional you’re considering is licensed, in good standing, and legally permitted to represent you.

The primary advantage of using your state’s Department of Insurance (DOI) lookup tool is absolute certainty. Unlicensed operators prey on vulnerable homeowners after disasters, and hiring one can jeopardize your entire claim. Verifying a license through the official state regulator ensures you are partnering with a legitimate advocate who is accountable to the state, not a scam artist. This is a crucial defense when you’re already facing a difficult battle with a carrier focused on protecting its own profits.

How to Effectively Use State Licensing Tools

The NAIC website provides a simple map that links directly to each state’s insurance department. Once you’re on your state’s site, like the North Carolina Department of Insurance or the Virginia Bureau of Insurance, you will look for a “Licensee Lookup” or “Agent Search” tool.

Here are a few practical tips for leveraging these official resources:

- Verify Every Candidate: After shortlisting adjusters from directories like NAPIA, use the state lookup tool to verify each one’s license number and status.

- Check for Disciplinary Actions: Some state portals will show if an adjuster has faced any enforcement actions or complaints, which is a major red flag.

- Confirm State Rules: Your state’s DOI website is the source for regulations, such as fee caps during a catastrophe in North Carolina, which can protect you from price gouging. Understanding the crucial differences between the insurance company’s adjuster and your own advocate is key; you can explore this further to see why a public adjuster’s role is so vital.

Why It Stands Out

What makes the state regulator’s database essential is its role as the single source of truth. Unlike commercial directories, this information is not influenced by advertising or membership fees. It is a direct, unbiased report on a professional’s legal standing to practice. While some state websites can be clunky and less user-friendly than modern search platforms, their authority is unmatched. This “con” of a potentially poor user experience is a small price to pay for the “pro” of avoiding fraudulent operators and confirming you’re hiring the best public adjuster near me who is fully compliant and legally authorized to fight for your rights.

| Feature Comparison | State Regulator Lookup | General Web Search |

|---|---|---|

| Vetting Process | The official, legally mandated licensing and compliance record. | No inherent vetting; results are based on marketing and SEO. |

| Trust Factor | Absolute. Information comes directly from the government authority. | Low. Requires extensive cross-referencing and verification. |

| Cost to Use | Free for consumers. | Free for consumers. |

| Focus | Providing factual, unbiased data on licensure and compliance. | Delivering search results, which often include paid ads and unvetted listings. |

Top 5 Public Adjuster Comparison

| Service / Tool | Complexity (process) ???? | Resource Requirements ⚡ | Expected Outcomes ⭐???? | Ideal Use Cases ???? | Key Advantages ⭐ |

|---|---|---|---|---|---|

| For The Public Adjusters, Inc. | Moderate–high — full end-to-end claim handling (inspection, scope, negotiation) | Contingency fee (typically 10–30%), client documentation, regional on-site visits | High — measurable settlement increases for complex/denied claims ⭐⭐⭐⭐⭐ | NC & VA homeowners/businesses with complex, denied or underpaid claims | Certified adjusters, free initial review, proven local results |

| NAPIA — Directory | Low — search & browse professionals; no engagement workflow | Minimal (time to search); relies on member firms for follow-up | Moderate — faster shortlist of vetted professionals ⭐⭐???? | Finding local licensed public adjusters nationwide for initial shortlist | Profession-led vetting, ethics/CE standards |

| United Policyholders (UP) — Directory | Low — directory plus educational resources and checklists | Minimal time; use of guides and Ask‑an‑Expert forum | Moderate — better-informed hiring decisions; improved vetting ⭐⭐⭐???? | Consumers who want education and hiring tools before engaging an adjuster | Consumer-first guidance, hiring checklists, expert Q&A |

| Better Business Bureau (BBB) — Local Pages | Low — reputation check and complaint review | Minimal time to review profiles and complaints | Low–Moderate — reputation signals and complaint trends ⭐⭐???? | Cross-checking shortlisted firms for complaints and responsiveness | Complaint history, ratings, accreditation indicators |

| NAIC / State Regulator License Lookup | Low–moderate — verification process may be bureaucratic | Minimal cost; time to search state DOI records | High — authoritative licensure and enforcement info ⭐⭐⭐⭐???? | Verifying licensure, fee rules, and avoiding unlicensed operators | Official source for license standing and statutory fee rules |

Take Control of Your Claim and Get the Settlement You Deserve

Searching for the “best public adjuster near me” is more than just a task on your to-do list; it’s the critical first step toward leveling the playing field against a powerful insurance company. The aftermath of a property disaster is chaotic and stressful, and carriers like State Farm or Allstate often exploit this vulnerability. They deploy their own adjusters, trained to protect the company’s financial interests by delaying, denying, and underpaying valid claims. You’ve paid your premiums faithfully, and now you deserve an expert who works exclusively for you.

This article has equipped you with a robust toolkit to cut through the noise and find a qualified advocate. From national directories like NAPIA and Adjusters International to state-level license verification tools, you now have the resources to vet potential partners thoroughly. Remember, the right public adjuster isn’t just a claim preparer; they are your strategist, your documentarian, and your champion in a fight you should not have to wage alone.

From Information to Action: Your Next Steps

The difference between a frustrating, lowball settlement and a fair, comprehensive recovery often comes down to who is in your corner. Don’t let your insurer dictate the value of your loss. It’s time to take decisive action.

- Revisit the Tools: Go back through the list of resources. Use the NAIC license lookup to verify the credentials of any adjuster you are considering. Cross-reference their profile on platforms like the BBB to check for experience, specialties, and any unresolved complaints.

- Schedule Consultations: Don’t settle for the first option. Contact at least two or three public adjusters from your research. Most reputable firms, including For The Public Adjusters, Inc., offer a no-cost, no-obligation claim review. Use this opportunity to gauge their expertise, communication style, and understanding of your specific situation.

- Ask the Tough Questions: During your consultations, be prepared. Ask about their fee structure, their experience with your specific type of damage (fire, water, NFIP flood), and their track record with your insurance carrier. Request references from past clients with similar claims. A confident and experienced adjuster will welcome this scrutiny.

- Document Everything: While you search, continue to document everything related to your claim. Keep a detailed log of all communications with your insurance company, including dates, times, and the names of people you spoke with. This meticulous record-keeping will be invaluable to the public adjuster you hire. To truly take control and secure the settlement you deserve, it’s essential to have a clear understanding of specific claim types, such as a guide to navigating a storm damage roof insurance claim, which details the kind of evidence and documentation needed.

Your Advocate in North Carolina and Virginia

For homeowners and business owners in North Carolina and Virginia, the path to a fair settlement can be particularly challenging, especially when dealing with catastrophic events like hurricanes or complex NFIP flood claims. Your insurance policy is a contract, and a public adjuster ensures the insurer holds up their end of the bargain. By meticulously documenting your loss, citing policy language, and negotiating from a position of strength, they force the insurance company to pay what you are rightfully owed.

You don’t have to be an insurance expert to get a fair outcome. You just need to hire one. Choosing to engage a public adjuster is choosing to empower yourself with the knowledge and leverage necessary to rebuild your life or business without compromise.

2. Why shouldn’t I just use the "Adjuster" provided by my insurance company?

The insurance company’s adjuster has a fiduciary duty to the carrier, not to you. There are three types of adjusters: Staff Adjusters (employees of the insurer), Independent Adjusters (contractors hired by the insurer), and Public Adjusters (hired exclusively by the policyholder). A Public Adjuster is the only professional licensed to advocate for your interests. In NC and VA, the "best" adjusters act as your claims quarterback—managing everything from forensic damage assessments to negotiating "Law & Ordinance" upgrades that staff adjusters frequently overlook.

3. Is it legal for my roofing contractor in VA or NC to negotiate my insurance claim?

No. In both North Carolina and Virginia, it is a crime for a contractor to negotiate an insurance claim; this is known as the Unauthorized Practice of Public Adjusting (UPAL). In Virginia, under Va. Code § 38.2-1845.1, only licensed public adjusters or attorneys can legally represent a policyholder in a claim. If your contractor is "handling the insurance," your claim could be voided for fraud, and you lose all legal leverage. The best practice is to have your contractor identify the damage and your Public Adjuster negotiate the settlement.

4. How much do the best public adjusters charge in NC and VA?

Public adjusters typically charge a contingency fee ranging from 10% to 20% of the total settlement, but specific state caps apply during disasters.

In North Carolina: Following a declared State of Emergency (like a hurricane), fees are often capped at 10% of the claim proceeds. The best public adjusters near me in NC cannot charge upfront "file fees" or "inspection fees," which are against NC State Statutes.

In Virginia: Fees must be "reasonable" and are clearly outlined in the written contract required by state law. The "best" adjusters provide a transparent fee schedule and do not charge upfront "file fees" or "inspection fees," which are red flags of predatory firms.

5. Can a public adjuster help me if my claim was already denied or "lowballed"?

Yes. A public adjuster’s primary value is in "reopening" claims where the insurer issued a partial payment or a full denial based on "wear and tear." In the Piedmont and Coastal regions of NC and VA, insurers often blame storm damage on age. A top-tier public adjuster will hire an independent engineer to provide a "Causation Report" that proves the storm was the primary "proximate cause," forcing the insurer to acknowledge coverage under the NC/VA Standard Fire Policy guidelines.

6. What is the "Appraisal Clause," and why does my local public adjuster use it?

The Appraisal Clause is a powerful alternative dispute resolution tool found in most NC and VA policies used to settle "amount of loss" disputes without a lawyer. If you and the insurance company disagree on the cost of repairs, your Public Adjuster can invoke Appraisal. This involves two independent Appraisers and a neutral Umpire. In North Carolina and Virginia, the decision of the Appraisal panel is generally binding, making it a faster and cheaper alternative to litigation.

7. How does a local public adjuster determine the "best" price for my repairs?

The best local adjusters use Xactimate or Symbility, but they manually adjust the "Price List" to reflect actual Raleigh, Charlotte, or Richmond labor rates. Insurance companies use "standardized" regional pricing that often lags behind real-world inflation. A local NC/VA adjuster understands the specific costs for IBHS Fortified Roof standards in coastal NC or historic preservation codes in Richmond, ensuring your settlement covers the actual cost of local contractors, not a national average.

8. When is it "too late" to hire a public adjuster for a claim in Virginia or North Carolina?

While it’s best to hire an adjuster immediately, you can generally hire one up until the Statute of Limitations expires, which is often 2 or 3 years depending on your state and policy. * Virginia: Most policies have a 2-year window to file suit or finalize a claim.

North Carolina: The window is often 3 years, but many "standard" policies shorten this. If you’ve already signed a "Proof of Loss" or a "Final Release," it may be too late. The "best" adjusters will offer a free claim review to determine if there is still "money left on the table."

9. Will hiring a public adjuster cause my insurance company to drop me?

No. In North Carolina and Virginia, it is a violation of unfair trade practices for an insurer to retaliate against a policyholder for hiring a licensed professional. Your policy is a contract that explicitly allows for professional representation. Hiring a public adjuster often makes the insurer’s job easier because they are dealing with a professional who provides evidence-backed estimates in a format the carrier can actually process.

10. How do I solve a dispute with my public adjuster if I’m not satisfied?

If you are in NC or VA, you have a statutory right to a "cooling-off" period to cancel your contract. * North Carolina: You have 3 business days to cancel a public adjuster contract.

Virginia: You have 3 business days (or 5 if the loss occurred during a disaster). If a dispute arises later, you can file a complaint with the NCDOI Consumer Services or the VA SCC. The "best" public adjuster firms will always have a "Satisfaction Guarantee" or a clear termination clause in their contract.

Don’t let your insurance company have the final say on your recovery. If you’re in North Carolina or Virginia and need a dedicated expert to fight for your claim, reach out to For The Public Adjusters, Inc. Their team offers the specialized advocacy needed to challenge unfair settlement offers and secure the funds you deserve.