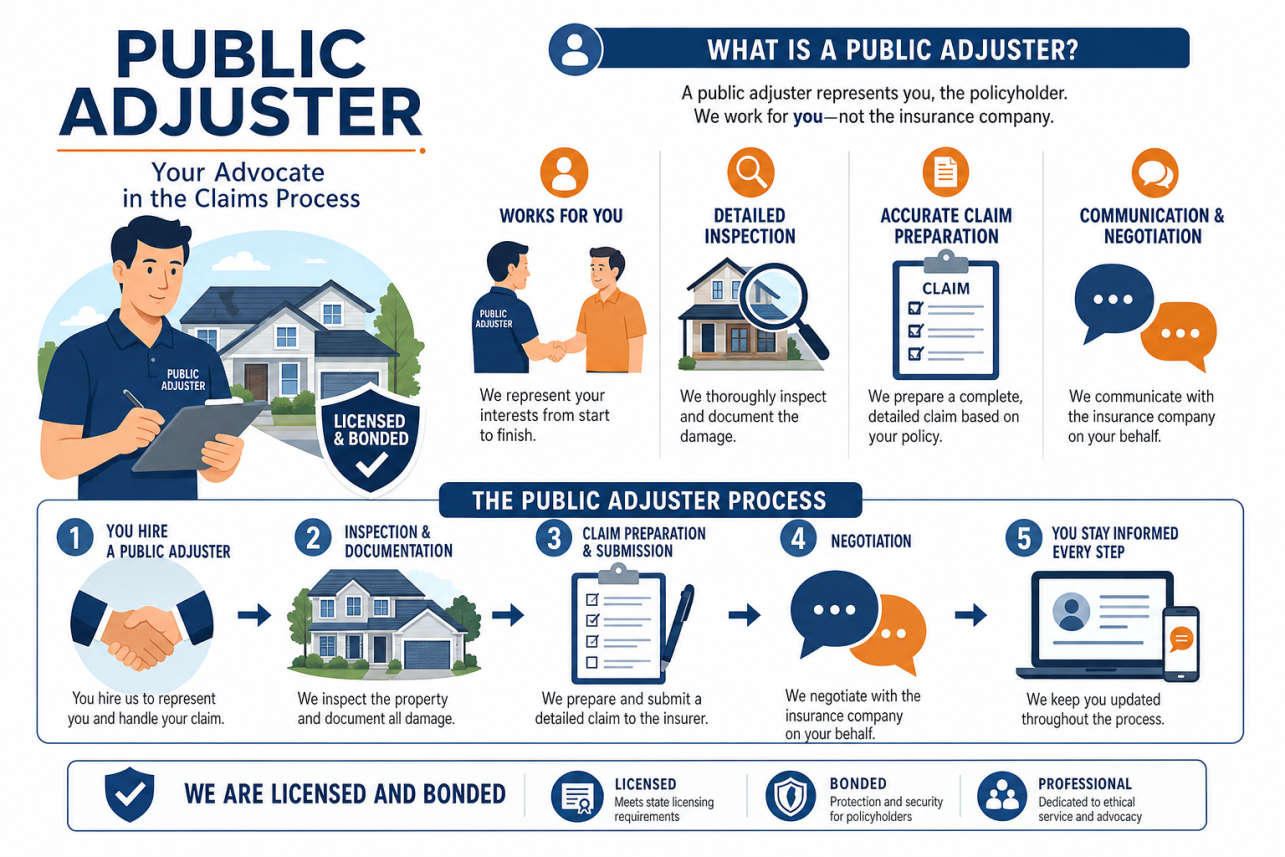

A public adjuster Cary NC policyholders hire works exclusively for you — not the insurance company — to document, value, and negotiate your property damage claim. For The Public Adjusters, Inc. is licensed and bonded, and we represent Cary homeowners and business owners on fire, water, smoke, wind, tree, vandalism, and flood losses. Because we are paid only from what your claim recovers, our interests stay aligned with yours from the first inspection to the final settlement check.

Key takeaways

- A public adjuster Cary NC homeowners trust works exclusively for the policyholder, not the insurance company, to maximize claim settlements.

- For The Public Adjusters, Inc. handles the entire insurance claim process for Cary residents, from damage documentation to final settlement negotiation.

- Hiring a public adjuster Cary NC property owners rely on can significantly increase claim payouts compared to accepting the insurer's first offer.

- For The Public Adjusters, Inc. serves Cary and the greater Wake County area for fire, water, storm, and other property damage claims.

- There are no upfront fees when working with a public adjuster Cary NC policyholders choose, as compensation is typically a percentage of the recovered settlement.

What This Service Is

When your home or building is damaged, the insurance company sends its own adjuster. That person is trained, experienced, and paid by the insurer. Most policyholders, by contrast, are handling their first serious claim while also dealing with a damaged home.

A public adjuster levels that field. We read your policy line by line, inspect and photograph every area of damage — including the hidden kind, like smoke residue in ductwork or moisture inside wall cavities — and prepare a detailed, itemized estimate of the loss. Then we negotiate directly with the carrier on your behalf.

Our Cary adjusters handle residential homeowners claims and commercial business claims alike: kitchen fires and full structure fires, burst pipes and roof leaks, wind and hail, fallen trees, vehicles that strike a home, vandalism, and flood losses including NFIP flood claims. We do not handle cell phone, motor vehicle, health, or life insurance matters — buildings and their contents are our entire focus.

The NCDOI Public Adjusters Guide explains that public adjusters in North Carolina must be licensed, and we encourage every policyholder to verify a license before signing anything. We are licensed and bonded, and we never promise a specific dollar outcome — no honest adjuster can. What we can promise is that your claim will be fully documented and professionally argued.

Common Problems

Lowball Offers — And How A Public Adjuster Cary NC Homeowners Hire Pushes Back

The first settlement offer is often based on a quick walkthrough and a software estimate that misses matching materials, code upgrades, and hidden damage. A pine limb through the roof, for instance, rarely stops at the shingles — it can crack decking, tear underlayment, and let water into insulation and drywall.

We build our own scope of loss from scratch, room by room and item by item. When our estimate and the carrier's don't match, we negotiate from documented evidence, not frustration.

Wind Vs. Water Disputes After Tropical Storms

When a hurricane remnant pushes through the Triangle, insurers sometimes argue over whether damage came from covered wind or excluded flooding. Policyholders have won this fight in court: in Corban v. USAA, the Mississippi Supreme Court sided with homeowners after Hurricane Katrina, holding that an insurer could not use water exclusions to escape paying for damage that wind actually caused.

Cause-of-loss arguments are winnable — but only with strong documentation gathered early. That is exactly the record we build for our clients.

Denied, Delayed, Or Underscoped Claims

A denial letter is not always the final word. Denials frequently rest on a policy interpretation or an incomplete inspection, both of which can be challenged with better evidence.

Delays are just as costly. Water damage left in limbo grows mold in Cary's summer humidity, turning a manageable claim into a much larger one. We keep the file moving, respond to every carrier request promptly, and document any prejudice caused by insurer delay.

Our Process

Free Policy And Damage Review

We start by reading your actual policy — coverages, endorsements, deductibles, and exclusions — and walking the property with you. Whether it's smoke damage after a kitchen fire or a tree resting on your roofline, we tell you honestly whether professional representation makes sense for your loss.

Full Documentation And Valuation

We photograph and measure everything, inventory damaged contents, and prepare a line-item estimate using the same industry pricing tools carriers use. For flood losses, we prepare the proof-of-loss documentation the National Flood Insurance Program requires, on the strict deadlines NFIP claims demand.

Negotiation Through Settlement

We present the claim, meet the insurer's adjuster on site, answer their engineers and consultants point by point, and negotiate until the offer reflects the documented loss. You approve every decision; nothing settles without your sign-off. Our fee comes from the recovery, so we only do well when you do.

| What Happens | Filing on Your Own | With a Licensed Public Adjuster |

|---|---|---|

| Damage documentation | Carrier's adjuster decides what gets photographed and measured | Independent inspection with moisture mapping, thermal imaging, and full scope documentation |

| Estimate pricing | Carrier software often uses below-market rates local contractors won't accept | Line-item Xactimate estimate priced to actual Wake County contractor rates |

| Negotiation | You argue your own claim against trained claims professionals | Licensed advocate negotiates every supplement and re-inspection for you |

| Policy interpretation | Exclusions, sublimits, and endorsements are easy to misread | Full policy review to identify every coverage that applies, including ones the carrier didn't mention |

| Time commitment | Dozens of hours of calls, emails, and meetings on your schedule | We handle correspondence and deadlines while you keep working and living |

| Typical result | First offers frequently undervalue the loss | Settlements routinely increase substantially once the full scope is documented |

Commonly Overlooked In The Public Adjusting Industry

- Matching provisions for continuous flooring and siding — Carriers often pay to patch one room or one wall, when North Carolina line-of-sight and matching arguments can require replacing the entire continuous surface.

- Ordinance and law coverage for code upgrades — Cary and Wake County building codes have changed over the years, and repairs often trigger required upgrades the base estimate never accounts for.

- Recoverable depreciation left unclaimed — Many policyholders never realize the depreciation withheld from their first check can be recovered after repairs, so thousands go unclaimed every year.

- Hidden moisture behind undisturbed walls — Field adjusters rarely carry moisture meters or thermal cameras, so water that migrated into closed cavities gets left out of the scope entirely.

- Additional living expenses beyond the first hotel stay — ALE covers meals, mileage, pet boarding, and extended displacement, but carriers seldom volunteer the full list of reimbursable costs.

- HVAC and duct contamination after fire or smoke losses — Soot pulled through the ductwork recontaminates a cleaned home, yet duct cleaning and system inspection are missing from most initial estimates.

- Seasonally accurate business interruption projections — Carriers tend to average recent slow months instead of modeling what the business would actually have earned during the restoration period.

- Proof-of-loss and claim deadlines in the policy conditions — Missing a contractual deadline can jeopardize an otherwise valid claim, and insurers are under no obligation to remind you it's approaching.

Case Studies

Case Study #1

Situation: A family in the Preston area of Cary came home from a July vacation to find their bonus room ceiling collapsed. A supply line to the second-floor HVAC condensate system had failed, and water had run for days through the ceiling, walls, and hardwood flooring below.

Problem: Their carrier's field adjuster spent forty minutes on site and issued an estimate of $11,400 — enough to replace drywall and paint, but nothing for the buckled site-finished oak floors, the saturated wall insulation, or the mold already blooming behind the baseboards in Wake County summer humidity.

Investigation: Our adjuster brought in a thermal imaging camera and moisture meters and mapped water migration through three rooms the carrier never opened up. We pulled baseboards, documented microbial growth with photos and lab sampling, and had a licensed flooring contractor confirm that site-finished hardwood cannot be patch-repaired to match.

Findings: The actual scope included continuous hardwood replacement across the connected living and dining areas, full insulation removal in two wall cavities, professional mold remediation under the policy's fungi endorsement, and pack-out costs for furniture. The carrier's estimate had also used builder-grade pricing that no Cary contractor would honor.

Solution: We rewrote the estimate in Xactimate with documented local pricing, submitted the moisture mapping and lab results, and invoked the policy's matching provision under North Carolina's line-of-sight guidance for continuous flooring. We then handled every carrier call and re-inspection so the family didn't have to.

Outcome: The claim settled at $67,800 — roughly six times the original offer — including the fungi sublimit paid in full and additional living expenses for the two weeks the family stayed out during remediation.

Lesson: Water losses in Cary homes are rarely surface-deep. If the carrier's adjuster didn't use a moisture meter and didn't open a single wall, the estimate is almost certainly incomplete.

Case Study #2

Situation: The owner of a small strip-center restaurant off Kildaire Farm Road suffered a kitchen fire that started in the hood system. The flames were out in minutes, but smoke and suppression chemicals contaminated the dining room, walk-in coolers, and everything in between.

Problem: The insurer accepted the fire claim but lowballed the contents inventory, denied most of the smoke-related dining room damage as 'pre-existing wear,' and calculated business interruption using only the slow January weeks before the loss — ignoring that spring is the restaurant's strongest season.

Investigation: We performed a full contents inventory item by item, including the spoiled walk-in stock, and had an industrial hygienist test dining room surfaces for combustion residue. For the income claim, we pulled two years of POS data and tax returns to build a realistic revenue projection covering the actual restoration period.

Findings: Wipe samples confirmed char and soot residue throughout the dining room, defeating the wear-and-tear denial. The contents inventory came in at nearly triple the carrier's allowance, and the corrected business interruption model showed projected spring revenue the January-only calculation had erased.

Solution: We packaged the hygienist report, inventory documentation, and financial projections into a formal supplemental claim, then negotiated directly with the carrier's large-loss adjuster and their outside accountant over three rounds.

Outcome: The final settlement reached $312,000 across building, contents, and business interruption — an increase of more than $180,000 over the initial position — and the restaurant reopened four and a half months after the fire.

Lesson: Commercial claims are won or lost on documentation. Insurers rarely volunteer a fair business interruption number; the seasonality of your revenue has to be proven, not assumed.

| Your Situation | Should You Hire an Adjuster? | What It Depends On |

|---|---|---|

| Small claim under your deductible or barely above it | Usually not | If the payout is a few hundred dollars over your deductible, a fee may not make sense — we'll tell you honestly in a free review |

| Water damage with possible hidden moisture or mold | Yes, early | Hidden migration behind walls and under floors is where carriers underpay most; documentation must happen before repairs |

| Fire or smoke loss, residential or commercial | Yes, immediately | Contents inventories, soot testing, and additional living expenses are complex and time-sensitive |

| Storm or hail damage the carrier called 'cosmetic' | Yes | An independent inspection often finds functional damage — cracked mats, compromised seals — the drive-by inspection missed |

| Claim already denied or delayed for weeks | Yes | North Carolina allows supplemental claims and formal disputes; denials are frequently reversible with proper evidence |

| Carrier offer received but repairs quotes come in higher | Yes | The gap between the estimate and real contractor bids is exactly what a supplement negotiation closes |

| Business interruption or lost rental income claim | Yes | Income projections require financial documentation carriers rarely calculate in your favor on their own |

| You already signed a full release and cashed final payment | Maybe | Options narrow after a release, but call anyway — some policies and situations still allow reopening |

Reviews

Our insurance company offered $9,000 for hail damage to our roof in the Lochmere area and called it cosmetic. For The Public Adjusters found soft-metal strikes, cracked shingle mats, and gutter damage their adjuster never photographed. The claim reopened and settled for a full roof replacement plus interior repairs. I would never negotiate with a carrier alone again.

Melissa T., Cary

After a pipe burst in our crawl space, the carrier kept asking for documents and going quiet for weeks. Once we hired this team, every deadline was tracked, every letter was answered, and the moisture readings they took found damage under our kitchen the insurer's estimate skipped entirely. Settlement came in at almost four times the first offer.

Raj P., Cary

I manage a rental property near downtown Cary that had a kitchen fire. I honestly didn't know public adjusters existed until my contractor recommended them. They handled the contents inventory, fought the depreciation the carrier applied, and got my tenants' displacement covered. Only wish I'd called them on day one instead of week six.

Donna W., Apex

Frequently Asked Questions

What Does A Public Adjuster Cary NC Homeowners Hire Actually Do For My Insurance Claim?

A public adjuster works exclusively for you, the policyholder, never for the insurance company. When you hire For The Public Adjusters, Inc., we take over the entire claim process: documenting the damage, reading your policy line by line, preparing a detailed estimate, and negotiating directly with your insurer's adjuster until you receive a fair settlement.

That matters because the adjuster your insurance company sends out is paid by the carrier. Their estimate often misses hidden damage, code-upgrade costs, or coverages buried in your policy language. We build an independent scope of loss using the same estimating software carriers use, so we can challenge their numbers item by item.

In Cary specifically, we handle a lot of wind and hail claims on homes in neighborhoods like Preston, Lochmere, and Carpenter Village, plus water damage claims from burst supply lines and failed water heaters. We know how Wake County permitting and current building codes affect repair costs, and we make sure those costs are included in your settlement rather than coming out of your pocket.

From the first inspection to the final check, you have one advocate managing deadlines, correspondence, and proof-of-loss paperwork. Most clients tell us the biggest relief is simply not having to argue with the insurance company themselves. If you have already received a lowball offer or a denial, we can also step in mid-claim and reopen the negotiation with proper documentation.

How Much Does It Cost To Hire A Public Adjuster In Cary?

For The Public Adjusters, Inc. works on a contingency fee, which means you pay nothing upfront and nothing out of pocket. Our fee is a percentage of the insurance settlement we recover for you, and it is agreed to in writing before we start. If we do not recover money for you, you do not owe us a fee.

North Carolina regulates public adjusting under state law, and fee agreements must be clearly disclosed in the contract you sign. We walk Cary clients through every line of that agreement so there are no surprises later.

Here is the practical math most homeowners care about: industry studies and our own case files consistently show that professionally represented claims settle for significantly more than claims handled by the policyholder alone. When a carrier's first offer on a hail-damaged roof in Cary comes in at a fraction of true replacement cost, the increase we negotiate typically exceeds our fee many times over.

The percentage can vary depending on the size and complexity of the loss, whether the claim is new, underpaid, or denied, and how far along the claim already is. A fresh fire loss is priced differently than reopening a closed water claim. Call us for a free claim review; we will look at your policy and damage first, tell you honestly whether representation makes financial sense, and quote the exact fee before you commit to anything.

When Should I Call Your Team Instead Of Handling The Claim Myself?

Call us before you file, if possible. The way a claim is reported, worded, and documented in the first few days shapes everything that follows. We regularly see Cary homeowners accidentally hurt their own claims by giving recorded statements, accepting a quick partial payment, or signing off on an inadequate scope of repairs.

That said, it is never too late to bring us in. We take over claims at any stage: freshly filed, stalled, underpaid, or outright denied. North Carolina gives policyholders time to dispute a settlement, and a supplemental claim backed by a professional estimate often recovers money the first offer left behind.

Some situations almost always justify professional representation. Large or complex losses like house fires, major water intrusion, or tree strikes from the storms that roll through Wake County every spring and summer. Claims where the carrier's estimate looks suspiciously low compared to local contractor quotes. Any claim involving disputes over matching shingles or siding, code upgrades, or whether damage is storm-related versus wear and tear.

Smaller, straightforward claims sometimes do not need us, and we will tell you that honestly during a free consultation. But if your home in Cary has serious damage, or the insurance company is already pushing back, having a licensed adjuster on your side levels a playing field that is otherwise heavily tilted toward the carrier. One phone call costs you nothing and can prevent mistakes that are difficult to undo.

What Types Of Property Damage Claims Do You Handle In Cary And Wake County?

For The Public Adjusters, Inc. handles the full range of residential and commercial property claims across Cary and the surrounding Wake County area, including Apex, Morrisville, and West Raleigh.

Wind and hail claims are the most common here. Severe thunderstorms and the occasional tropical system push through the Triangle every year, damaging roofs, siding, gutters, and windows. These claims frequently get underpaid because carriers dispute hail hit counts or offer roof repairs when full replacement is warranted, and that is exactly where a public adjuster Cary NC property owners trust earns their fee.

Water and plumbing losses are a close second. Cary's housing stock ranges from 1980s homes with aging supply lines to newer construction with PEX and tankless systems, and we handle everything from slab leaks and burst pipes to water heater failures and appliance overflows, including the mold issues that follow when drying is delayed.

We also represent policyholders on fire and smoke losses, lightning strikes, fallen trees, hurricane damage, and theft or vandalism claims. On the commercial side, we handle business property damage and the business interruption coverage that often gets overlooked.

Every claim starts the same way: a free inspection and policy review. We document the loss with photos, moisture readings, and measurements, then build an estimate that reflects real Wake County repair costs, not the discounted pricing carriers prefer. If you are unsure whether your damage is worth claiming, ask us first; we will give you a straight answer either way.

Can A Public Adjuster Cary NC Residents Trust Reopen A Claim That Was Denied Or Underpaid?

Yes, in many cases we can. North Carolina policies generally allow supplemental claims, and most give you up to three years from the date of loss to pursue the full amount owed. If your carrier denied your claim or paid far less than the repairs actually cost, that decision is rarely final.

Our process starts with a free review of the denial letter or settlement paperwork alongside your policy. Insurers in Wake County frequently underpay by missing hidden damage — moisture trapped behind drywall after a plumbing leak, hail bruising on shingles that only shows up on close inspection, or code-upgrade costs required by the Town of Cary's permitting office.

Once we identify the gap, we document it properly. That means a fresh inspection, photographs, moisture readings where relevant, and a line-item estimate built with the same software carriers use. We then file a supplemental claim or formally dispute the denial with evidence the insurer cannot easily brush aside.

We have reopened claims in Cary neighborhoods from Preston to Lochmere where homeowners were told the damage was "wear and tear" or below their deductible, only to recover meaningful settlements once the loss was scoped correctly. If you still have your denial or payment documents, bring them to us. Even claims that were closed months ago are often worth a second look, and reviewing yours costs you nothing.

Are Your Adjusters Licensed In North Carolina, And How Can I Verify That Before Hiring Anyone?

Every adjuster at For The Public Adjusters, Inc. holds an active North Carolina public adjuster license issued by the NC Department of Insurance. Licensing is not optional here — state law requires it for anyone negotiating a property claim on a policyholder's behalf, and working with an unlicensed "claim consultant" can put your entire settlement at risk.

Verifying us is simple, and we encourage it. Go to the NC Department of Insurance website and use the agent and adjuster lookup tool, or call the Department directly. You can search by name or license number, and we will give you our license numbers up front before you sign anything.

North Carolina also regulates how we work. Our contracts must clearly state our fee, you have a statutory right to cancel within three business days, and we are prohibited from paying referral fees to contractors — protections that matter after a storm, when out-of-state solicitors sometimes flood Cary and the rest of Wake County.

Beyond the license itself, ask any adjuster about local experience. Handling claims in Cary means understanding Town of Cary permitting, local rebuild costs that run higher than the state average, and how regional carriers' desk adjusters typically scope losses in the Triangle. We have negotiated with the same insurance company representatives repeatedly on Cary claims, and that familiarity shapes how we build and present each file. A license is the floor; local claim experience is what actually moves your settlement.

How Long Does The Claim Process Take When I Work With A Public Adjuster In Cary?

Most residential claims we handle in Cary resolve in 30 to 90 days from the day we take over, though the timeline depends on the size of the loss and how the carrier responds. A straightforward roof claim after a hailstorm often settles faster; a large fire or water loss with contents inventory and additional living expenses takes longer because there is simply more to document.

Here is the typical rhythm. In the first week, we inspect the property, photograph everything, and review your policy line by line. Within two to three weeks, we submit a complete, itemized claim package to your insurer. North Carolina rules then require the carrier to acknowledge and act on the claim within set timeframes, and we hold them to those deadlines.

Negotiation is usually where time is won or lost. Because we deliver a fully documented file up front — measurements, moisture maps, code-upgrade costs, comparable Wake County pricing — carriers have fewer excuses to delay or send repeated reinspections. Claims handled without that documentation routinely drag on for six months or more while homeowners chase adjusters who keep rotating off the file.

One honest caveat: after a major regional event, such as a hurricane pushing inland through the Triangle, every insurer's queue slows down. Even then, having a professional managing deadlines, follow-ups, and appraisal rights if needed keeps your claim moving instead of sitting at the bottom of a desk adjuster's stack.

Will Hiring A Cary Public Adjuster Raise My Insurance Premiums Or Damage My Relationship With My Insurer?

No. Your premium is affected by the claim itself — the type of loss, the amount paid, and your claims history — not by who represents you. Whether you negotiate alone or bring in a public adjuster Cary NC insurers already know by name, the carrier records the same claim either way. Recovering the full amount you are owed does not create a separate penalty.

Some homeowners worry that pushing back will make their insurer treat them as a problem customer. In practice, the opposite tends to happen. When a licensed professional submits a thorough, well-documented claim, the file gets handled more carefully because the carrier knows every figure will be checked. Sloppy lowball estimates are harder to justify when someone on your side can rebut them line by line.

It is also worth remembering that North Carolina law protects policyholders from unfair claim practices. An insurer cannot legally retaliate — through cancellation, non-renewal, or rate manipulation — simply because you exercised your right to representation. If a carrier's conduct ever crossed that line, it would face scrutiny from the Department of Insurance.

What genuinely can hurt you is filing small, marginal claims repeatedly, which is why we give honest advice up front. If your Cary home's damage falls near your deductible, we will tell you it is not worth filing. When the loss is significant, though, professional representation protects your recovery without costing you anything on future premiums beyond what the claim itself already would.

What Documents Should I Have Ready Before Meeting With A Public Adjuster Cary NC Property Owners Recommend?

The single most important document is your full insurance policy, including the declarations page and all endorsements. Many Cary homeowners only have the summary page, so if you can't find the complete policy, we can request a certified copy from your carrier on your behalf.

Beyond the policy, gather any photos or videos of the damage, ideally with timestamps. Pictures from before the loss are just as valuable, because they establish the condition of your home prior to the storm, fire, or water event. Real estate listing photos, holiday pictures, and even Zillow archives often help here.

Bring any correspondence you've already had with your insurance company: the claim number, emails, letters, and the carrier adjuster's estimate if one has been issued. Receipts for emergency repairs, tarping, water mitigation, or hotel stays matter too, since those are often reimbursable under your policy's additional living expense or emergency provisions.

For contents losses, start a rough inventory of damaged personal property, even if it's just a phone video walking room to room. Don't throw anything away until it has been documented.

That said, don't delay calling us because your paperwork isn't perfect. Plenty of Wake County clients come to us with nothing but a claim number, and we build the file from there. Our first meeting at your Cary property is free, and we'll tell you exactly what's missing and how to get it.

Do You Handle Commercial Property Claims In Cary, Or Only Residential Losses?

We handle both. A significant portion of our work involves commercial properties across Cary and Wake County, including retail spaces along Kildaire Farm Road and Walnut Street, office parks near the Weston area, restaurants, medical practices, warehouses, and multi-family apartment communities.

Commercial claims are considerably more complex than residential ones. Beyond building damage, they often involve business interruption coverage, loss of rents, extra expense provisions, and equipment or inventory losses. Carriers scrutinize these claims heavily, and the burden of documenting lost income falls on the policyholder. We work with your financial records to build a defensible business interruption calculation the insurer can't easily dismiss.

We also represent condominium and homeowner associations, which sit in a gray zone between residential and commercial. Association claims involve master policies, bylaws, and questions about where the association's responsibility ends and the unit owner's begins. Getting that allocation wrong can leave tens of thousands of dollars unclaimed.

For business owners, timing matters even more than it does for homeowners. Every week a claim drags on is another week of lost revenue, frustrated tenants, or displaced employees. Our adjusters push carriers to issue advance payments so mitigation and repairs can begin before the final settlement is reached.

If you own or manage commercial property anywhere in the Triangle and you've suffered fire, water, wind, or hail damage, call us before you accept the carrier's first number. The gap between an initial commercial offer and a properly documented claim is frequently substantial.

What Happens After I Sign With For The Public Adjusters — What Does Your Process Actually Look Like?

Once you sign our contract, we immediately send a letter of representation to your insurance carrier. From that point forward, the insurer is required to communicate through us, which takes the phone calls, deadlines, and paperwork off your plate entirely.

Next, we conduct our own detailed inspection of your Cary property. This is not a quick walkthrough. We document every affected area with photographs, moisture readings where relevant, and measurements, and we look for damage the carrier's adjuster commonly misses, such as hidden water intrusion behind walls, compromised roof decking, and smoke residue in HVAC systems.

From that inspection, we prepare a line-item estimate using the same industry software carriers use, priced for the Wake County construction market. Local labor and material costs matter; an estimate built on generic national pricing will come in low for the Triangle.

We then submit our documented claim package and negotiate directly with the carrier's adjuster. If they dispute our findings, we schedule joint reinspections and support our position with evidence, policy language, and North Carolina insurance regulations. You receive regular updates throughout, and no settlement is accepted without your approval.

Finally, when payment is issued, we review the settlement documents to confirm nothing was waived and that recoverable depreciation procedures are clearly explained, so you can collect every dollar you're owed as repairs are completed.

The Insurance Company Already Sent Its Own Adjuster And Made An Offer — Can A Public Adjuster Cary NC Families Use Still Get Involved?

Yes, and this is actually one of the most common situations we see. A public adjuster Cary NC policyholders bring in after the carrier's initial offer can review that estimate, identify what was missed or underpriced, and submit a supplemental claim demanding the difference. Accepting a first check does not close your claim in North Carolina; you generally retain the right to pursue additional amounts.

Carrier estimates in our area are frequently incomplete. We regularly find omitted items like code-required upgrades under Cary's permitting requirements, matching issues with discontinued roofing shingles or siding, inadequate drying and mold remediation scopes after water losses, and depreciation applied too aggressively.

When we take over a claim mid-stream, we start by comparing the carrier's line-item estimate against our own independent inspection. The gaps are often significant — it's not unusual for the documented scope of repairs to be substantially larger than what the first offer covered.

There is one important caution: deadlines. Your policy contains time limits for submitting documentation and disputing payments, and North Carolina's statute of limitations applies to the claim overall. The sooner we review your file after that first offer, the more options you have.

So if a check is sitting on your kitchen counter and something about the number feels wrong, don't cash it and move on without a second opinion. We'll review the carrier's estimate at no charge and tell you honestly whether it's fair or whether there's real money left on the table.

What's The Difference Between A Public Adjuster Cary NC Policyholders Hire And The Adjuster My Insurance Company Sends Out?

The difference comes down to who each adjuster works for. The adjuster your insurance company sends — whether a staff adjuster or an independent adjuster hired by the carrier — is paid by the insurer and represents the insurer's interests. Their job is to evaluate your claim within the company's guidelines, which often means a conservative estimate.

A public adjuster works exclusively for you, the policyholder. For The Public Adjusters, Inc. is retained by Cary homeowners and business owners, not by any insurance company, so our only obligation is to document your loss fully and pursue every dollar your policy entitles you to.

In practice, that difference shows up in the details. Carrier adjusters in Wake County frequently handle heavy caseloads, especially after a major hail or wind event moves through the Triangle, and inspections can be brief. We take the time to open ceilings, moisture-map walls, inventory contents room by room, and price repairs at actual local contractor rates rather than software defaults.

We also read your policy line by line. Coverages like code upgrade allowances, matching provisions for siding and roofing, and additional living expenses are commonly overlooked when nobody advocates for the insured. Having your own adjuster levels the playing field from the first inspection forward.

Is My Claim Large Enough To Justify Hiring Your Firm, Or Is That Only Worth It For Major Losses?

There's no strict dollar minimum, but the honest answer is that it depends on the gap between what your insurer is offering and what the loss is actually worth — not just the size of the loss itself. We give Cary property owners a free claim review, and if we don't believe we can add meaningful value beyond our fee, we'll tell you so up front.

As a rough guide, claims involving structural water damage, fire and smoke, roof replacement disputes, or business interruption almost always benefit from professional representation. These losses have hidden components — moisture inside wall cavities, smoke residue in HVAC systems, code-required upgrades — that carriers routinely leave out of their estimates.

Smaller claims can still make sense to bring to us when the insurer has denied coverage outright or offered a settlement that won't come close to covering repairs. A $15,000 underpayment on a modest claim matters just as much to a family in Cary as a large shortfall does on a bigger loss.

Because we work on contingency, you're never paying out of pocket to find out. Bring us the carrier's estimate and your policy, and we'll give you a straight assessment of whether representation will genuinely improve your outcome.

What Deadlines Do I Need To Worry About For A Property Insurance Claim In North Carolina?

Several clocks start running the moment you have a loss, and missing any of them can cost you real money. First, nearly every policy requires "prompt" notice of the claim. There's no universal number of days, but waiting weeks to report hail or water damage gives the carrier grounds to argue the delay worsened the loss.

Second, many policies require a signed, sworn proof of loss within a set window — often 60 days after the insurer requests it. This is a formal document, not just a phone call, and an incomplete or late proof of loss is a common reason claims stall or get denied in Wake County.

Third, North Carolina generally allows three years to file suit for breach of an insurance contract, though some policies attempt to shorten that period. If a dispute is heading toward litigation or the appraisal process, you don't want to discover a contractual deadline after it has passed.

Finally, there are practical deadlines: replacement cost holdback provisions often require repairs to be completed within a set timeframe before the carrier releases depreciation. When For The Public Adjusters, Inc. takes on a claim, we track every one of these dates for you and make sure nothing lapses. If your loss happened months ago and you're only now questioning the settlement, call us anyway — in most cases there's still time to act, but the sooner we review it, the more options you have.

My Insurer And I Can't Agree On The Settlement Amount — How Does A Cary Public Adjuster Resolve That Kind Of Dispute?

Most disputes we handle come down to scope and pricing: the carrier's estimate leaves out damaged items or prices repairs below what Triangle-area contractors actually charge. Our first step is building a competing estimate with photographs, moisture readings, contractor bids, and line-item pricing, then negotiating directly with the carrier's adjuster using that evidence. A well-documented supplement resolves the majority of disagreements without escalation.

When negotiation stalls, most policies contain an appraisal clause — a formal dispute-resolution process where you and the insurer each select an appraiser, and those two select a neutral umpire. Any two of the three can set the loss amount, and the result is binding on the dollar value. It's typically faster and far less expensive than a lawsuit, and it's a tool a public adjuster Cary NC property owners work with can help you invoke correctly and prepare for thoroughly.

If the dispute involves a coverage denial rather than pricing — the carrier claiming the damage is excluded or pre-existing — appraisal usually isn't the right vehicle. In those cases we build the factual record, and if legal action becomes necessary, we can coordinate with policyholder attorneys while our documentation supports your position.

The key point for Cary homeowners: a low offer is a starting position, not a final answer. You have contractual rights to challenge it, and exercising them with professional support changes outcomes dramatically.

Local Relevance

Cary sits far enough inland to escape the coast's worst storm surge, but Wake County still catches the remnants of hurricanes and tropical storms nearly every season — anyone who lived through Fran in 1996 remembers what those systems do to the Triangle's tall pines. Summer here also brings severe thunderstorms with straight-line winds, hail, and lightning, which drive a steady stream of wind, tree, and water claims.

Much of Cary's housing stock was built during the town's rapid growth from the 1980s through the 2000s. Roofs, water heaters, and supply lines in those homes are now reaching the age where failures happen — and where insurers start raising wear-and-tear arguments to reduce what they pay.

Heavy downpours can also overwhelm creeks and low-lying lots in ways homeowners don't expect, and standard homeowners policies exclude flood. FEMA notes that flood coverage is a separate policy, and NFIP claims run on their own rules and deadlines. We handle both sides — the homeowners claim and the flood claim — so nothing falls between the two.

Many Cary neighborhoods were deliberately built among mature loblolly pines, and when tropical remnants soak the clay soil and then bring wind, those shallow-rooted trees tend to come down on roofs — so photographing the tree, the point of impact, and the interior water path before cleanup crews arrive often decides how the claim gets paid.

Get A Second Opinion Before You Accept The Insurer's Number

Whether a summer storm just dropped a tree on your roof or a claim from months ago still hasn't been paid fairly, talk to us before you sign a release. For The Public Adjusters, Inc. is licensed and bonded, serves Cary and all of Wake County, and reviews your policy and damage at no cost or obligation.

Request Your Free Claim Review

Call us: (919) 400-6440

Helpful Resources

- NCDOI Public Adjusters Guide

- Federal Emergency Management Agency (FEMA)

- National Flood Insurance Program (NFIP)

- Insurance Information Institute (III)

- FEMA's flood insurance resources — Official federal guidance on NFIP flood coverage and claims

- North Carolina Department of Insurance — State regulator where consumers can verify adjuster licensing

Our services in this city

- Car Hit My House Insurance Claim Cary: When A Vehicle Strikes Your Home, Two Policies Collide — Here's Who Actually Pays

- Fire Damage Claim Adjuster Cary NC: When Your Insurance Company's Numbers Don't Add Up

- Fire Damage Claim Help For Homeowner Cary NC: Fighting Back When The Insurance Company Offers Too Little

- Flood Damage Insurance Claim Help Cary — Navigating NFIP Proof Of Loss Deadlines And Underpaid Flood Settlements

- Public Adjuster For Arson Claim Cary NC — When You're The Homeowner Wrongfully Accused Of Setting The Fire

- Smoke Damage Claim Cary NC: When A Kitchen Cooking Fire Leaves More Damage Than It Looks

- Tree Damage Insurance Claim Help Cary: When A Fallen Tree Causes Severe House Damage

- Water Damage Insurance Claim Cary NC: What To Do When A Burst Pipe, Roof Leak, Or Storm Soaks Your Home

Last updated: July 16, 2026